A roller-coaster ride for FMCG

We all know that Latam is not like the rest of the world. And when it comes to our economy, it is more varied and performance more fluctuating.

Inflation in 2021 was 4.3%, its highest level since 2011, although regional GDP has soared after a major dip due to COVID-19 in 2020. The expectation for 2022 is for economic deceleration , with the prospect that FMCG could be hit.

Each year of the decade has brought challenges, be they political, economic or social in countries across the region. The pandemic has also been an additional economic strain.

Such challenges mean the FMCG industry has seen periods of growth and periods of consolidation. When we track the sales of the Top 50 brands across our Latam markets, we see expansion in 2014 to 2016 coupled with decreases in 2019 to 2021.

Across the decade, sales value has declined 3% when indexed against 2012. This compares with the overall global performance of a 33% boost (worth $650 billion in additional sales).

A decade is a long time and the Latam of 2012 is very different to the Latam of today. For a start there are now more shoppers to target. The number of households has risen from 102m to 124m, a rise of 22m, regionally.

Overall, in Latam, brands were able to grow CRPs leading to a more competitive landscape. Add to this equation the number of regional and local brands, making it even harder to consistently remain on the ranking.

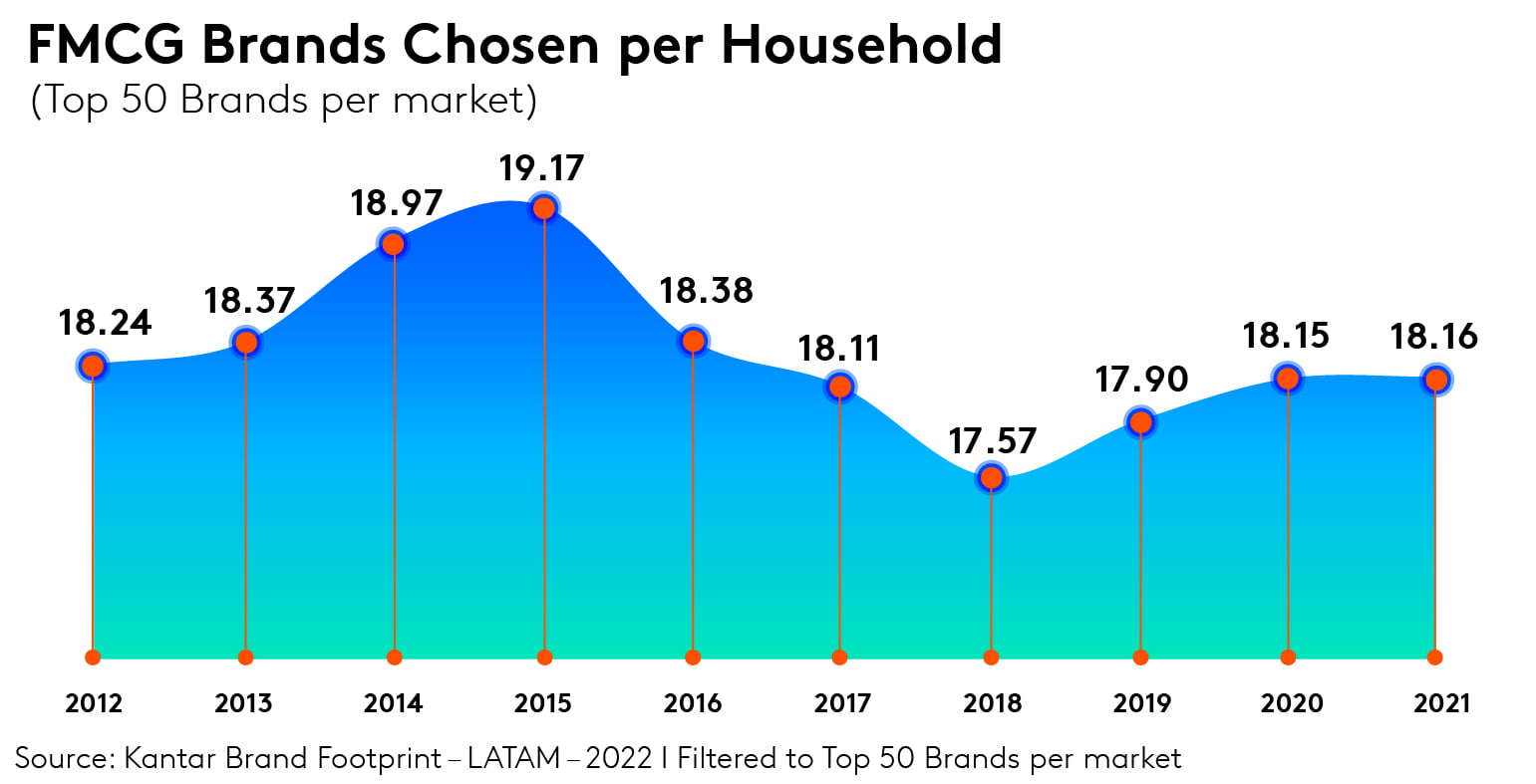

The number of brands being bought per household, however, has stayed pretty consistent. It has stayed at 18 in eight out of the 10 years. In 2014 and 2015, it hit 19.

For individual brands, the growth story has changed from year to year.

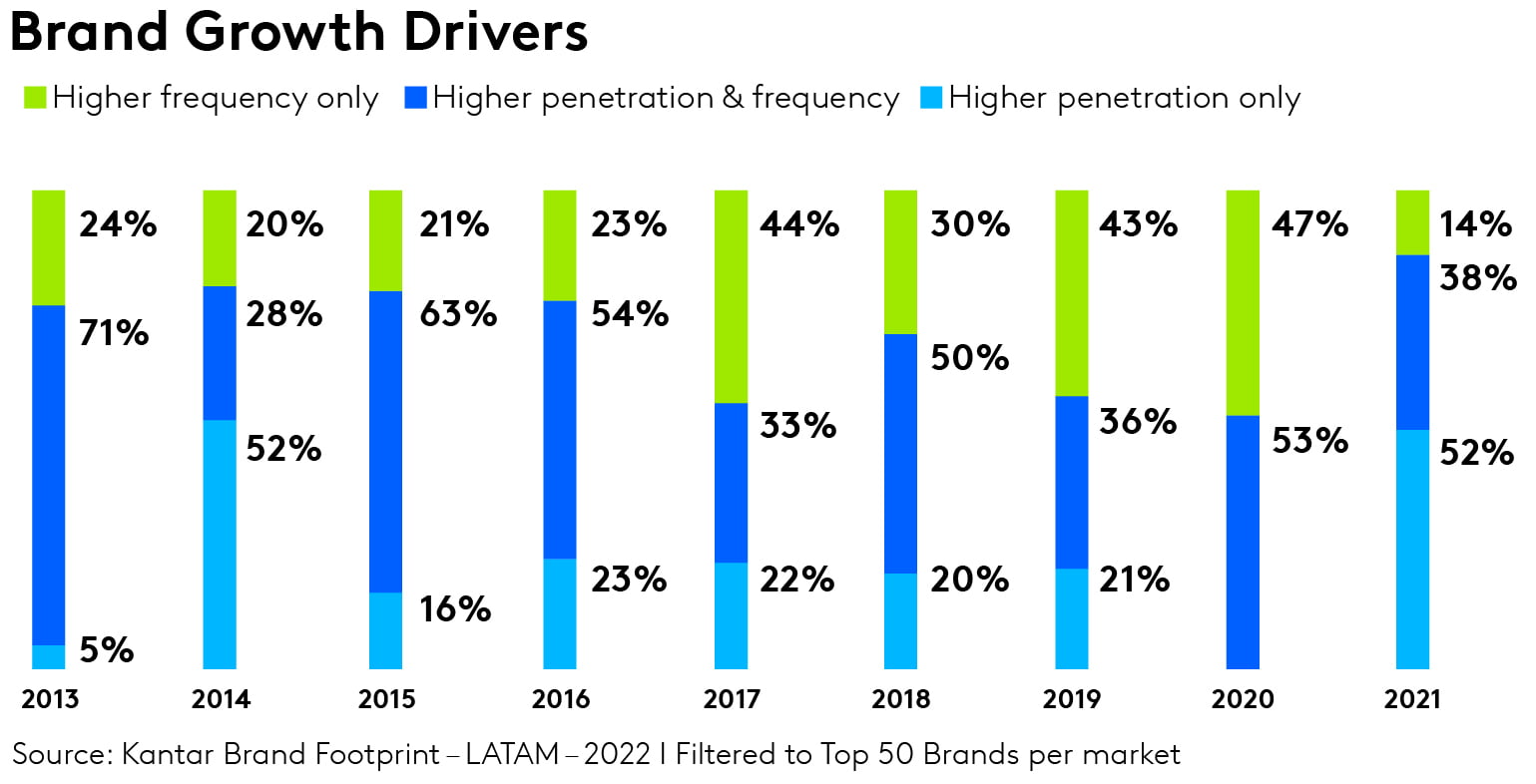

In 2021, more than half the growth (52%) came from boosting penetration but the previous year, 47% had been down to frequency alone and 53% to a combination of both frequency and penetration. Penetration alone is rarely the major driver for brand growth, although it did hit similar heights as 2021 in 2014.

When we analyze the performance of growing brands in our Top 50s for every market, we find that successful brands typically grow penetration by 1.1 points in a market every year. That means that our growing brands, which had a cumulative reach of 102 billion households in 2012, reached 124 billion in 2021.

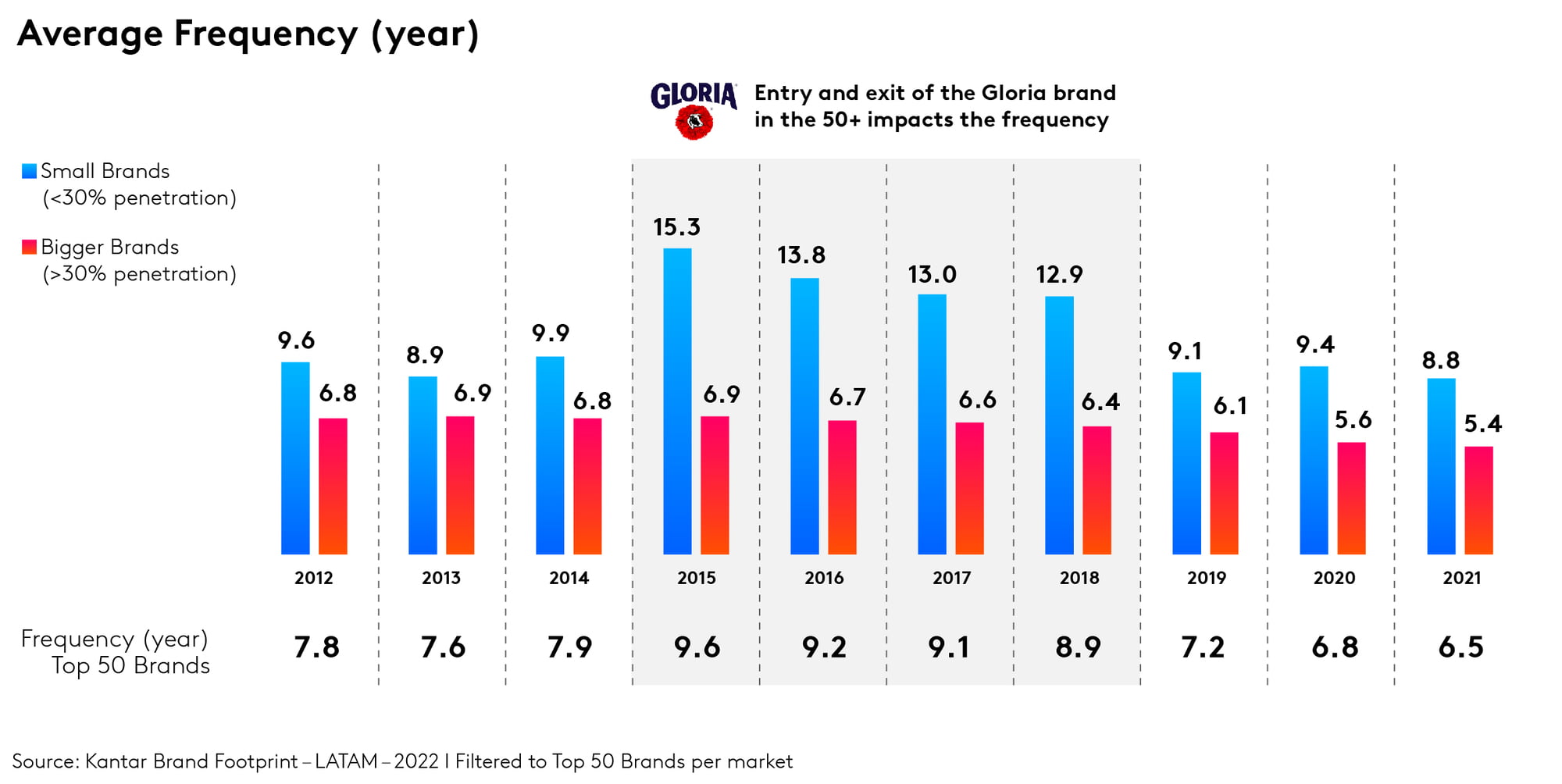

Frequency averages also tell a story, one that is different for small and large brands (those with more than 30% penetration). Analysis of all the Top 50 brands we’ve been tracking found that frequency has dropped from 7.8 in 2012 to 6.5 in 2021 overall. That may not sound much but across Latam’s billion plus households it represents a huge opportunity.

The story is also more challenging for larger brands, which have declined from 6.8 in 2012 to 5.4 in 2021. The story is still one of decline for smaller brands, but frequency is higher – 8.8 in 2021 compared to 9.6 in 2012.

Some of the biggest brands in Latam have lost frequency – Coca-Cola is down from 32.4 to 25, Colgate has fallen from 8.5 to 7.1 and Bimbo has dropped from 22.4 to 14.7.

Some brands have bucked the trend, however. Oreo has boosted frequency from 2.7 to 2.9 since 2017, similarly Lux recorded 3.2 in 2021, up from 3.1 in 2017.

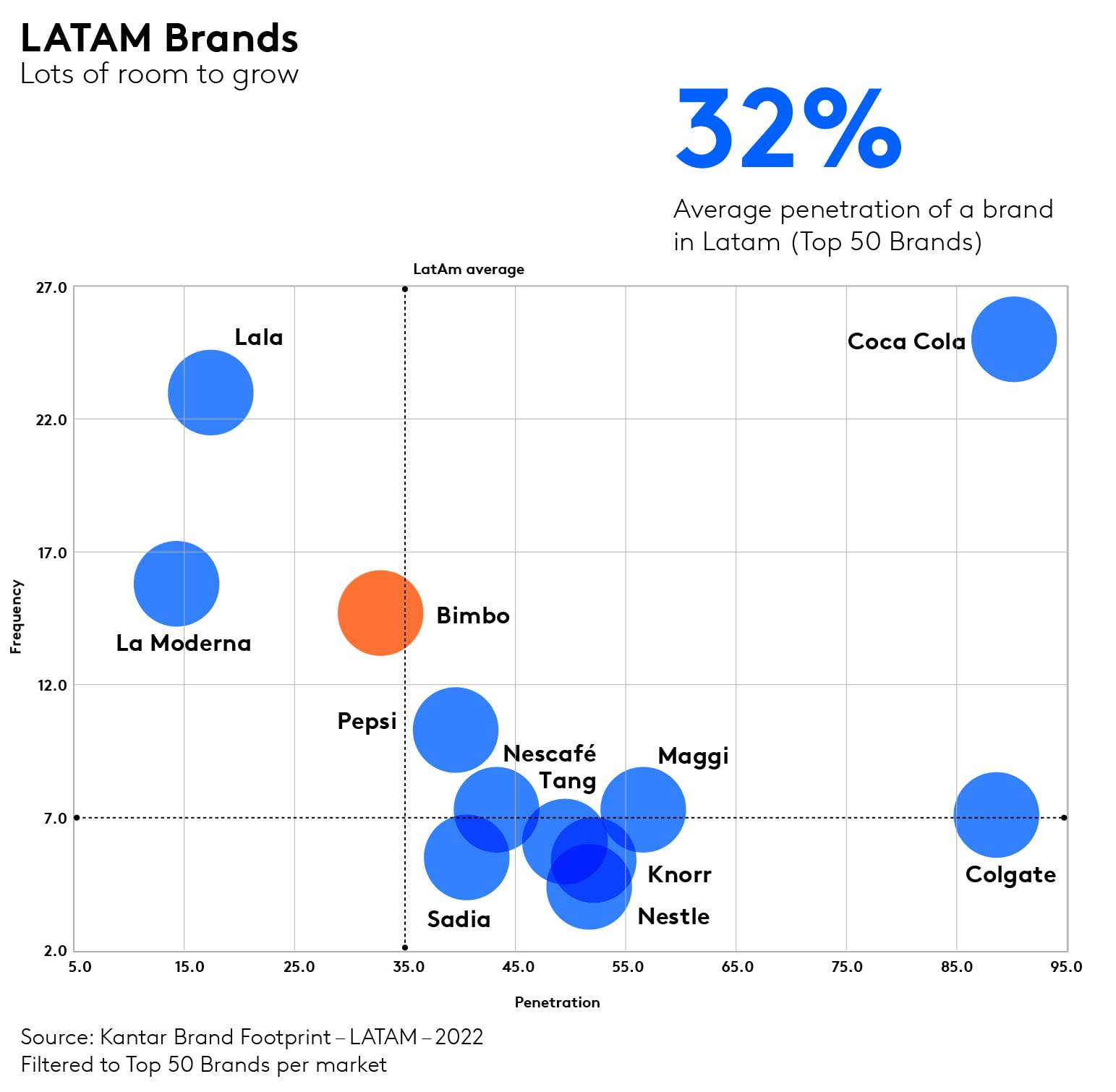

There are huge opportunities around both penetration and frequency. The average penetration among our top 50 brands in all 14 markets is 32%. And the truth is that while some brands are beating the average, many are not.

Lala scores 23 on frequency, for example, compared to a regional average for the top 50 of 6.5, but is much lower when it comes to penetration – scoring just 17.4, compared to an average of 36.3.

Only the region’s No. 1 brand – Coca Cola – beats the average for both by some distance. For all brands there is huge scope for growth.

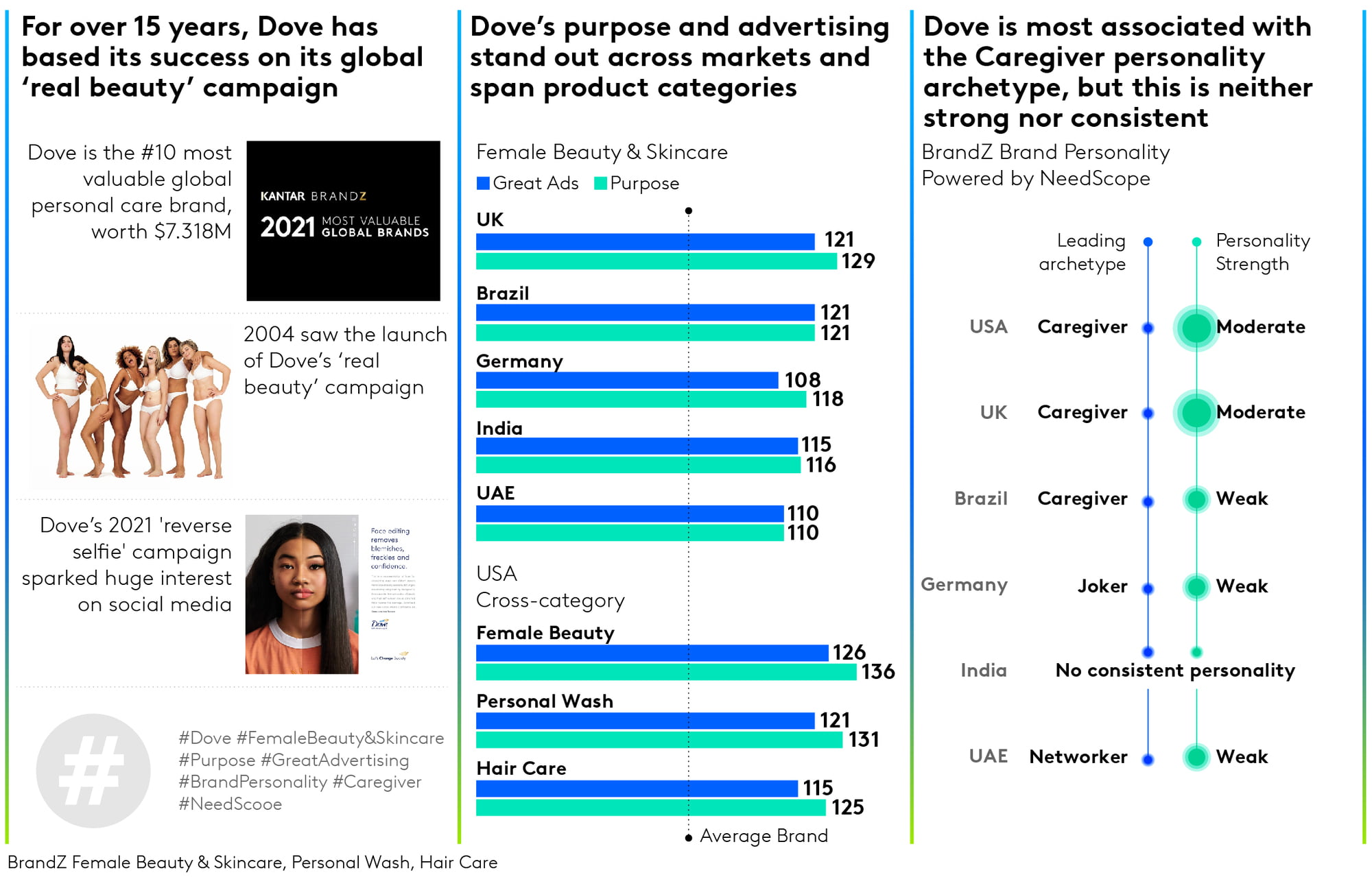

Global change happens differently in Latin America for brands as well. The timescale for consumer response and customer base expansion is different. One example is Dove. The brand has been one of the global success stories of the last decade, achieving constant growth. In Latin America, however, the growth of the brand has taken longer, accelerating mainly in the last few years.

Around the world Dove has recorded 10 years of growth by consistently finding more shoppers. Its ‘Real Beauty’ purpose and advertising stands out by creating an emotional bond and helping expansion into new categories. That global success is echoed in Latam where it recorded its best-ever results with 67m shoppers, up 41%, and 55% penetration. Dove continuously invests in innovation through new categories or new targets, such as male grooming. This helps it reach more shoppers in Latam, where it grew its CRP by attracting more buyers to its existing customer base.

It’s No. 13 in our Latam ranking.