Local Plates, Global Stakes

Why you can’t scale without understanding what’s cooking

Brands often talk about going global, but food stays close to home. What people eat, how they cook it, who they share it with — these habits grow out of place and pace. A late lunch in Madrid, an evening snack in São Paulo, a family dinner in Chengdu — each follows its own rhythm. There’s meaning in the ingredients, the timing, and the company. These aren’t small differences. They shape the role food plays in everyday life.

Behaviour doesn’t travel as easily as strategy.

Yet the growth playbook still leans on the idea that a product built in one country will thrive in another with only light adjustments. Packaging shifts. Positioning shifts. But the core often stays the same.

That assumption is breaking.

What’s on the plate may look familiar. The pattern around it rarely does. Eating habits reflect climate, work hours, generational ties, even the pace of conversation. These things don’t show up in category data, but they decide whether a brand feels present or misplaced.

Growth begins when brands stop treating habits as hurdles and start treating them as signals. The clues are there — in kitchens, in calendars, in quiet, ordinary routines. All it takes is a different kind of attention.

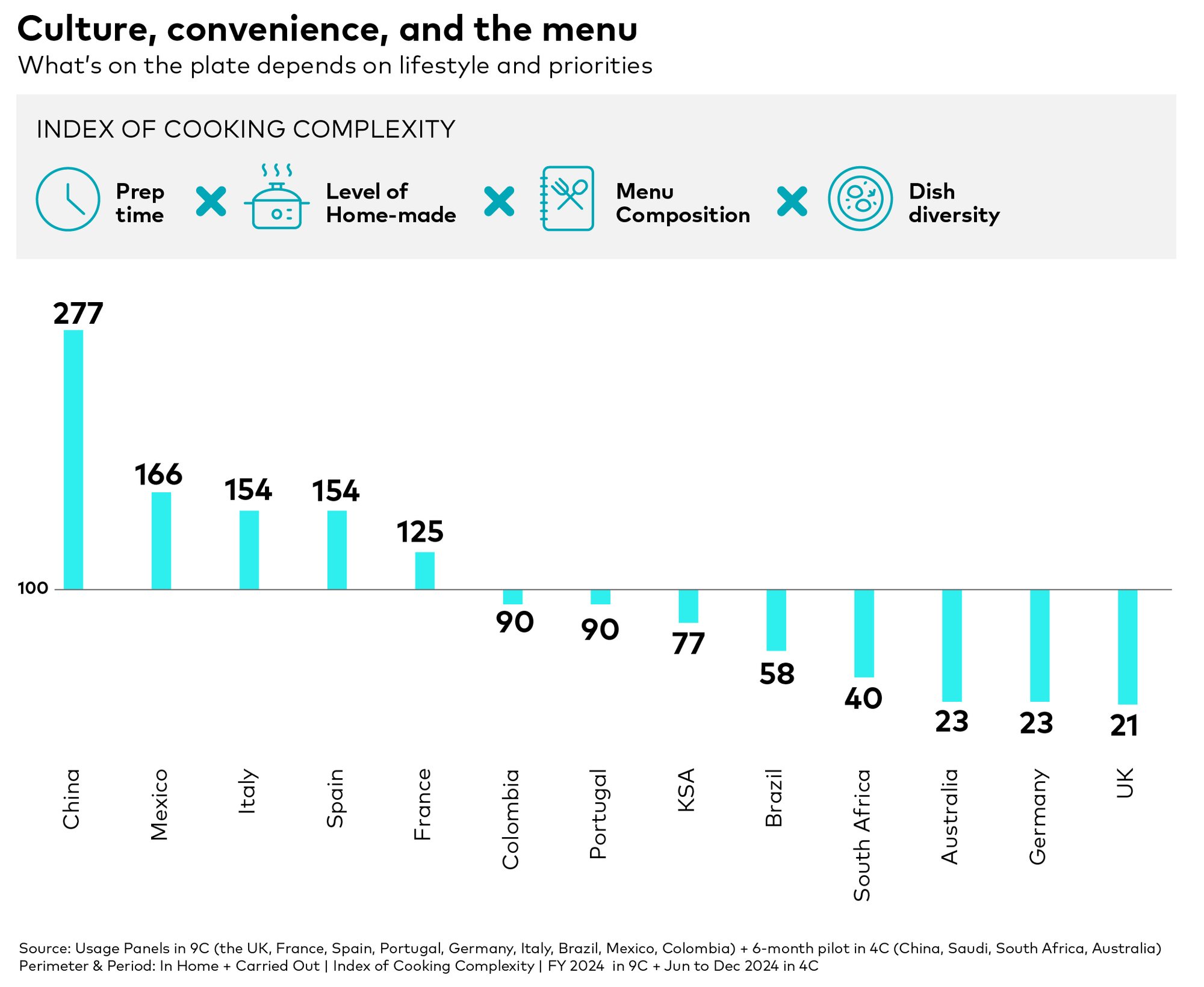

From rigid to real

In the last year alone, we’ve seen a 3% drop in the number of dishes prepared per person across Europe, and a 15% decline when compared to 2019. Even dessert, once a ritualised part of formal meals, is shrinking fast: –3% year-on-year, –6% since 2019. Morning meals are drifting later. Dinner menus are slimming down. Eating today is driven by personal pace and emotional context, not by a fixed schedule. GLP-1 drugs that curb appetites are also increasingly playing a part in the shift away from complete meals.

Meal times are moving; so are the rules around how we eat. In China, traditional menus still consist of multiple components: a soup and cold starter, followed by hot dishes, hot pot, and a selection of staples like rice or noodles. These meals take time, coordination, and intention. But in much of Europe, that complexity is being replaced by simplicity.

Across countries like Spain, France, and Italy — historically known for elaborate home cooking — meal prep times are falling. In the UK, it’s just 20.5 minutes. Germany sits at 21.6, and Portugal at 18.1. Alongside this, the share of ready-to-eat (RTE) meals is climbing: +1.9 in Germany, +0.9 in France, and +0.6 in Portugal year-on-year. These aren’t one-off changes — they’re indicators of a structural shift in how people allocate time and energy to food.

Effort is only half the story; outcome is what counts. Single-bowl meals are fast, nourishing and low-prep — and they’re winning. Traditional multi-course menus are losing ground, even for higher-effort occasions like “Filling Meals” or “Family Favourites.” Across the board, the average menu now includes fewer components: fewer starters, fewer mains, fewer desserts. It’s not that people don’t want enjoyment — they want it in ways that suit their lifestyle.

Cultural specificity adds another layer. In the UK, tea and biscuits remain a bedtime staple. In Brazil, evening means beer and crisps. In Saudi Arabia, it’s kabsa. In Colombia, it might be arepas. These aren’t just food choices — these are ritualised moments. They reflect how cultures close the day, how households wind down, and how products earn their role at specific times.

Even within a shared occasion like snacking, behaviour diverges sharply. In some countries, after-dinner snacking is the most incremental, meaning it adds the most additional consumption. The correlation is striking: countries with strong after-dinner snack cultures (Brazil, France, Mexico, Spain) also tend to have higher total snacking levels. In contrast, early breakfast — say, 6am to 8am — has almost no predictive value for how much people will snack later in the day. So if you're basing your targeting strategy on breakfast patterns, you may be looking in the wrong place.

This is where traditional marketing logic fails. It assumes cause and effect where there’s only coincidence. A big breakfast doesn’t reduce snacking. In fact, those who eat big breakfasts often snack more, not less. The behavioural profiles alongside these choices change what it means to position a product effectively.

Format meets function

This fluidity is also reflected in category blurring. Cheese at breakfast. Eggs as snacks. Yoghurt as dessert. Food is no longer bound by its aisle or packaging. In Brazil and Saudi Arabia, cheese is a morning item. In Australia and Portugal, it’s an afternoon snack. In France and Italy, it still holds its place at the centre of meals. So where your product fits — and how it's used — depends entirely on local rhythms.

For brands, this means one thing: localisation is essential. If you’re only thinking in terms of category, you’ll miss the crossovers. If you’re only measuring by daypart, you’ll miss the bridges between moments.

That’s why Worldpanel built the Demand Moments framework. It captures eating and drinking occasions not by product type or time slot, but by human context — need state, mood, setting, and intent. It allows brands to identify 14 distinct moments, from “Restore & Replenish” to “Sofa & Chill,” each one with its own logic, emotional cues, and product relevance.

When combined with Demand Spread Score — our KPI that tracks how many of those moments your brand is present in — it becomes a powerful tool for market entry and role expansion.