Thailand, Malaysia, the Philippines and Vietnam

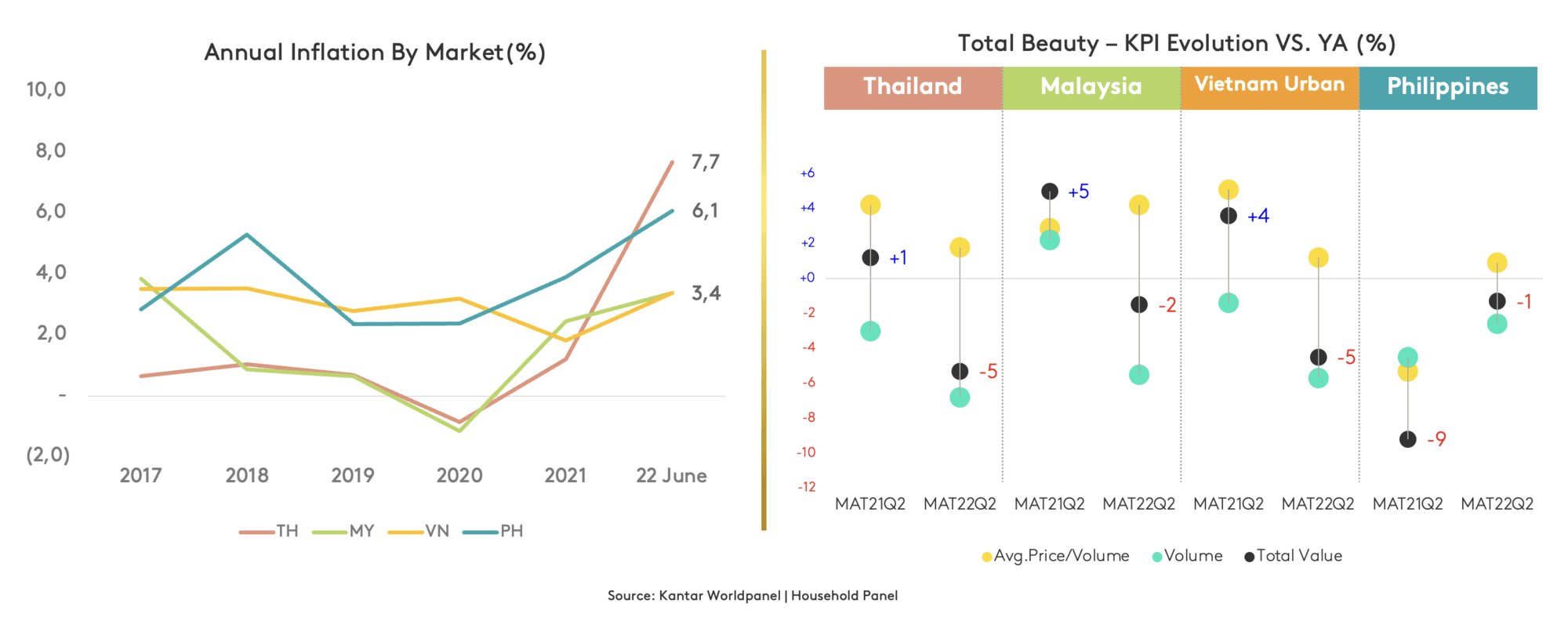

Beauty shoppers in Thailand, Malaysia, the Philippines, and Vietnam are feeling the pressure from inflation more acutely than anywhere else in Asia.

It has weakened consumer spending power and resulted in steep price increases across the beauty category. Price and consumption sit in a ‘see-saw’ relationship with each other and we can see this clearly in these four markets, where the volume of beauty products purchased has decreased.

However, despite the need to manage their budgets, shoppers are not only looking to buy products that are cheap or commoditised. In fact, they have a healthy appetite to try out new formats, invest in premium products, and add steps to their grooming routines. This presents exciting opportunities for brands that can innovate and introduce new ideas while making their offerings affordable for consumers.

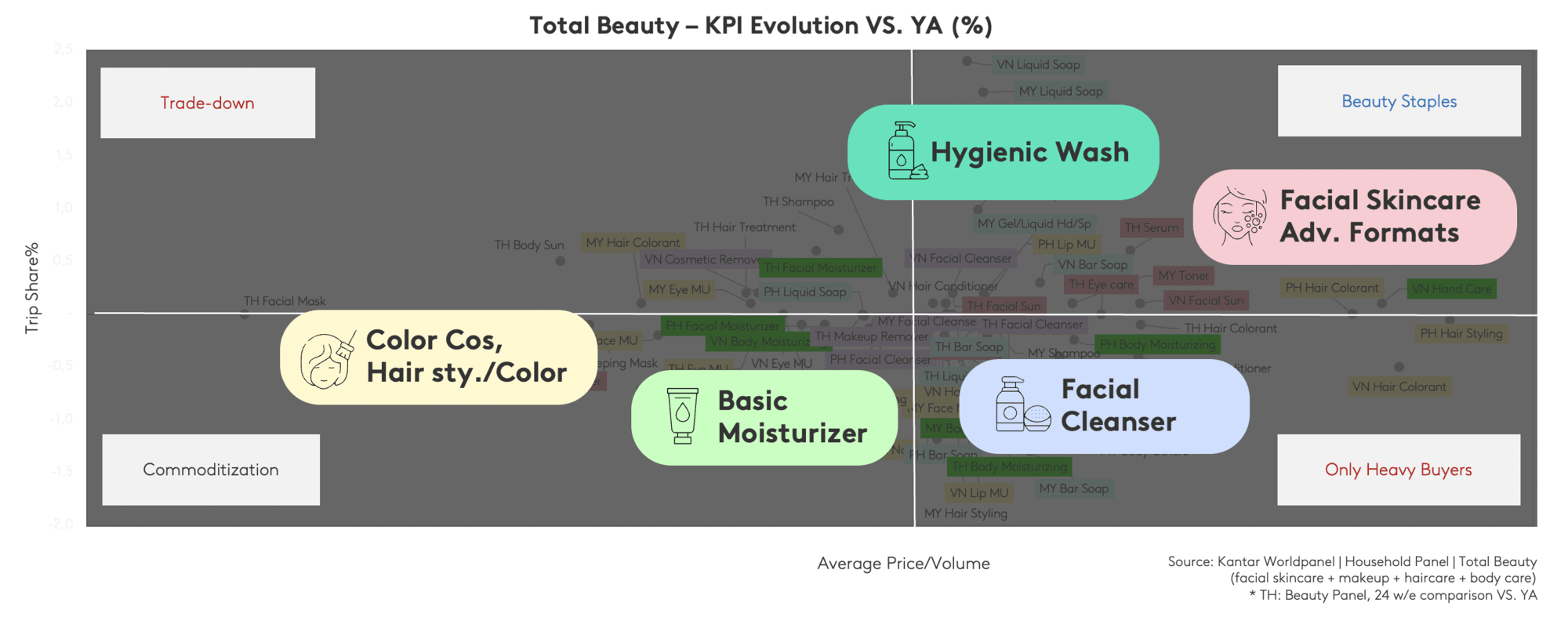

Colour cosmetics and hair styling products have declined in importance to households in Thailand, Malaysia, the Philippines and Vietnam, due to the prolonged impact of pandemic restrictions on mobility and the ability to socialise.

It’s a very different story for facial washes, facial cleansers, and hygiene care, which took on greater significance in consumers’ lives as awareness of the importance of sanitation rose. Shoppers are continuing to add these staple products to their baskets, even as prices climb.

Facial cleanser, for example, is one of the core categories within facial skincare, particularly in Malaysia and Vietnam where it accounts for more than 30% of total sector spending.

What’s more, these staple categories are developing. Not only do consumers want to keep buying them, but they are willing to pay premium prices.

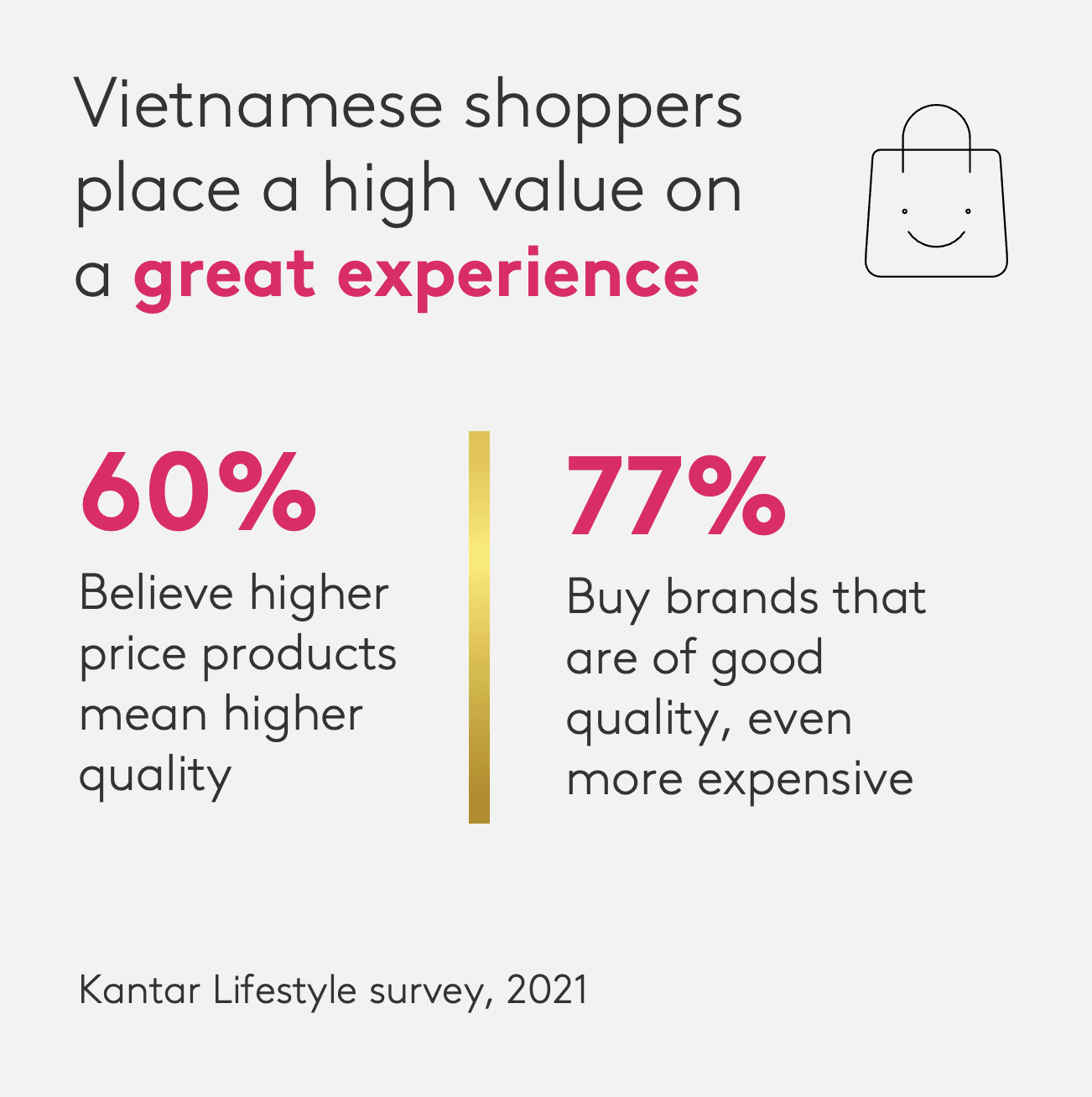

Shoppers in these four markets have become more conscious of the ‘actual value’ of their beauty purchases – measured in terms of the experience it brings them or the benefits of using it, rather than in monetary value.

Consumers in Thailand, Malaysia, the Philippines, and Vietnam are keen to try out new formats in facial skincare, such as toner, serum and sun protection. They explored diverse categories during the pandemic, as they spent more time at home, and many have either kept or continued to expand the new skincare routine they developed in recent years. Meanwhile, the popularity of ‘plain’ moisturisers, for example, has declined. Within body wash and facial cleansers, we can see consumers moving away from traditional bar soap towards more sophisticated liquid formats in a higher price tier, which offer additional medical benefits such as antibacterial ingredients that kill viruses and bacteria.

Brands are also evolving their products to meet this demand, creating premium versions by introducing new properties. This trend is coming from two directions:

In Malaysia, Lux and Safi have both launched liquid washes with added antibacterial benefits, while traditional medical concept brands, including Dettol, have developed products with skincare ingredients that elevate them above their core hygienic function. Lifebuoy is another example of a brand which has launched products to address specialist skin concerns, such as body acne, with the ability to remove bacteria from the skin.

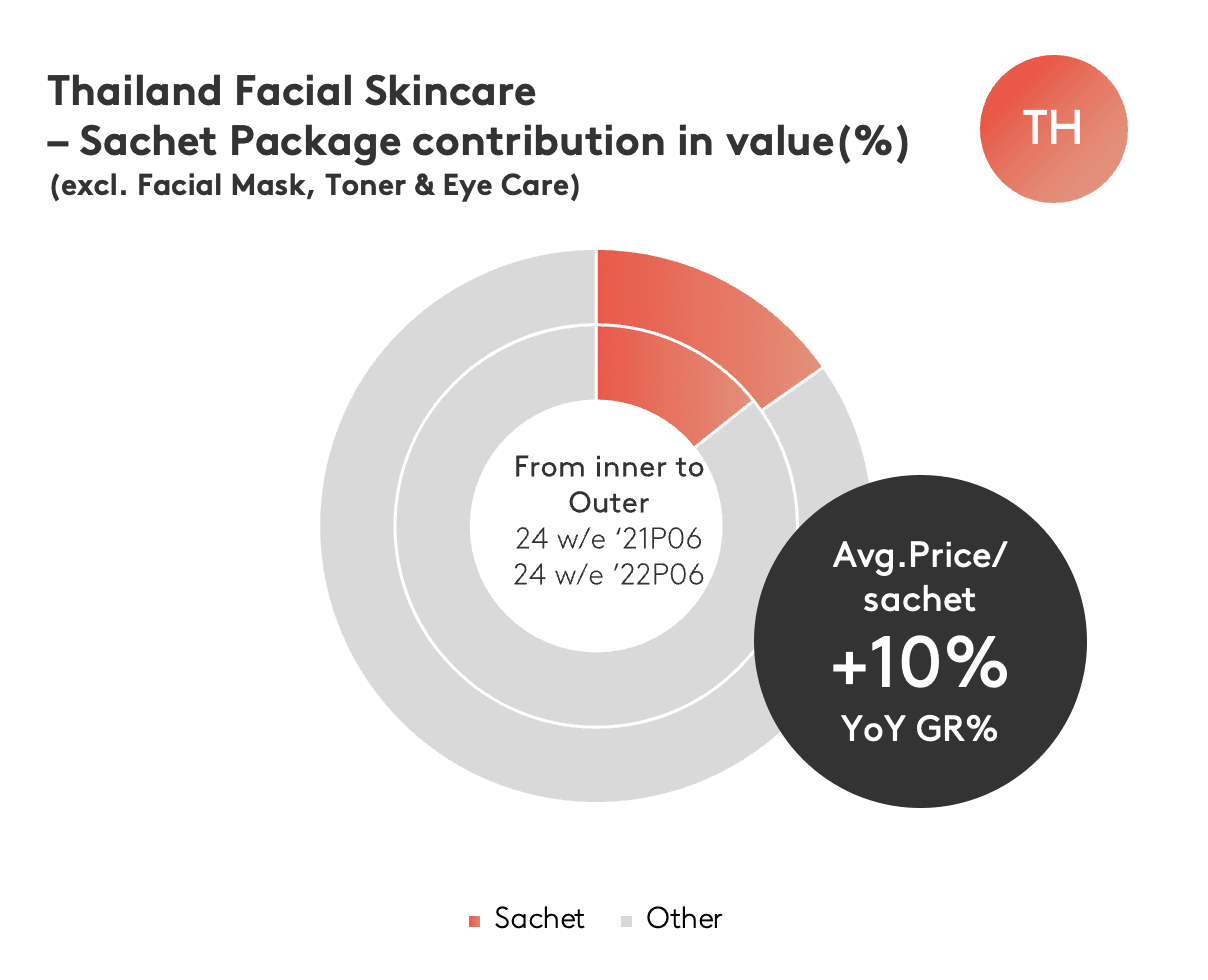

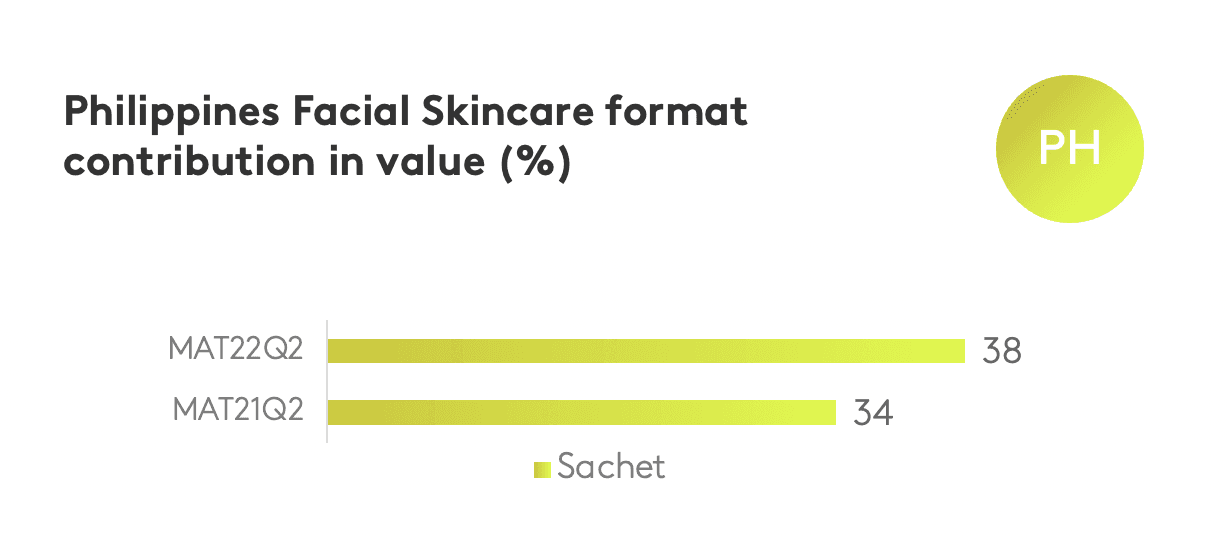

Brands are encouraging consumers to trial new and different formats by finding a variety of ways to lower the entry barrier to purchase. Prestige and medical derma brands that sell at a higher price on average are offering promotional bundling to make themselves more attractive and affordable.To make their products more accessible, many brands are launching small package or sachet versions. This allows shoppers to explore and trial advanced formats such as serum, or sophisticated benefits such as brightening, at low cost and low risk. Facial skincare brands in Thailand and the Philippines have leveraged this strategy with particular success to lift shoppers’ spend per trip.

In Thailand, the initiative has driven up the average price per sachet by 10%, increasing the contribution of facial skincare in sachet formats to total category value in 2022.

In the Philippines, meanwhile, 38% of the total value of facial skincare now comes from products sold in sachet format, compared with 34% in 2021.

Giving shoppers a good reason to purchase plays an essential role in raising consumer demand for new categories, for example by providing online content that educates them on the usage occasions of new formats and properties. Done well, this can turn occasional usage into regular daily usage.

In Vietnam, educational campaigns run by beauty brands have increased awareness of the need to use suncare products every day, directly contributing to an 11% growth in category value. At the same time, they have influenced a 12% increase in the consumption of make-up remover, by highlighting the importance of two-step cleansing.

Consumers’ minds are open to mass beauty brands, which are launching enhanced products that give shoppers with restricted budgets the opportunity to upgrade their beauty routines at a lower price point.

In Thailand, mass brands are meeting consumers’ demands for flawless and transparent skin with affordable serums – a category that was mainly owned by prestige brands – in advanced formats that address specific concerns such as dark spots or melasma. Local brands are driving the success of the serum category, in particular Jula Herb, which increased an impressive 225% in value during the past year, and Clear Nose, which rose 22% in value.

1. More sophisticated beauty routines

Despite their limited spending power, consumer demand for more sophisticated and advanced beauty routines is growing in Thailand, Malaysia, the Philippines and Vietnam. We recommend that brands and manufacturers leverage this by developing enhanced offers that lower the barriers to trial.

2. Premiumised hygienic care

Brands that would like to increase their presence in these four markets could also win new buyers and increase spending by taking advantage of the interest in premiumised hygienic care, as the impacts of Covid-19 continue into the post-pandemic era.

3. Advanced formats in facial care

In the facial care categories, there is a golden opportunity for mass and masstige brands to meet shoppers’ needs as inflation bites – but they must remember that consumers are craving upgraded, advanced formats, rather than commoditised, volume-driven offerings.