As we reported in Winning Omnichannel 2021, take-home FMCG growth quadrupled from 2.5% in 2019 to 10% in 2020. But did this result in more brands growing or a change in how they grew?

Benjamin Cawthray, Global Thought Leadership Director, Worldpanel Division, Kantar

Before COVID-19, the growth of global FMCG sales had slowed—with just 2-3% reported in 2017, 2018 and 2019. This slowdown made it harder for brands to find new growth.

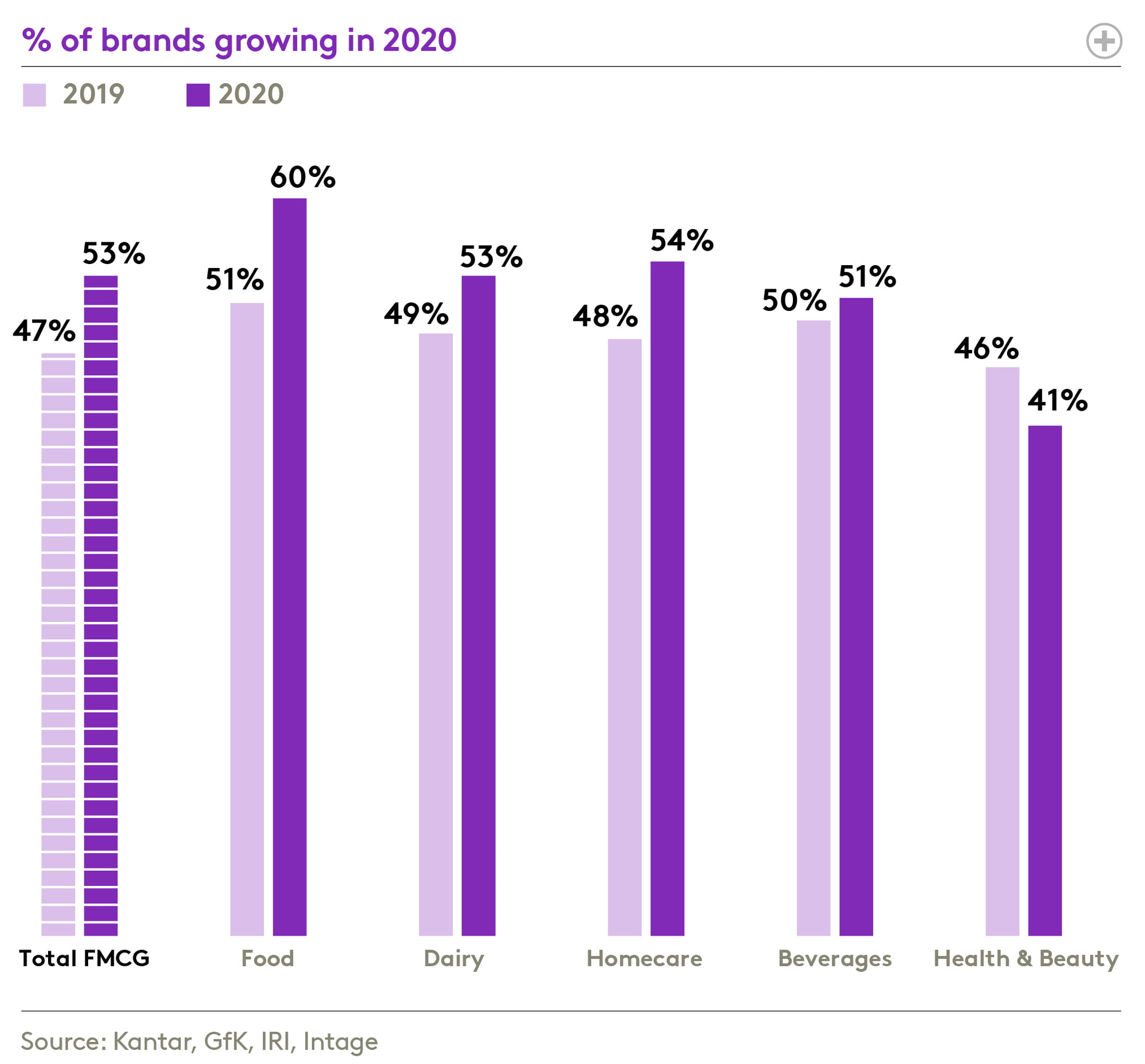

But the events of 2020 turned this on its head. With the FMCG industry enjoying an impressive 10% global growth over this period, a bounce-back for brands was seen. 53% saw an increase in their CRPs—representing a +6% swing on the previous year.

At a sector level, the bounce-back reflected the value growth. Food brands saw the most significant swing (+9%), which also grew by 11.4% in value. At the opposite end, Health & Beauty brands saw 5% fewer brands growing in 2020—mirroring its fall in value.

Extraordinary changes in the way we shopped

The average number of FMCG trips made by households fell by 2% across 2020. This may sound like a small number, but in reality, that’s 1.6 billion fewer shopping trips being made in 2020. This means that almost all the growth across regions came from more spend per trip—a metric that increased by 11%.

In practice, this means that shoppers were putting more volume in their baskets, broadening the range of categories they were buying and often purchasing bigger pack sizes.

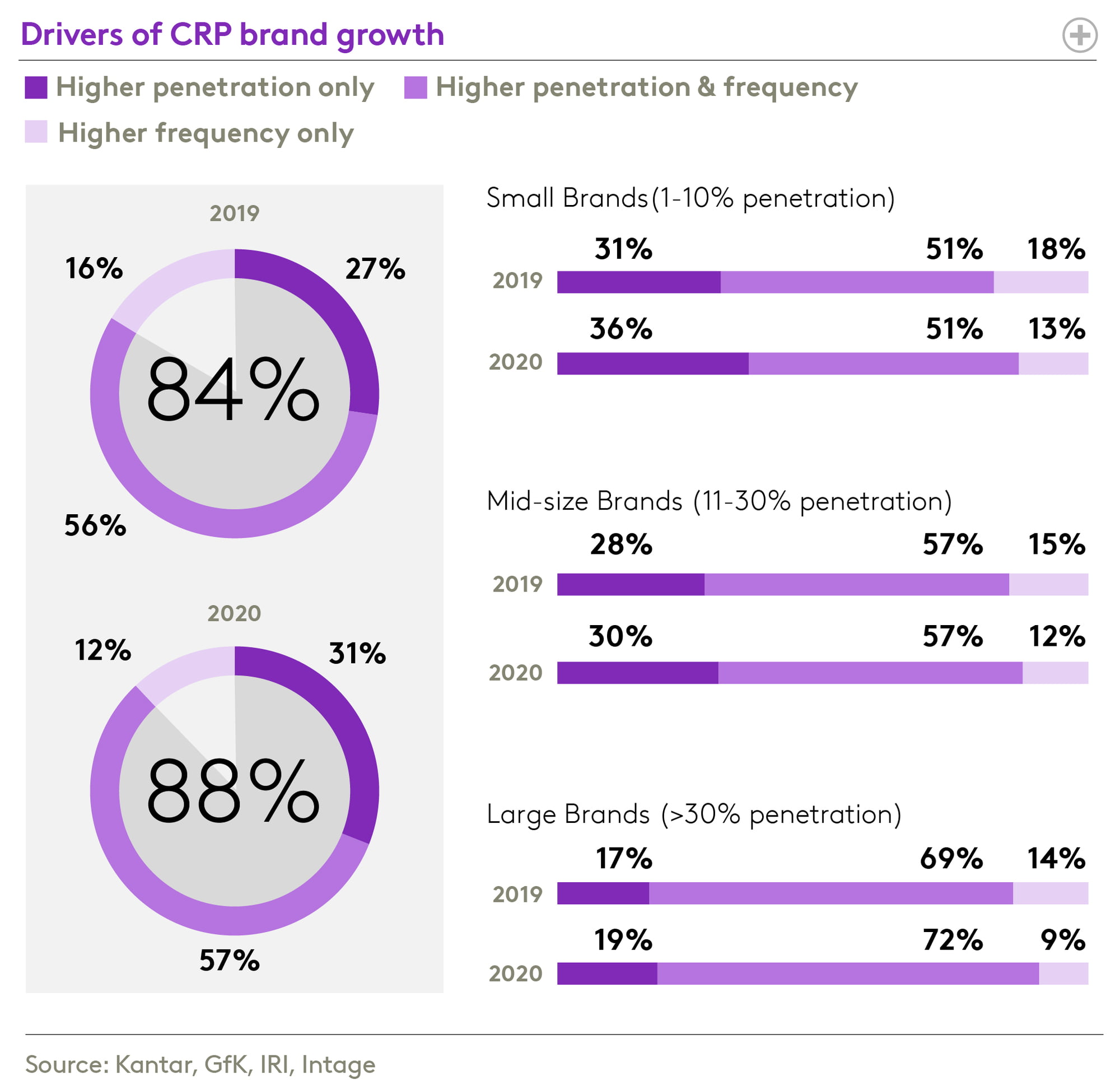

Did this change in behaviour impact how brands grew last year? In 2019, 84% of growing brands found more shoppers. But in 2020, this figure increased to 88%, making finding more shoppers more important than ever.

The size of a brand also has an impact on this type of analysis, with different ratios of growth coming from finding more shoppers versus frequency. But the results were just as impressive when we controlled for size, with an increase in penetration-led growth seen across all the board.

This analysis also uncovered that larger size brands made up a bigger proportion of growing brands increasing from 50% to 54%. Combined with the fact that more brands grew, this shows that shoppers returned to those they knew best during the pandemic.

Rules for growth and 2021 target-setting

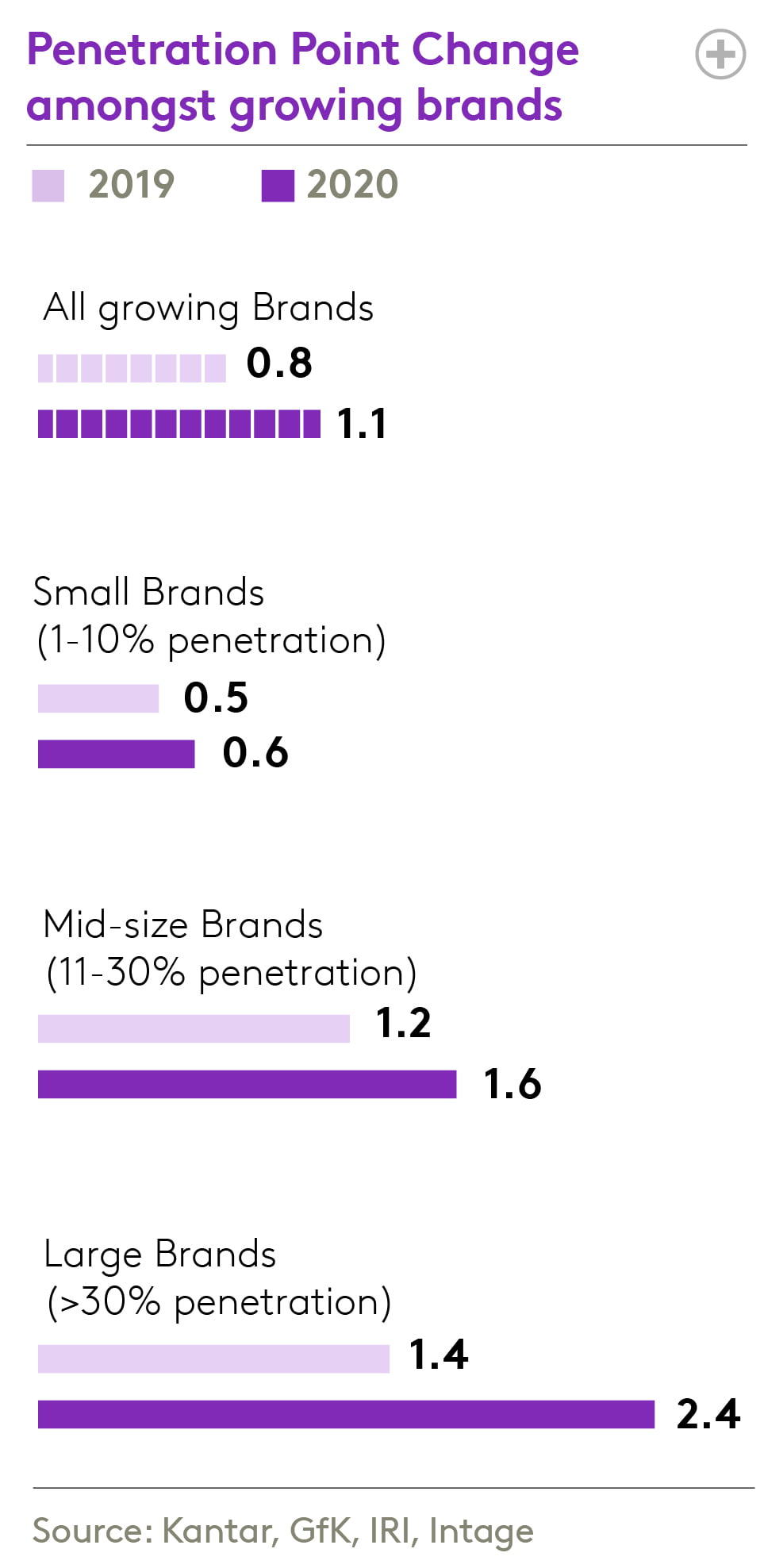

With finding more shoppers more important than ever, what is a realistic penetration target?

Growing brands in 2020 experienced more shopper gains than brands in 2019. The median increase was 1.1 penetration points—up from 0.8 the year before.

But is this down to more larger brands growing than previously? Again, controlling for size, there was an increase in penetration gains across the board. This shift helps guide us on what is realistic for 2021 brand growth.

A nuanced target between 2019 and 2020 gains would be sensible. If your brand is small, success looks like +0.5 penetration points gained, for mid-size brands +1.4, and for large brands +2.

The return of global brands?

In recent editions of Brand Footprint, we have reported on local brands steadily winning share against global brands. And from the outset, it appears that global brands had a strong year, gaining back any losses from the previous few years.

However, the same split at a regional level shows that local brands are still winning share—particularly in the USA, where the share of global brand spend is much higher and the region is growing the fastest.

Despite larger brands doing well in 2020, the best performing markets display a mix of global and local brands—with the local brands still winning.