The movers and shakers within Latam’s FMCG categories

We demonstrated the vital role that growing penetration plays in achieving growth – both in the short and long term.

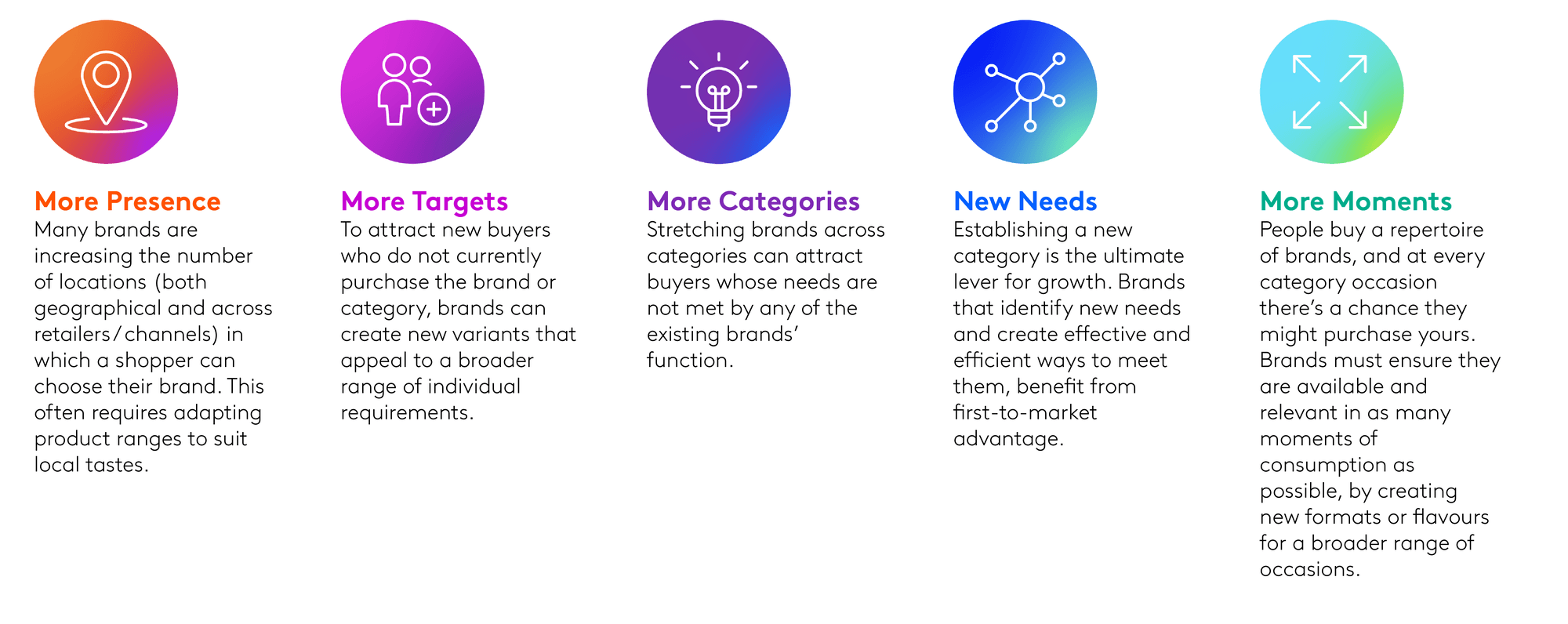

For each case study in this chapter, we have identified the combination of growth levers each brand has used. Here’s a quick reminder of the five levers.

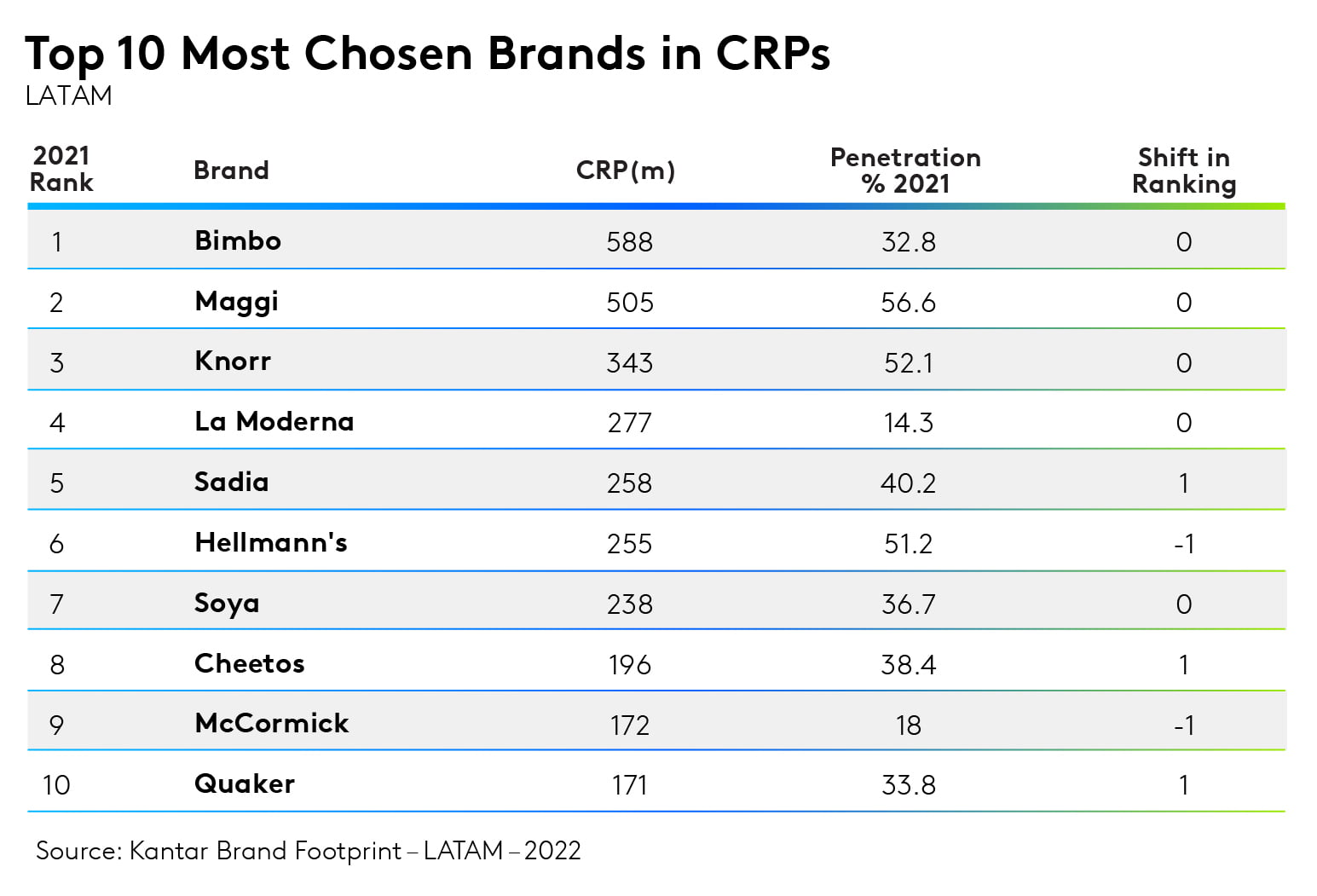

Bimbo retained its No. 1 spot in the food category with nearly 590(m) CRPs, significantly ahead of Maggi and Knorr at No. 2 and No. 3 respectively. In a fairly static ranking for 2021, the only movement came from a couple of position swaps with Sadia moving above Hellmann’s to take the No. 5 position and snacks Cheetos rising above spice brand McCormick’s to become the new No. 8. Oat brand Quaker also moves into the top 10.

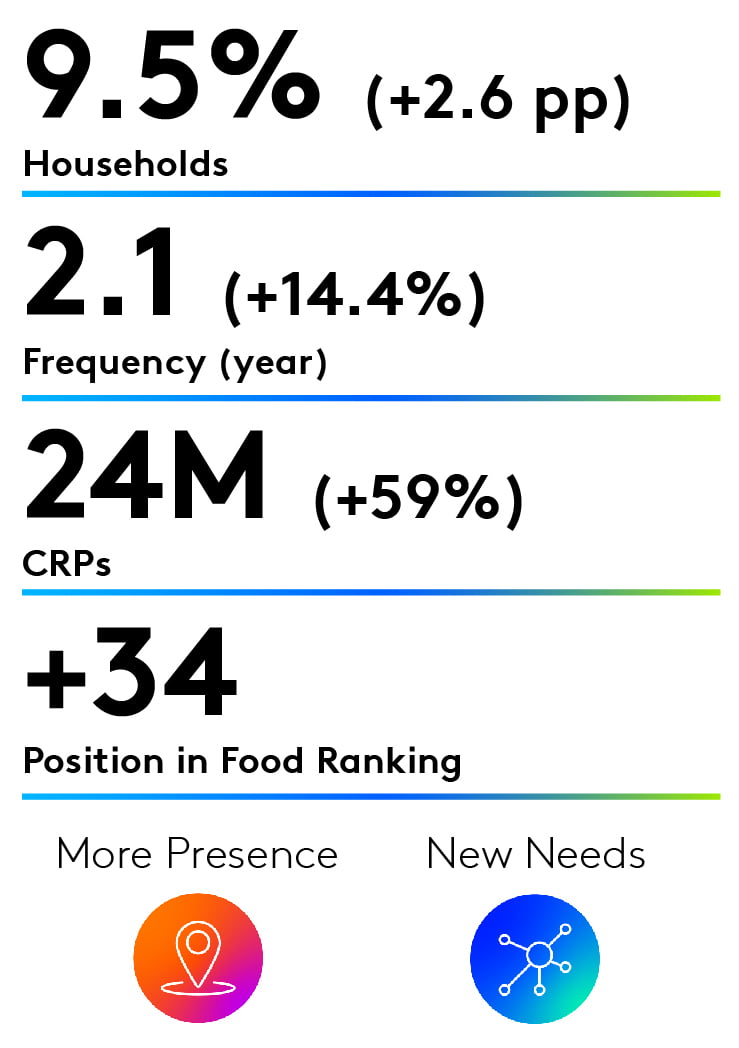

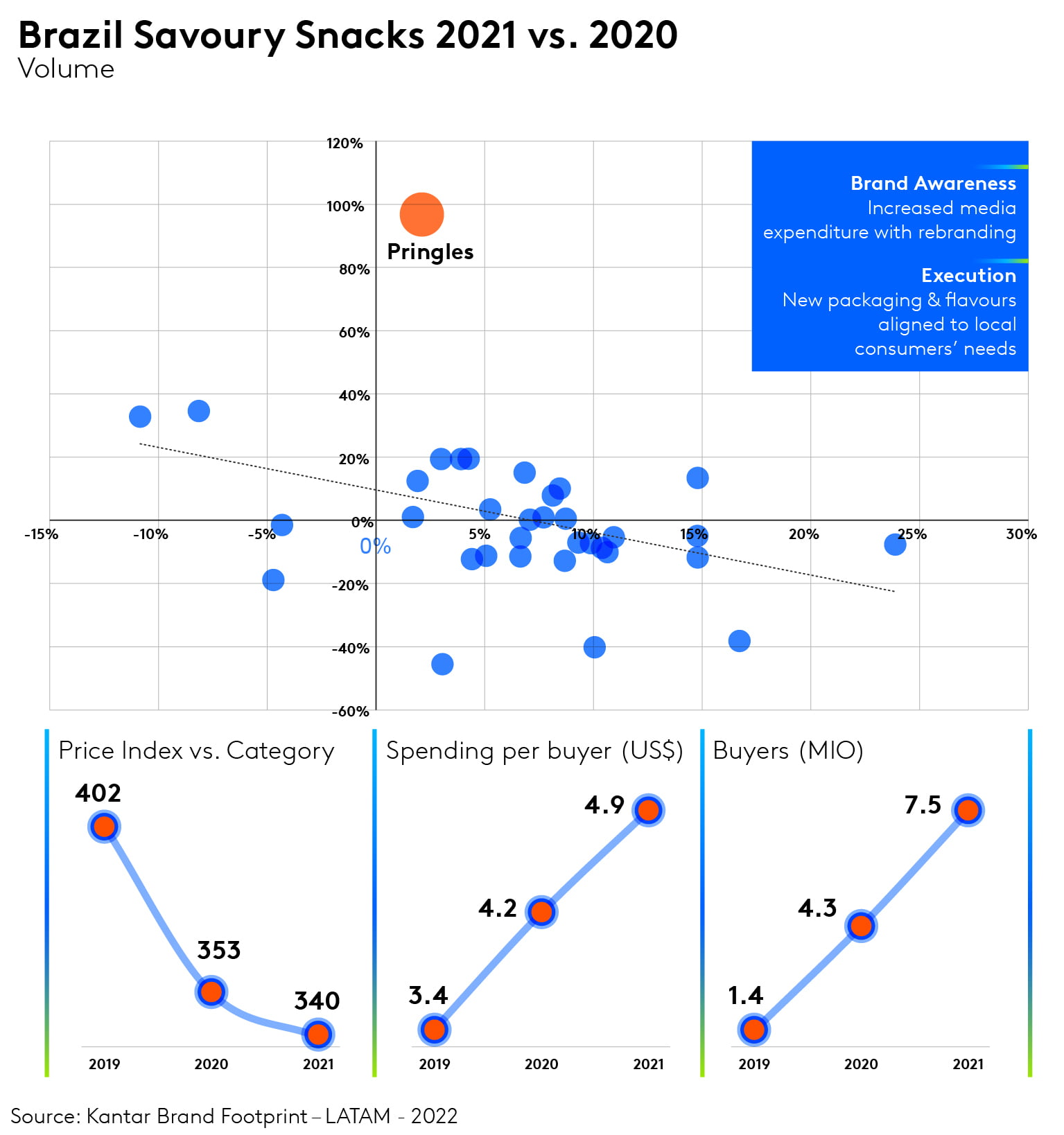

Pringles has stormed up the rankings in 2021, gaining more than 30 positions, thanks to a 59% rise in CRPs built on a combination of frequency (14.4%) and penetration (up 2.6 points to 9.5%) gains. A particular hotspot was Brazil, where it boosted investment in media to support a rebrand, new packaging and new flavours. This was combined with the opening of a new local factory, which enabled it to become more price competitive and attract more buyers. While still a premium product, it now indexes 340 against the category compared to 402 in 2019.

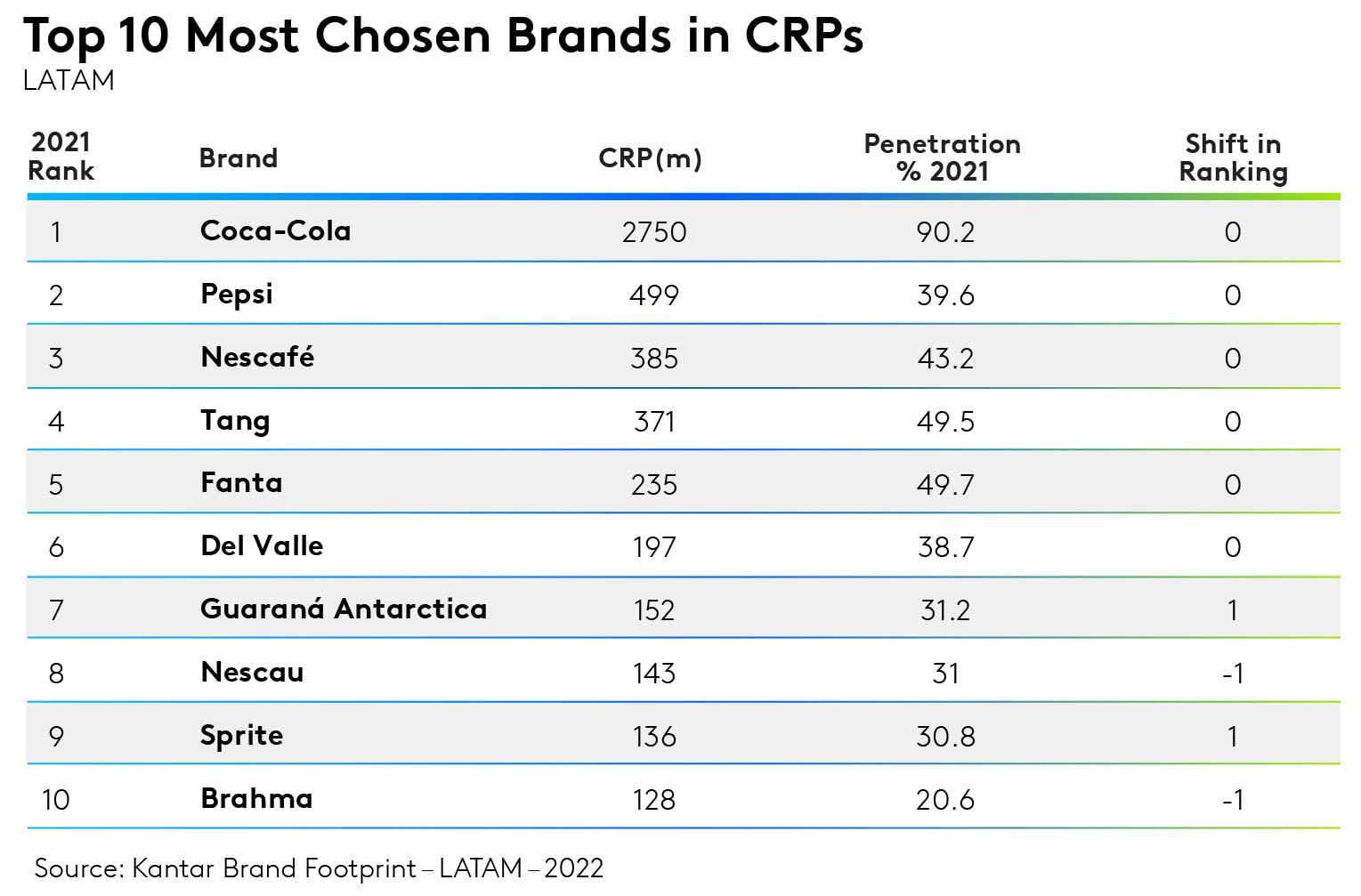

Much like the food sector, the beverages category has been relatively static at the top of the table. Coca-Cola is No. 1, with nearly six times as many CRPs as arch-rival Pepsi at No. 2. What changes there are happened at the bottom of the Top 10 with Antarctica Guaraná overtaking Nescau to gain the No. 7 place and Sprite beating Brahma beer to the No. 9 spot.

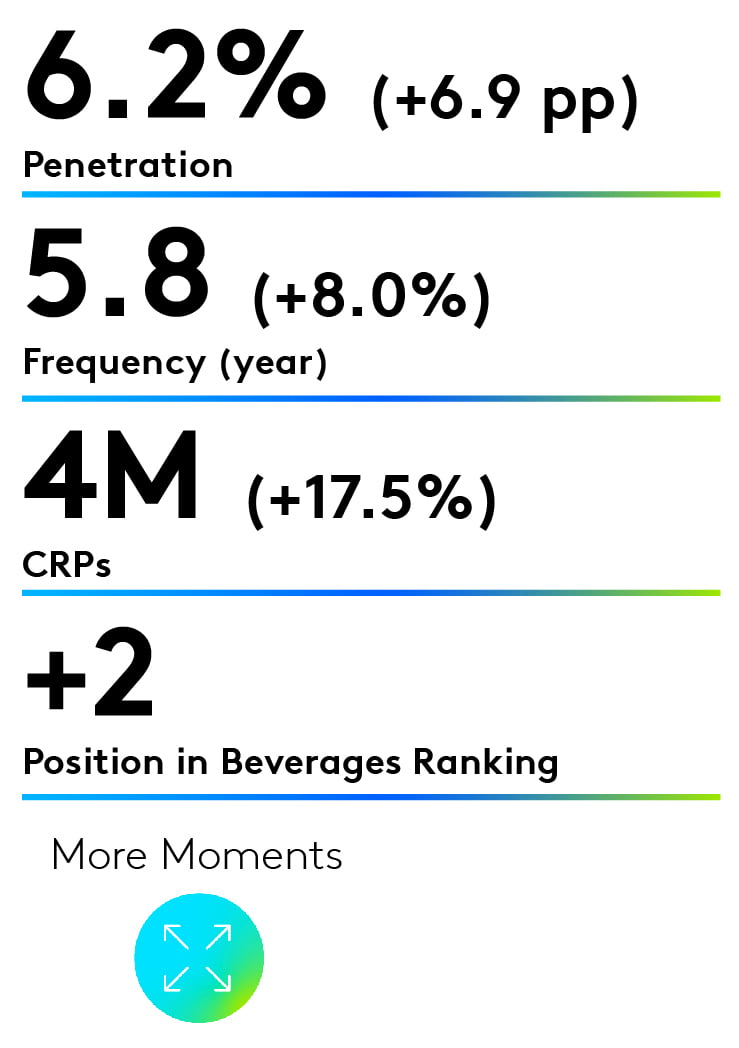

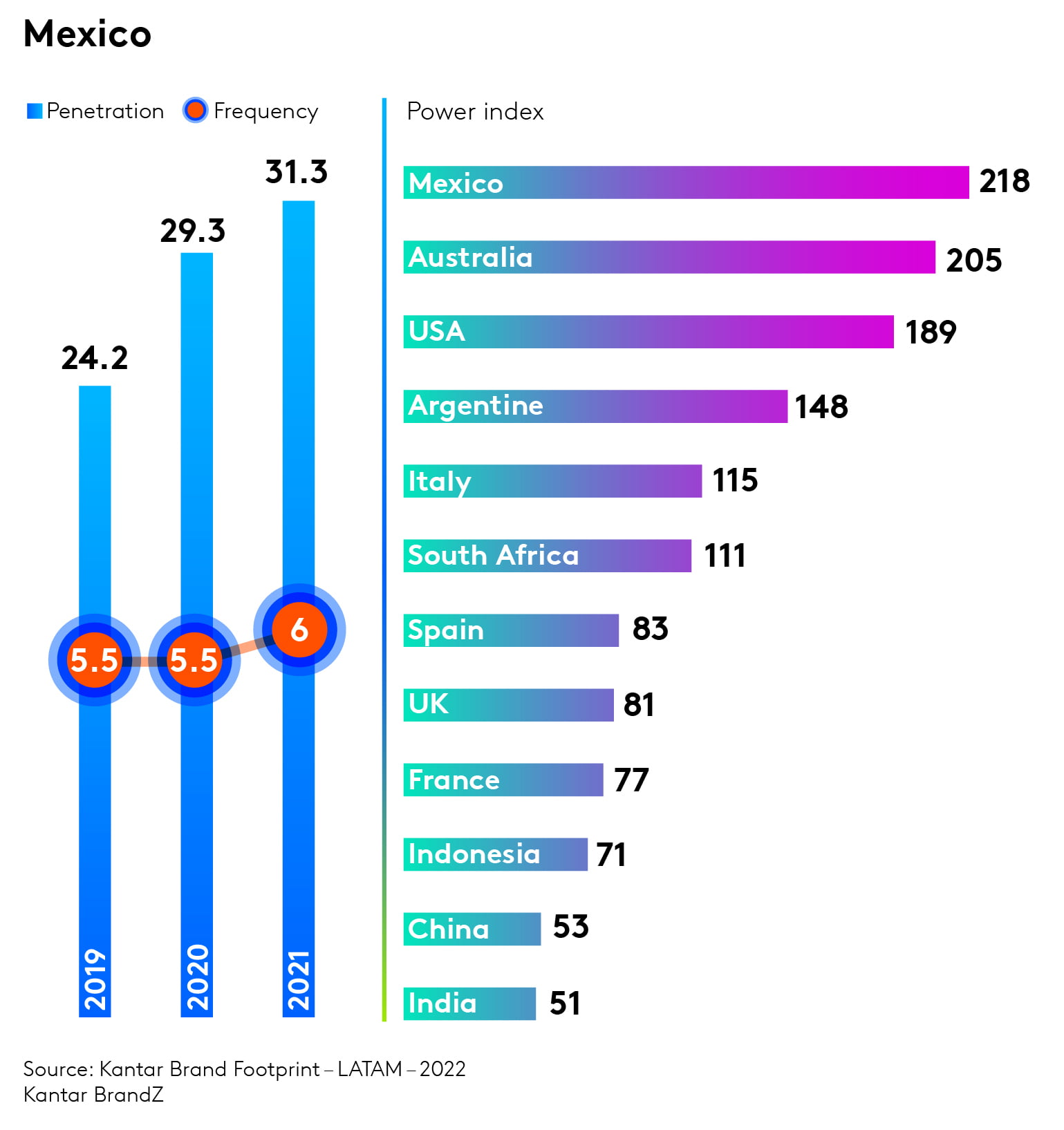

Corona faced potential disaster in 2020 as COVID-19 engulfed the world in a pandemic. While bars, pubs and restaurants were closed due to lockdowns, it was reported that consumers were busy Googling ‘beer virus’ and ‘corona beer virus’. The share price fell as investors panicked. The real story, however, was very different. The strength of Corona beer’s non-viral associations – sun, sand, a slice of lime – allowed it to become so much more than just its name. In Mexico, for example, a jump in grocery and liquor store sales had more than covered the 50% drop in restaurant sales. Across Latam, in 2021 we saw a significant rise in CRPs – up 17.5% – thanks to a boost in both penetration and frequency, with the latter rising 8% year-on-year.

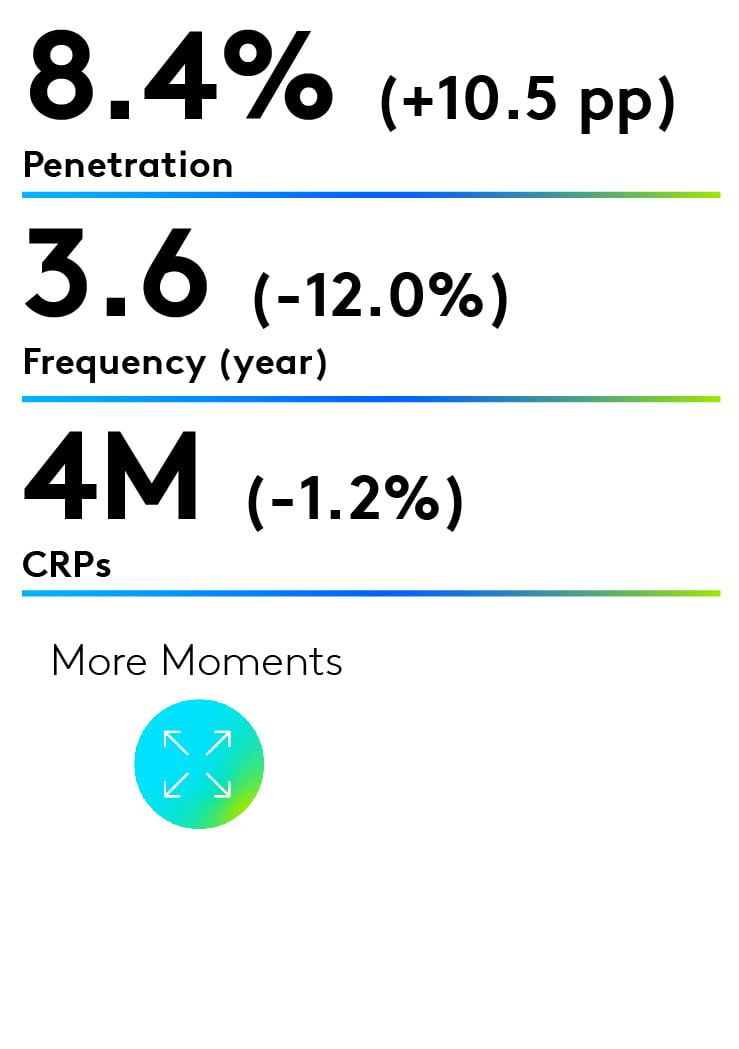

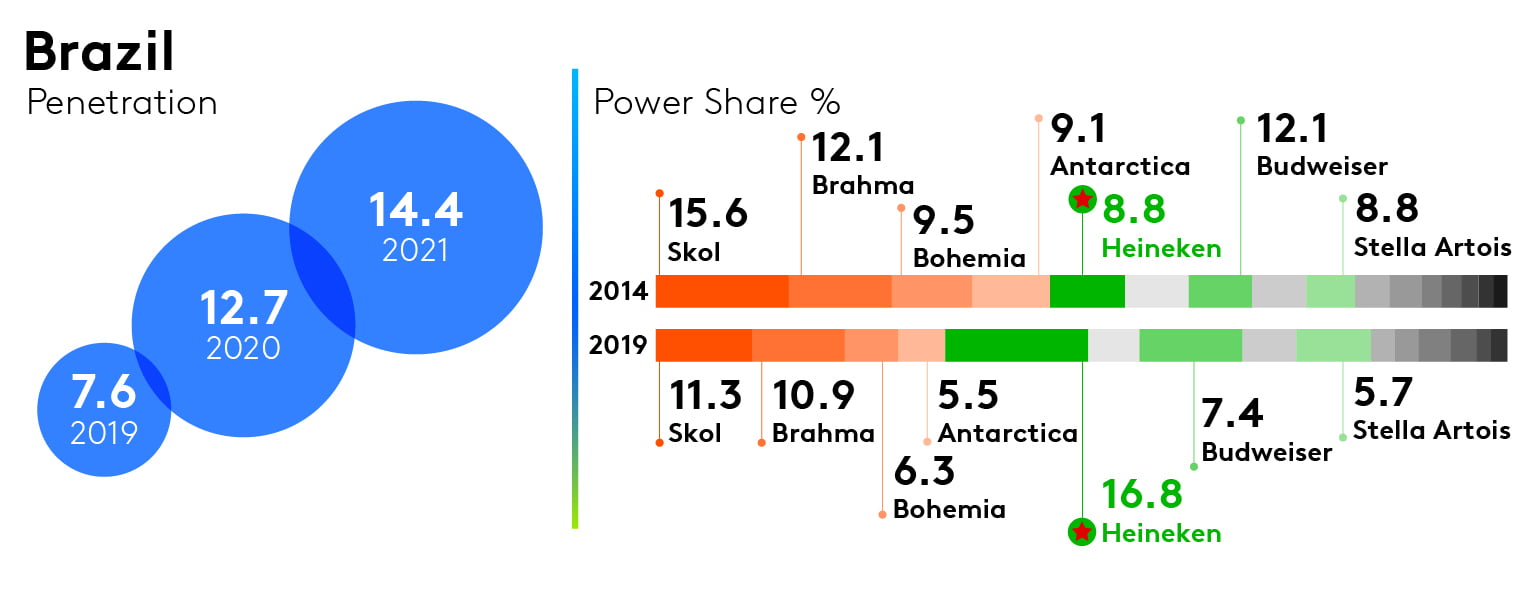

Heineken has grown brand equity over the past decade to lead the beer category in Brazil, displacing local giants Skol, Brahma, Bohemia and Antarctica. Heineken has used its status as an imported premium beer to win leadership in a category dominated by Anheuser-Busch InBev’s local brands by focusing on its premium malt ingredient. While ABI focused on pushing its own premium global brands Budweiser and Stella Artois, Heineken made itself both different and desirable through an association with night-time bars, the brand’s rich green colour and aspirational lifestyle. Brazil is now Heineken’s biggest market globally.

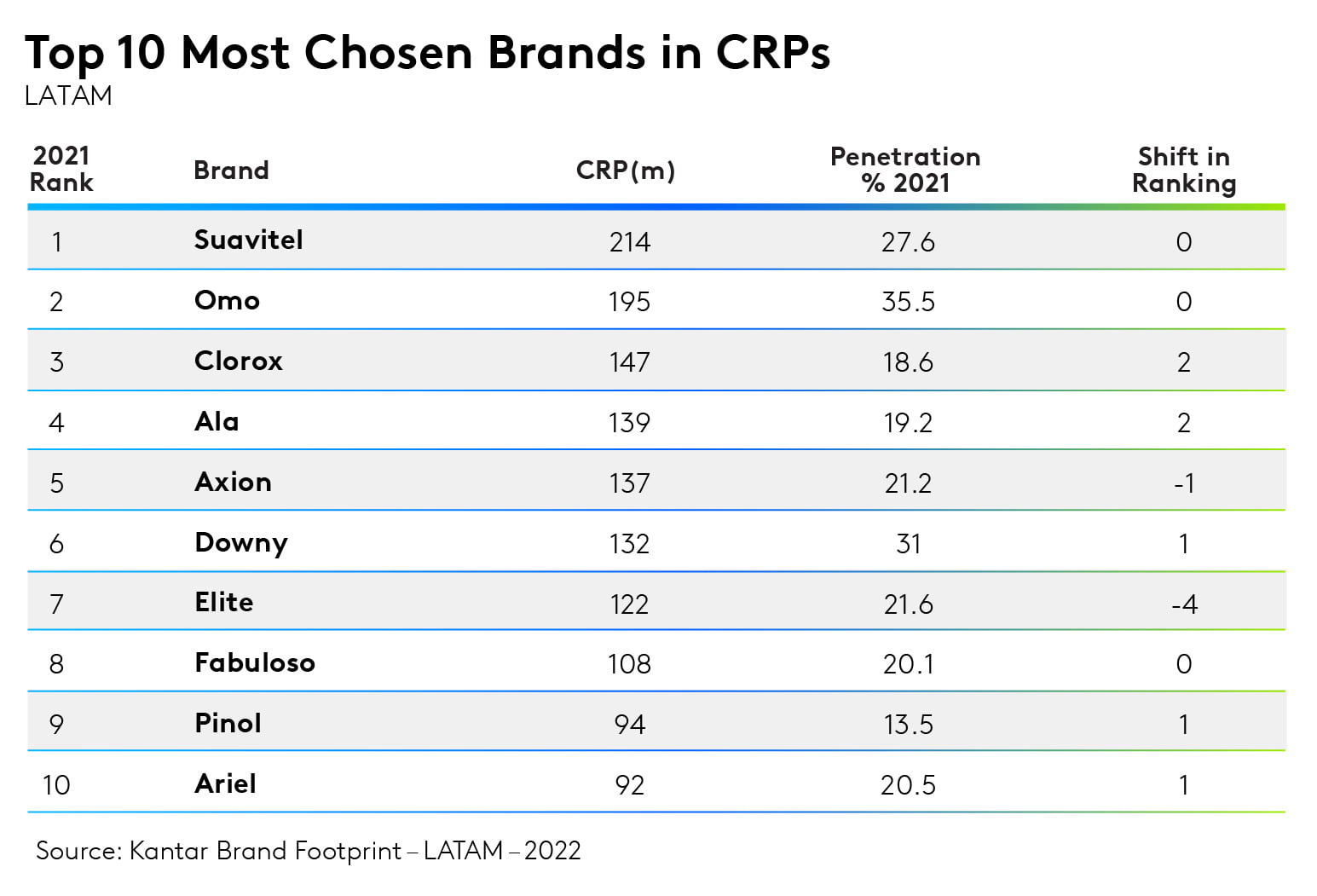

Home Care has seen more movement than other categories with Clorox and Ala both climbing two positions to No. 3 and No. 4 respectively. The big winner, however, was paper towel brand Nova, which boosted its CRPs by 27% and rose seven positions to No. 24. Nova has taken on rival Elite by targeting the C and D socioeconomic levels, which had previously seen paper towels as a luxury. The result is that Nova has displaced the ubiquitous yellow cloth as a cleaning tool. It’s also gained as consumers gathered post pandemic to celebrate various holidays with family and friends at home, helping it reach all demographic groups.

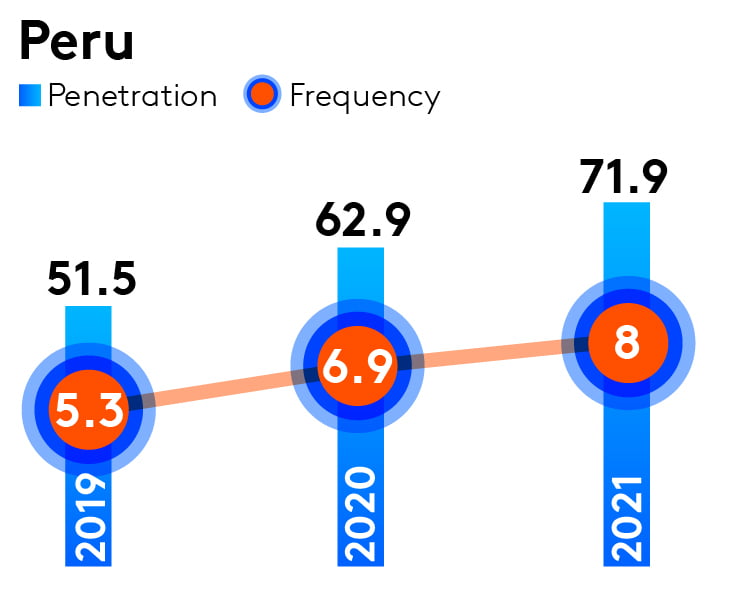

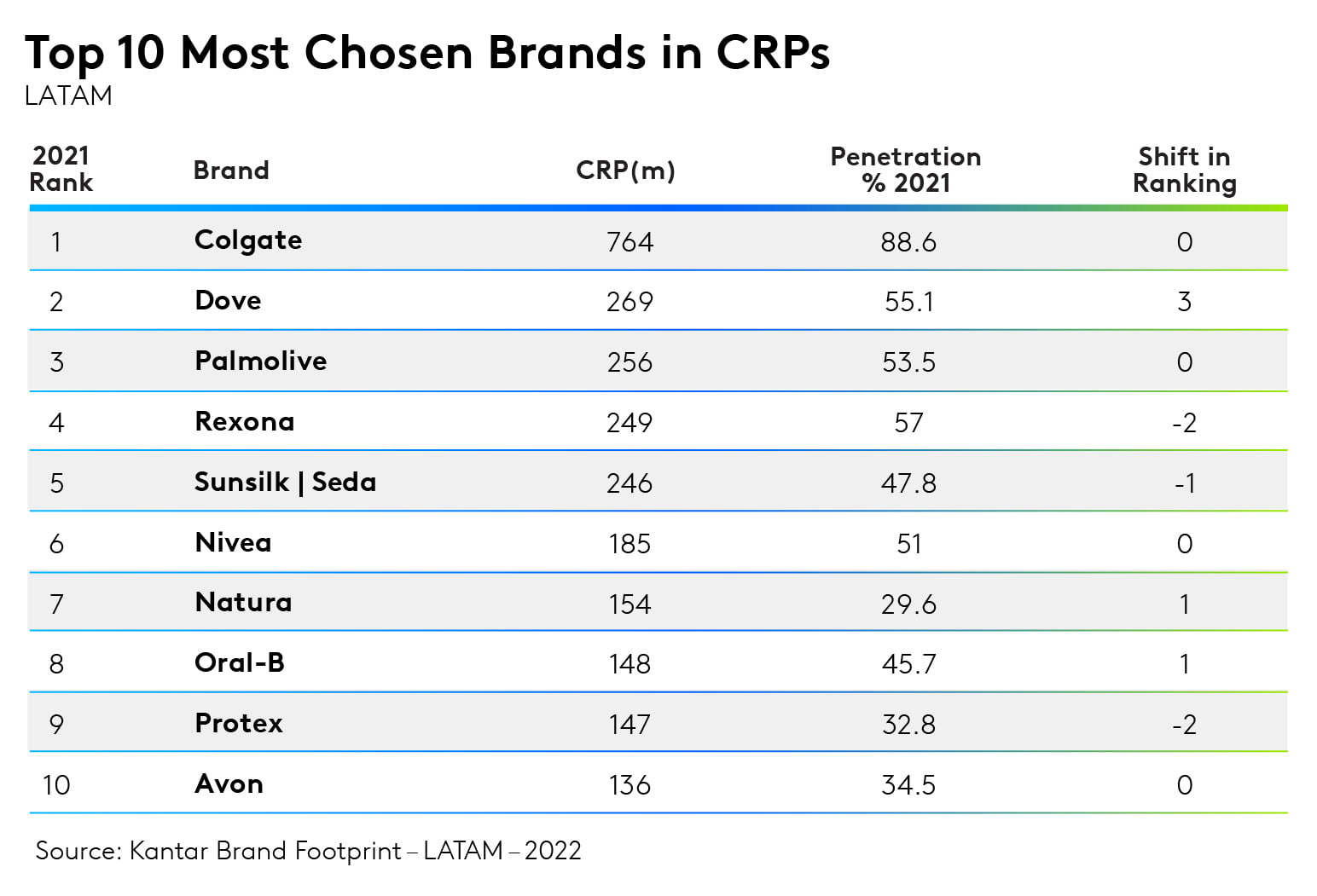

The success of Dove's Real Beauty campaign has helped drive overall category growth, as Dove rises three places. However, Colgate remains No. 1 in 2021. Natura and Oral B are also big winners. Listerine was the fastest growing brand by CRPs in Health and Beauty, with a rise of 16%, moving up six places to take the No. 36 spot in the category. Growth was driven by a combination of more buyers and more occasions. In Peru for example, Listerine has successfully reached more shoppers for the third consecutive year.

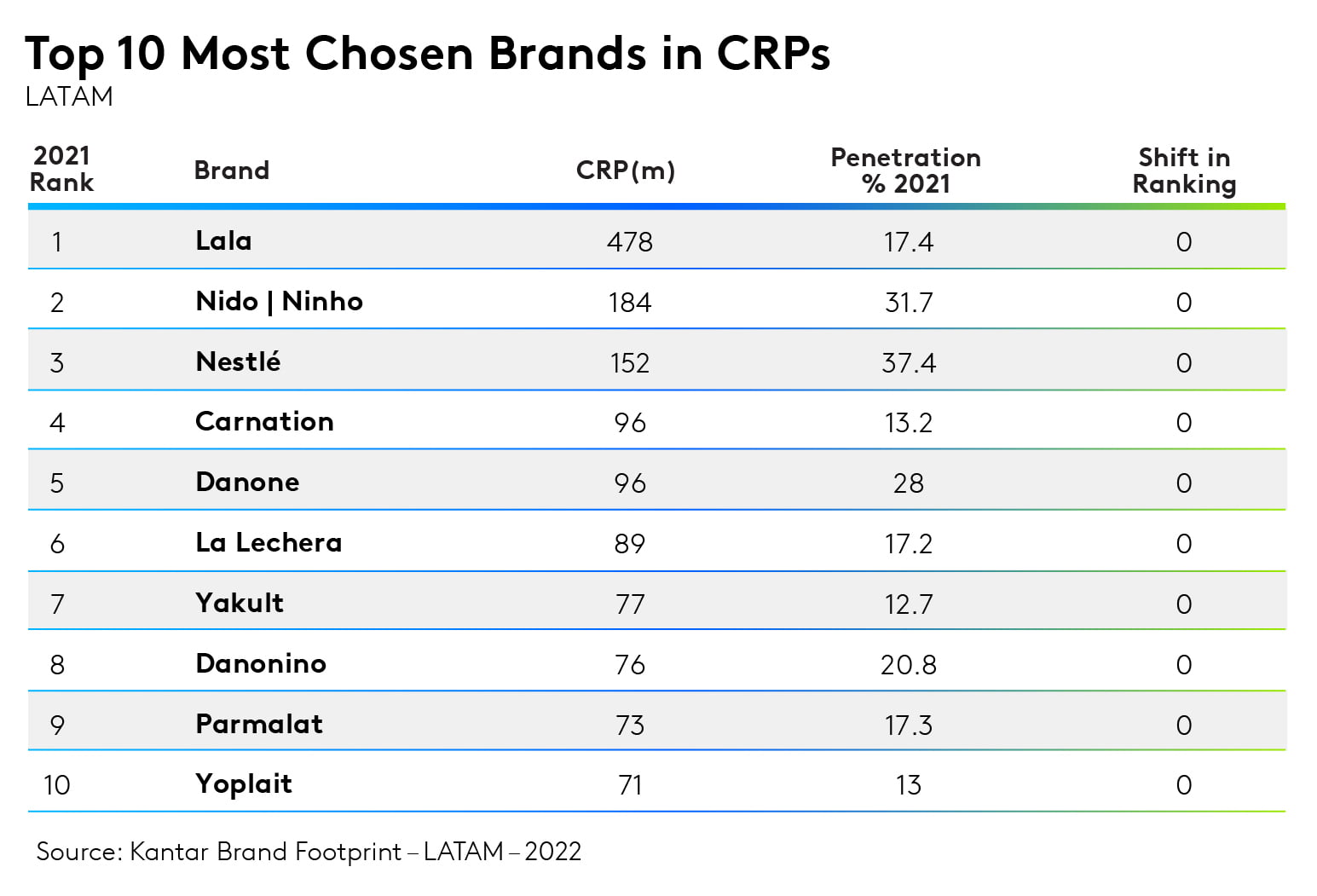

Local Latam champion Lala tops the category with 478 (m) CRPs, well ahead of rival Nido/Ninho in No. 2.It's been a year of no change in the Top 10, however Kraft nearly doubled (+92%) its CRPs to move up to No. 44 in the category, mostly thanks to a rise in frequency (up 14.3%). In Chile, penetration has reached close to six in 10 homes (59.5%) in one of the brand’s most impressive performances in the region. Cream cheese, in particular, was key to driving more moments for consumers to reach for the brand in 2021.