01

FMCG

SHOPPERS MATTER

Understanding and Empowering Choices

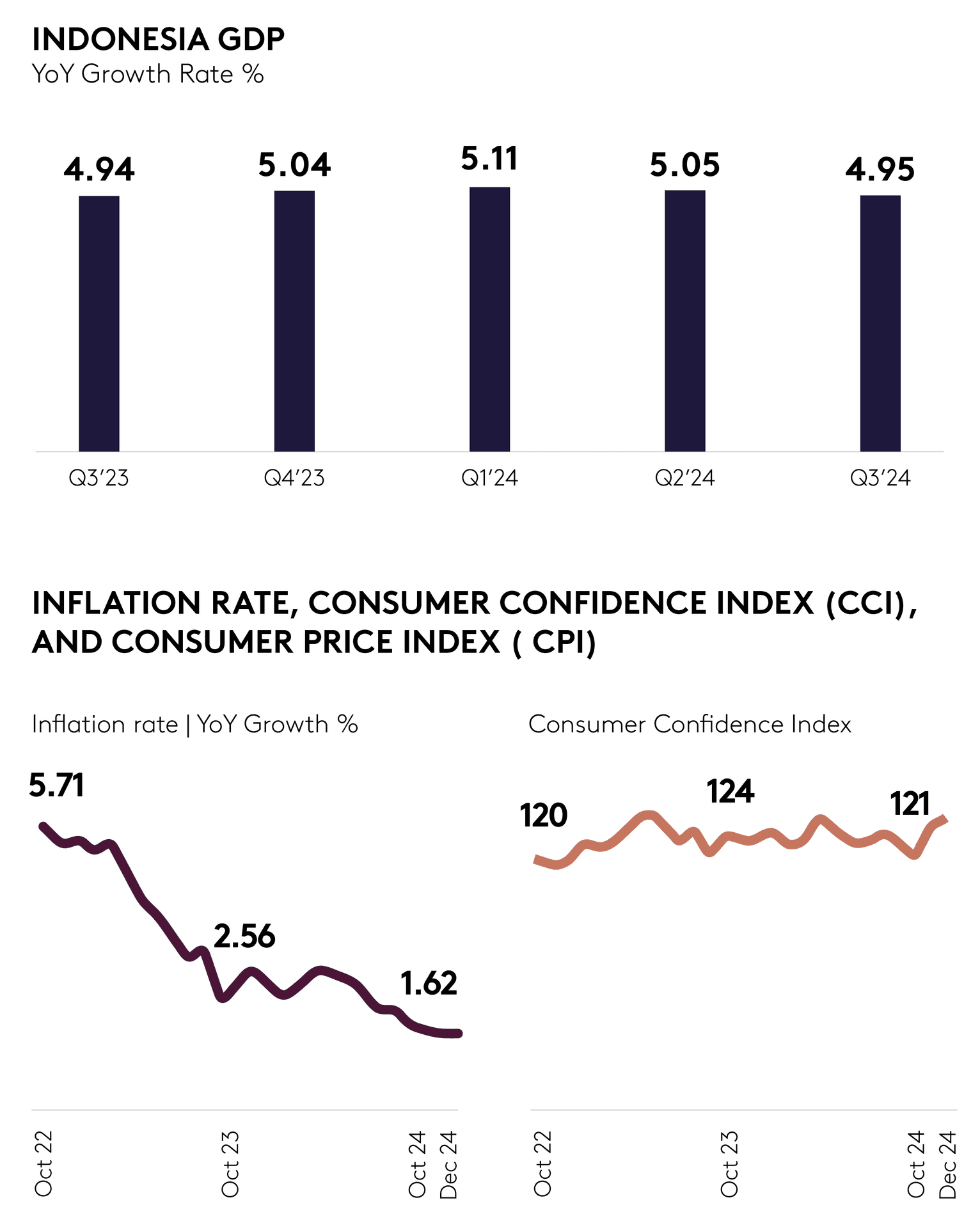

As Indonesia enters 2025, the FMCG industry continues to be a cornerstone of the country’s economic and consumer landscape. With steady GDP growth, controlled inflation, and a stable Consumer Confidence Index, the overall economic climate appears promising. However, these macroeconomic indicators belie the nuanced challenges and opportunities across various socio-economic segments (SES). Shoppers remain at the heart of this dynamic, as their priorities, behaviours, and coping mechanisms shape the FMCG sector's trajectory.

This report explores the current state of FMCG in Indonesia – highlighting how SES, regional trends, and external factors influence shoppers' decisions – and the outlook for 2025.

Indonesia’s economy continues to hold steady with value growth of 5% , a rate that has remained unchanged for the past two years. With no significant improvement in GDP growth, consumers’ confidence has also stagnated, despite the inflation rate slowing down. As household spending contributes more than half of the increase in Indonesia’s GDP growth , spending growth is fundamental to the overall economy.

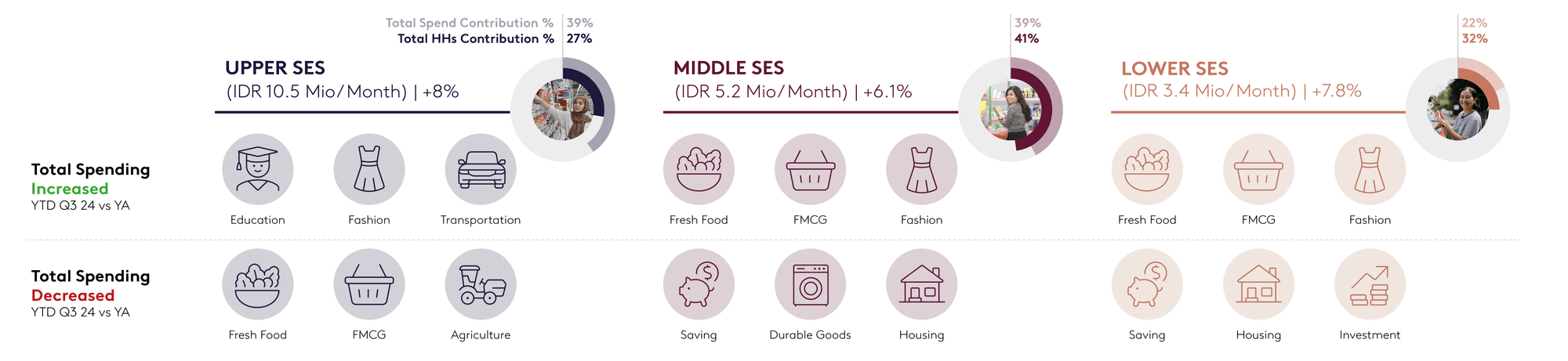

Looking deeper into Kantar’s expenditure survey data, household spending has grown 7.6% over the last year, driven by upper-class shoppers. With more cash outlay, these consumers are able to allocate more of their budget to categories beyond food and other necessities, embracing premium and discretionary categories that cater to lifestyle enhancement.

On the other hand, middle-class spending growth is the slowest, suggesting that this consumer group may be exposed to bigger challenges than others. They focus their expenditure on necessities, and allocate less to saving and to purchasing durable goods, suggesting that the drive to meet basic needs is dominant. Likewise, lower-class shoppers are also designating more spend to necessities, and saving less.

In short, spending priorities vary across social groups, and economic pressures are hitting mid-to-low SES shoppers hardest, forcing them to find ways to become more resilient and thrive.

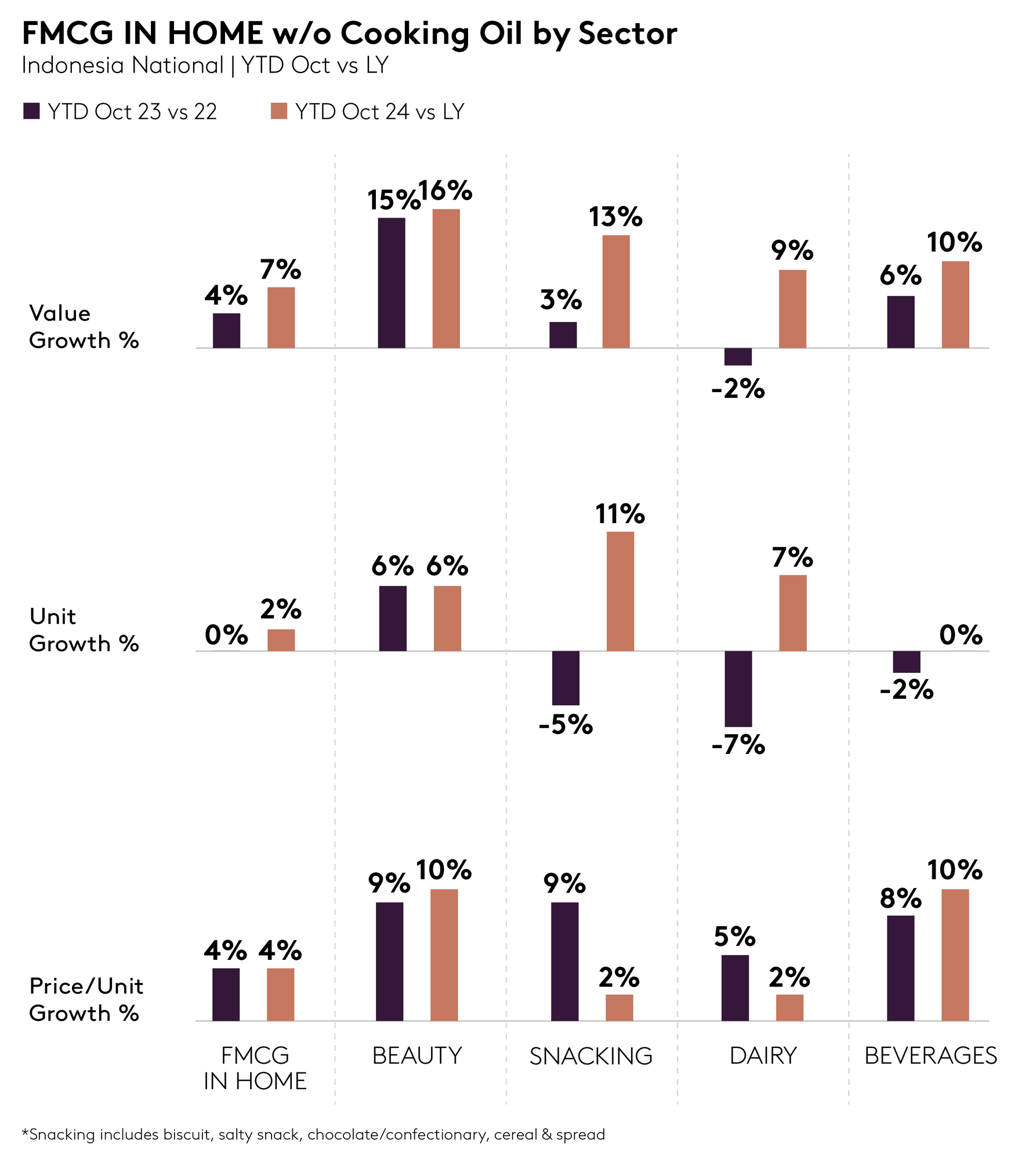

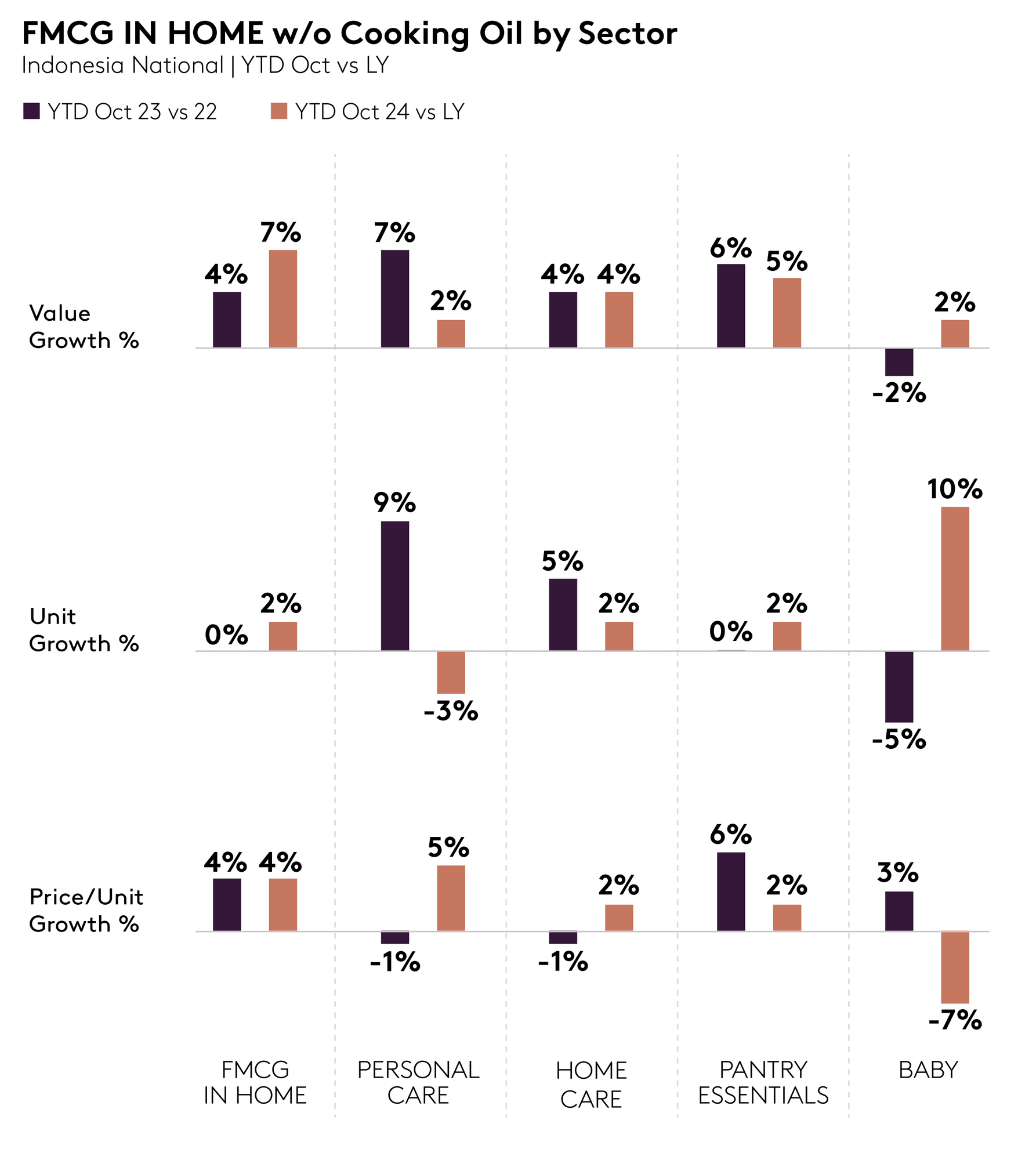

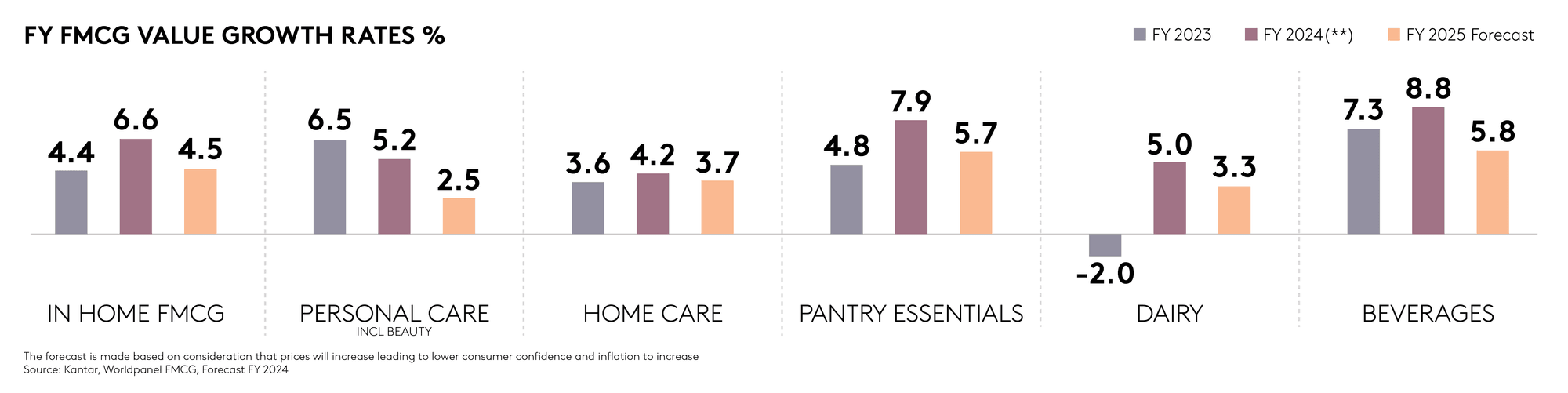

Indonesia’s total FMCG value grew by 7% over the last year, mirroring the overall rise in household expenditure. This was primarily driven by the beauty sector, and the rebound in festive-driven snacking and dairy categories.

Beauty has sustained double-digit growth over recent years, surpassing total FMCG growth in 2024 at 16%. As both price and volume are increasing, this suggests a higher willingness to spend more on beauty products, presenting brands with an opportunity to drive premiumisation. Unlike beauty, growth in the personal care sector is more limited, with shoppers opting for better value for money by upsizing their purchases.

Another growth driver in 2024 was the rebound of festive spending in the snacking and dairy sectors. This helped snacking foods – mainly biscuits – to achieve double-digit growth of 13%, a marked uplift compared with the previous year’s increase of 3%. Likewise, the dairy sector has turned a decline of -2% into growth of 9%. Brands in these sectors can leverage this momentum to create more occasions beyond the festive season, to drive more sustainable growth throughout the year.

On the other hand, however, some FMCG categories face challenges as market dynamics shift. Home care and pantry essentials value growth are stabilising, reflecting their status as staple categories in the household. Shoppers are only able to cope with the price increases, and therefore are making no significant increase in basket size. For beverages, substantial price increases for some commodities such as coffee beans were the only driver of growth. This could herald an opportunity for brands to provide better value for money options, by supporting big packs or encouraging higher consumption with multipack offers.

The baby category is also under pressure, with shoppers adjusting their spending by downsizing to smaller packs to maintain affordability. This challenge highlights the importance for brands to make their products more accessible by extending the pack size assortment.

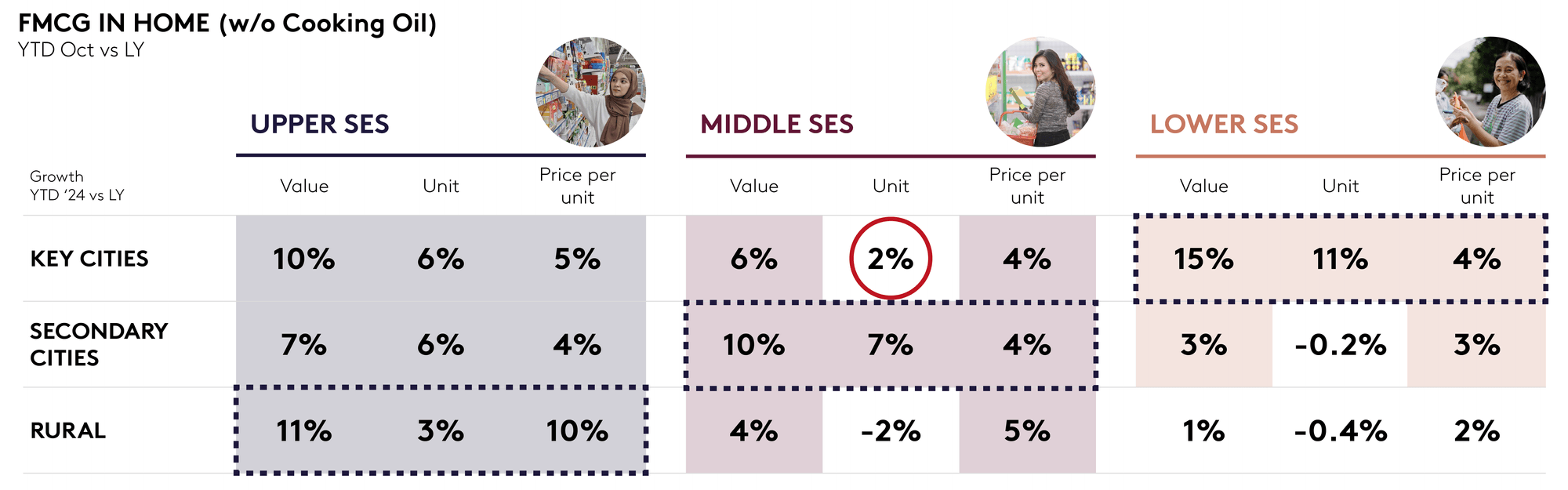

The range of different coping strategies employed across socio-economic groups highlights the varied impact of economic pressures. Middle-class households, particularly in key cities, face significant challenges such as widespread layoffs and financial constraints. However, opportunities remain for brands to target middle-class consumers in secondary cities, where basket sizes still show potential for growth.

For lower-class households, government support has bolstered purchasing power, particularly in urban areas, enabling them to prioritise spending on necessities, including FMCG products. Meanwhile, upper-class households continue to experience modest growth in spending and basket size, presenting a distinct opportunity for brands to cater to their evolving preferences. These dynamics underscore the need for region-specific and group-specific strategies.

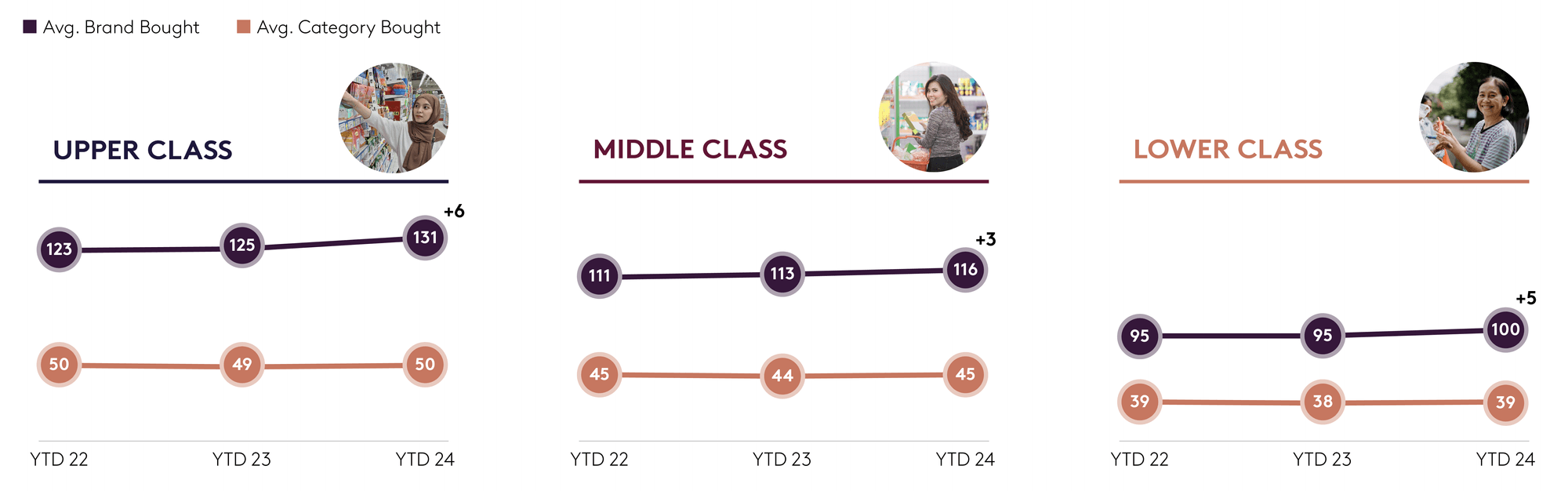

In terms of brand exploration, middle-class shoppers have become less experimental due to spending constraints. To address this, brands can focus on enhancing affordability to mitigate the impact of price increases. Conversely, other shopper groups are becoming more explorative, seeking better value for money – for example, larger pack sizes at the same price – or embracing innovation and novelty, resulting in an increased variety of brands in their shopping baskets.

From a category perspective, spending patterns across social classes show similarities, with a growing allocation toward beauty products such as face moisturisers and lipsticks. This reflects the so-called ‘lipstick effect’, where beauty serves as an affordable luxury and a form of self-care, particularly among younger shoppers seeking small indulgences amid economic pressures.

Additionally, categories like biscuits and instant coffee are gaining traction across cohorts, signalling a shift toward in-home snacking and indulgence. With economic pressures leading to reduced spending on dining out or café visits, shoppers are recreating café-style experiences at home with ready-to-drink beverages and ready-to-eat snacks. Brands can leverage this trend by optimising in-home occasions and introducing innovative products that bring excitement to the market.

The varying coping methods witnessed across social classes in Indonesia present both challenges and opportunities for brands. Understanding the dynamics of each sector and category is crucial to comprehending how shoppers adapt to the changes they face. This knowledge will enable brands to develop more effective go-to-market strategies to recruit more shoppers and increase basket size.

To engage middle- and lower-class shoppers, brands need to focus on offering better affordability and improved access to premium products. Reaching upper-class shoppers, meanwhile, may be achieved more effectively by emphasising value for money and clearly justifying the benefits of premium pricing.

Looking ahead to 2025, additional macroeconomic factors are likely to intensify existing challenges, potentially constraining FMCG spending. Our advanced analytics forecast indicates slower growth across FMCG sectors, suggesting that shoppers may adopt more cautious spending habits in anticipation of these challenges.

In this context, it’s important for brands to develop a deep understanding of shopper behaviour, adapt to shifting dynamics, and proactively address challenges. By doing so, they can position themselves to navigate uncertainty and drive growth this year.