The omnichannel present

How brands can navigatethe retail revolution

Omnichannel stabilises as consumers mix and match for better value

Retail is becoming more complex across Latam. Consumers expect to be able to buy your brand at any time and place. The line between formats, channels and even the digital world has blurred. E-commerce may only account for 1% of FMCG value in Latam but it’s on a steep growth curve, up 40% last year.

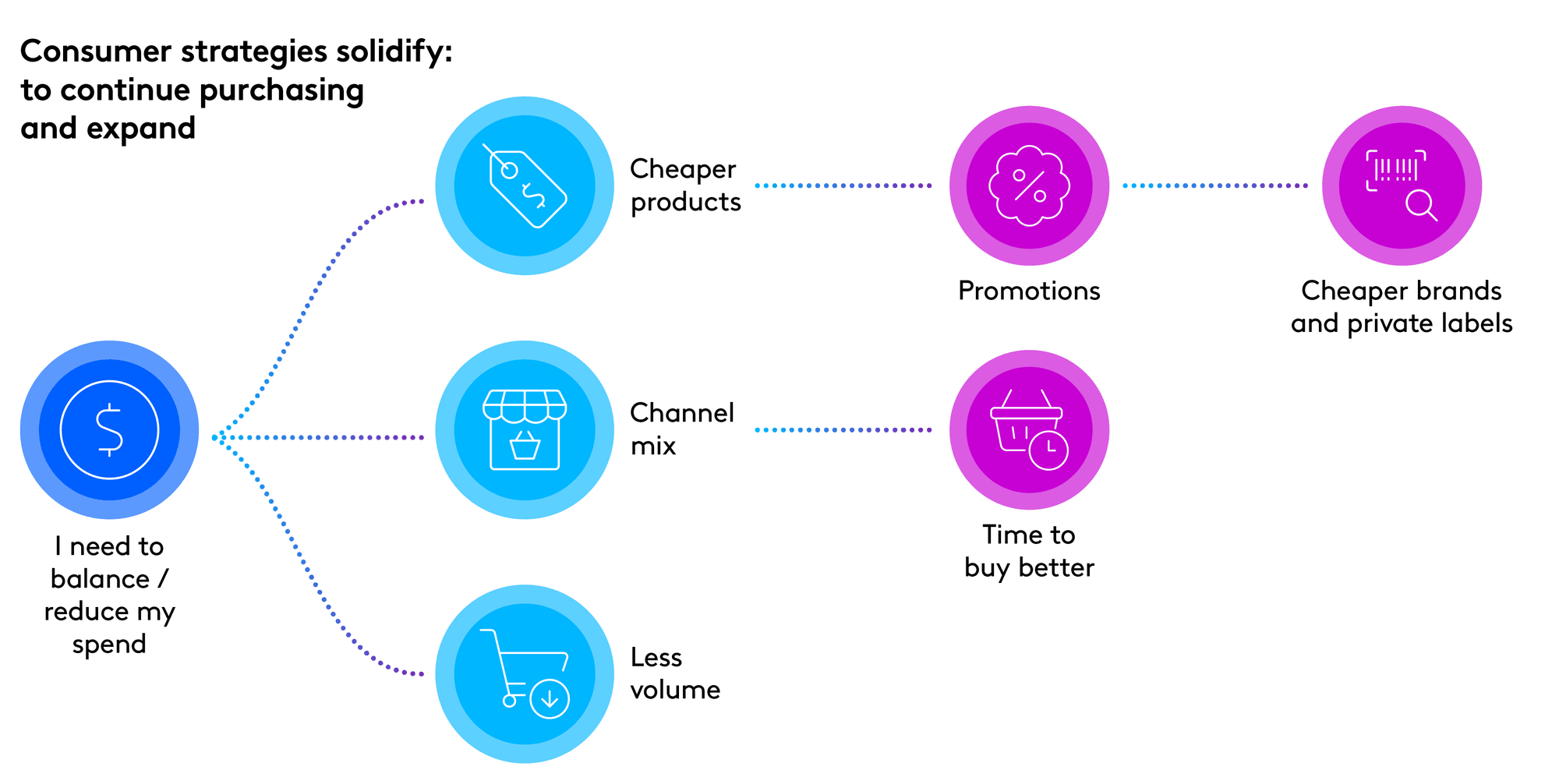

Consumers do not have a plan to transform retail, they simply take advantage of the opportunities that make their lives easier. In some cases, the answer will be traditional, in some it will be modern trade and for others it will be discounters or even their smartphone.

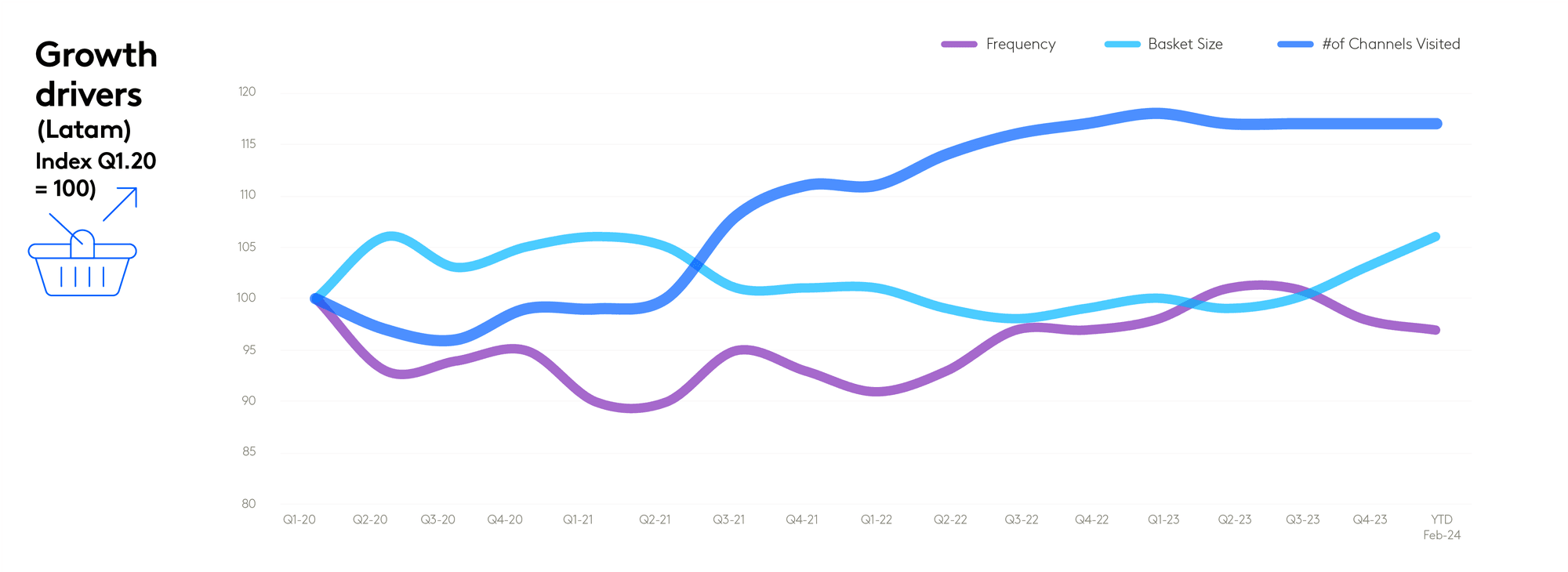

The good news is that the transition could be slowing down (though there’s always potential for further dramatic changes). What we see is that Omnichannel, after growing 20% during the pandemic as consumers learned to look for products in more places, has stabilised. The number of channels used by the average household has remained constant at just over 9.

The key change is the need for retail channel integration, which is happening at different speeds for different markets and consumer groups.

In 2023, shopper expenditure on consumer goods increased by 8.6% globally, the second-fastest in the past 12 years, behind only the pandemic spike in 2020. This growth was primarily driven by persistent inflation, a dynamic that insists on pushing its way into consumer spending power in 2024. Prices in most categories remain high.

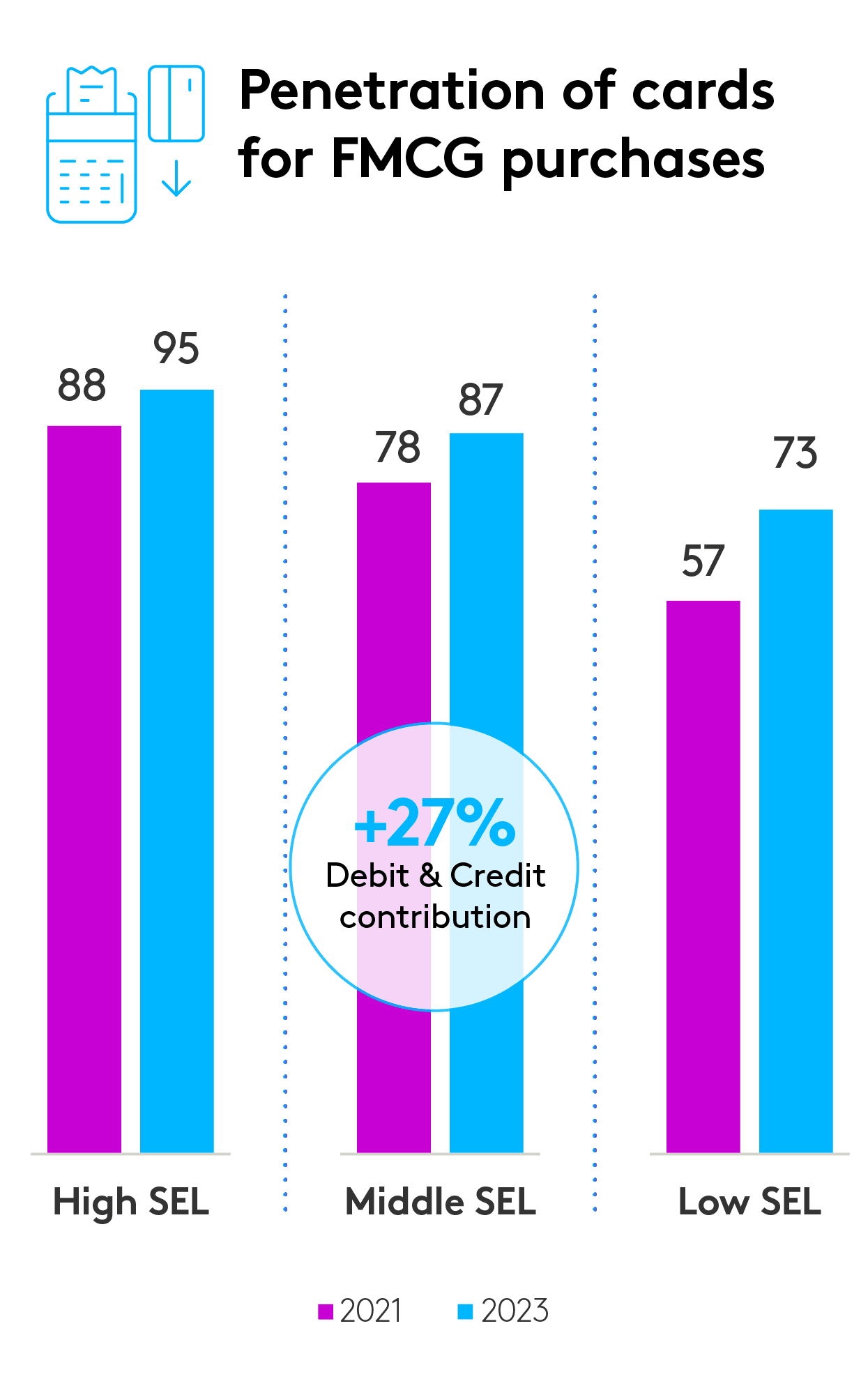

Latam consumers have responded in recent years by moving away from the traditional trade, which used to make up the bulk of purchases, to seek out more options on promotions, packaging, pricing and product range. This has allowed them to make different and smarter purchases for their circumstances, helped by the increasing availability of card payments. These are now used for 87% of FMCG purchases among middle income families, a rise of 27% between 2021 and 2023.

The result is a new landscape for brands to navigate and many have responded with smart promotional strategies knowing that 1/4 of FMCG growth in the last year came via promotions.

We spotted six key trends in consumer behaviour:

Polarising powerplays

The average FMCG growth in 2023 was 8% globally but beverages, and health and beauty products experienced even higher growth rates. This growth was partly a function of inflation but also reflected the sectors’ ability to premiumise their offerings effectively.

In Latam consumers have sought to maintain their basket, sometimes by buying smaller packs in categories such as snacks, enabling them to continue to purchase their premium treats.

Successful premium brands have tapped into emerging consumer needs, such as wellness and indulgence, which have remained resilient in consumer spending priorities despite overall tighter budgets. This ability to align with consumer preferences and introduce value-added products allowed these sectors to drive higher revenue growth.

The bottom line was that they found ways to convince shoppers to buy from them and save elsewhere.

Shopping behaviours and omnichannel

There was also a noticeable increase in shopping frequency and trip spend across regions, driven by consumers searching for the best prices across different channels.

Across Latam the rise of omnichannel may have stabilised but consumers are still visiting nearly nine different types of stores each year, following the global trend of dividing their grocery shopping across more stores to save money.

They are still behind the global numbers, however, with consumers buying groceries from an average of 20.7 different stores in the latest year on average, an increase from 16.8 stores in the year prior to the pandemic, a growth of 23%.

For brands, the vital message is that meeting consumers at their point of need and ensuring visibility at every conceivable touchpoint matters more than ever. It can be a tough game, but being more present will always be central to winning.

Private labels and product plays

Private label products have increasingly become a staple in consumers’ shopping habits, particularly in Europe, where they have carved out significant market shares. In 2023, private label products grew globally at a rate of 11.2%, surpassing the growth of branded products, which stood at 7.9%. This growth was not isolated but rather part of a broader consumer shift towards products that balance quality and affordability.

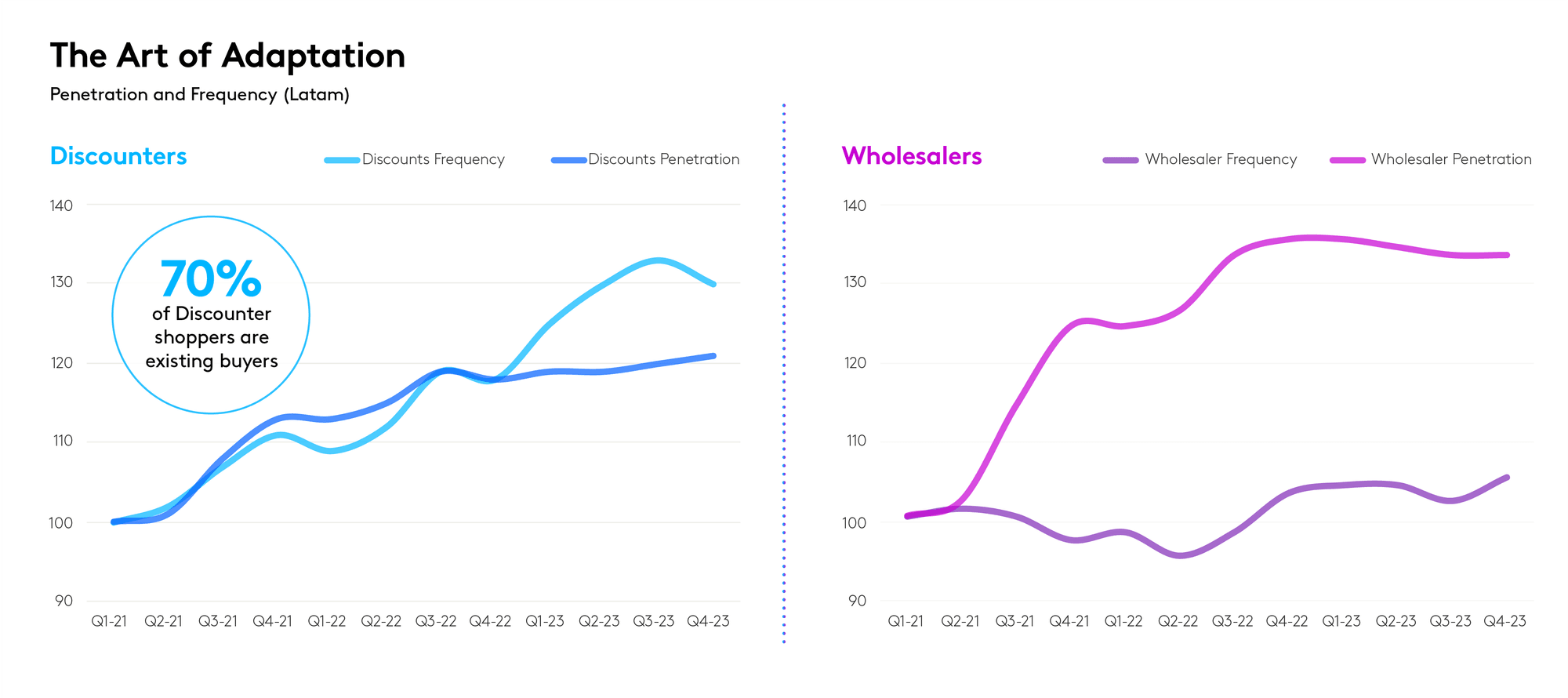

In Latam, Private Label doesn't account for as much of the market as it does in Europe, having just 5% overall FMCG value share. It has, however, been the fastest-growing area and, in some countries, such as Colombia, already takes more than 20% share. Development is tightly linked to the spread of Discounters, which has been stronger in countries such as Colombia, Ecuador, Mexico and the Central America region. These markets are expected to see the fastest growth of Private Label in the next few years.

The rise of discounters

Discount stores have emerged as one of the fastest-growing retail channels globally, particularly in Europe, where they have even more firmly entrenched themselves in the consumer shopping routine.

In 2023, there was noticeable expansion in the United States and Latin America. In Latin America, super and hypermarkets, along with traditional trade, still hold the biggest share of the market but there was a significant rise in the use of price value formats. With discounters rising in Mexico, Colombia and Ecuador and wholesalers growing in Brazil and Chile.

Across the region, discounters grew more than 303m shopping occasions while wholesalers added 1.5m new shoppers.

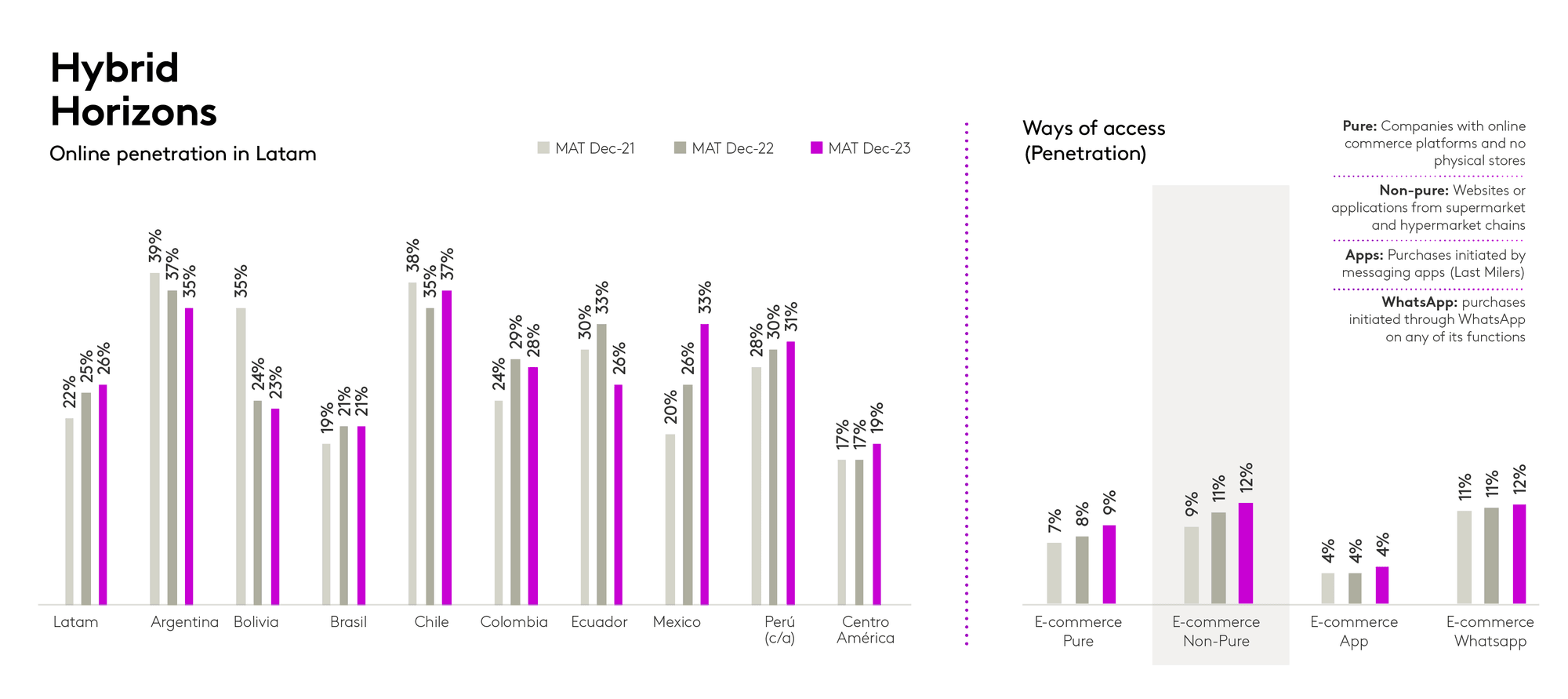

Ecommerce evolution

The significant drivers of ecommerce growth include increased shopping frequency and the broadening of consumer bases, which now cuts more clearly across generational lines, with both younger and older consumers appreciating the convenience of shopping from homes and phones. But there is clearly significant room to expand penetration in most markets.

Across Latam we see continuing overall growth in online penetration although as ever it’s not uniform. In the year to December 2023, online penetration hit 26% regionally (up 1% year on year), although that hid declines in Argentina, Bolivia, Colombia, Ecuador and rises in Chile, Mexico, Peru and Central America.

Seamless shopping

As the boundaries between online and offline shopping blur, brands that successfully manage the integration of digital, physical and away-from-home shopping experiences see remarkable gains in both reach and resonance.

But the omnichannel approach extends beyond building a mere presence. It encompasses a strategic deployment of resources to ensure that every consumer encounter — be it online, in- store, or via social media — reinforces brand values and drives engagement.