BRAND FOOTPRINT 2025

Decoding brand choicesin Scotland

Since its launch in 2013, we've built the most comprehensive picture of consumer choice available anywhere, now covering more than 30,000 brands across 56 countries. The depth and breadth of this data is incomparable. It enables us to celebrate...

The top 20 rankings

Predictions for the remainder of the year

What is Brand Footprint

Find out more

Every year, our Brand Footprint rankings show which FMCG brands are being picked most often. The metric behind them — Consumer Reach Points (CRPs) — tracks both penetration and frequency. It doesn’t measure awareness or media buzz. It reflects actual choice. Real decisions, in real homes.

In Scotland, where overall consumption has remained flat, those choices tell us even more. There’s no tide lifting all boats. To hold position, let alone grow, a brand must find relevance in how people eat, shop, and live. It’s no longer enough to be visible. You have to be useful, and consistently so.

Irn Bru remains Scotland’s most chosen brand. That result isn’t surprising for this iconic drinks brand, but it is instructive. The brand continues to find its place in the middle of the day — lunch and afternoon snacks — even as pressure builds at evening meals. It’s growing across a wider range of age groups, which suggests a deliberate shift in how it connects with shoppers. Strong Consumer Reach Points (CRPs) are the outcome of that breadth. Irn Bru keeps showing up in the moments people reach for it.

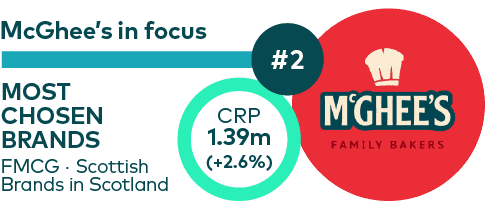

McGhee’s, is gaining ground through coverage across breakfast, lunch and snack moments. Like others in the bakery space, it faces pressure from evolving eating habits. But its tone and outreach — especially on social media — suggest a push to connect with younger consumers. If the brand can continue to win new buyers while retaining its core, it has a good shot at sustainable growth in a segment that is otherwise softening.

From a portfolio perspective, McGhee’s has also seen notable frequency gains across its top-selling SKUs, including rising repeat rates for staples like Soft White Floury Rolls and Pineapple Tarts. An uplift in online channel sales also hints at improved digital shelf presence and broader accessibility beyond the traditional bedrock of supermarkets.

Simon Howie #6 is showing momentum. The butchery staples brand is building strength at lunch while becoming less tied to the evening meal. That shift creates resilience. The broader the range of use cases, the less exposed a brand becomes to external factors, whether it’s changing habits or unseasonal weather that disrupts barbecues and other occasional formats.

Baxters, #7 best known for soups and condiments, reflects a more traditional pattern. Consumption is stable, anchored in lunch and dinner. That’s where the brand has long played a role, especially among older households. While growth is limited, Baxters continues to serve consistent needs in consistent ways. There’s value in that kind of dependability, particularly when trend-led categories face sharper swings.

Scotland’s FMCG landscape hasn’t shifted dramatically in volume terms. But the patterns of use beneath the surface have. Snacking is in decline. Mealtime structures are less predictable. Brands that understand how those moments change and shape themselves to meet them hold their place in the rankings.