02

FMCG IN INDONESIA 2025

Discover Growth Opportunities Amid Economic Pressures

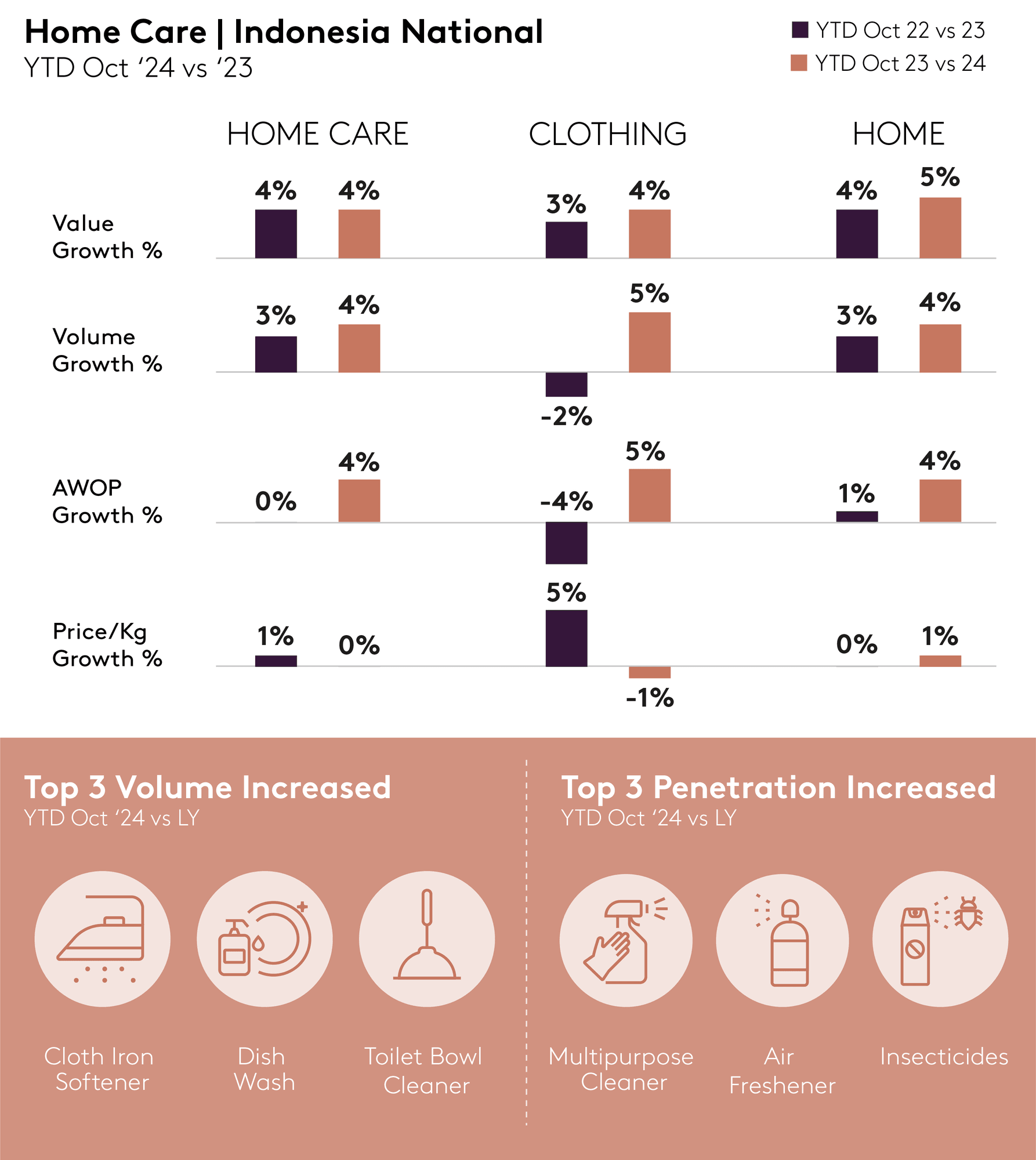

The home care sector in Indonesia experienced value growth at the same rate with last year of 4%, driven by higher basket sizes. This trend has been particularly prominent among middle-class consumers, and is seen in both the clothing and home segments, suggesting that this cohort has a need for affordability as they adjust how they allocate their FMCG budgets. Meanwhile upper-class shoppers, with their higher cash outlay, are more open to exploring and adapting to innovations in the market, especially within clothing, such as new products that offer added eco-friendly benefits.

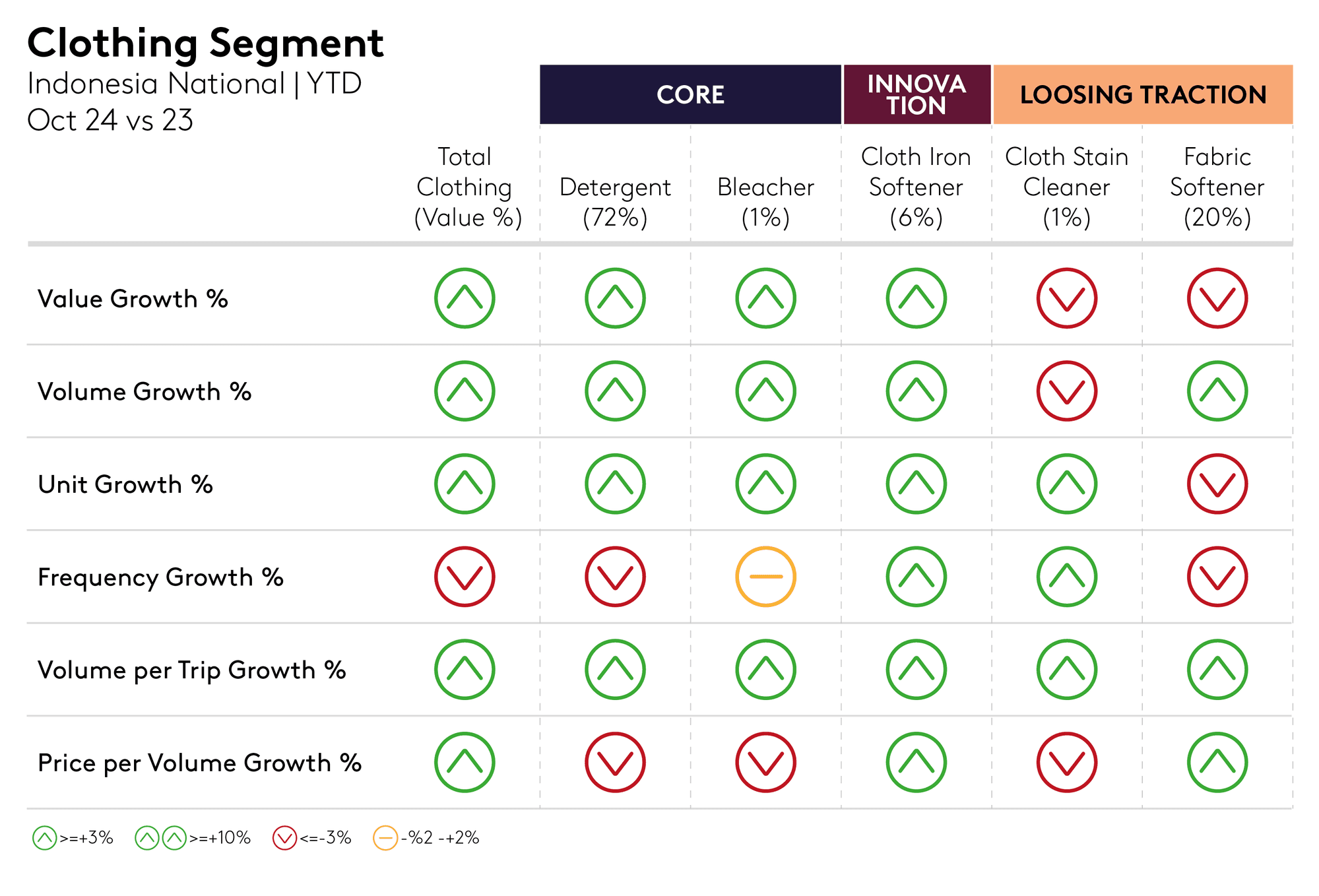

In the core clothing category, the detergent segment needs to bring excitement to shoppers. Some brands are managing to recruit buyers by offering all-in-one cleaner and softener to increase functionality, while certain newcomers are introducing features that are eco-friendlier and gentler for the skin. Although bigger pack sizes might offer better value for money, sachet packs remain attractive to shoppers, enabling them to manage their usage dose. This indicates that all newcomers that provide an extended assortment through sachets have the potential to increase their penetration. In short, shoppers are open to novelty if it fits their affordability and accessibility requirements. To meet basic needs in the clothing category, detergent brands seeking to win more buyers need to combine the right price-pack strategy with improving accessibility.

For instance, one newcomer in the liquid detergent segment had a strategy of offering premium bottle formats for affluent shoppers in the first launch phase, and selling mostly in modern trade. Liquid detergent might be perceived as more premium than powder, but the brand managed to extend accessibility by launching sachet packs and selling in general trade. The sachet format grew faster than the bottle pack, demonstrating how accessible premium products can enlarge the buyer base and foster brand growth.

Another well-received innovation in the clothing segment has come from cloth iron softener. Although the size of the category is much smaller than detergent, the way to win shoppers is no different: brands that offer better functionality and affordable premium products are likely to do well. Likewise, in the declining fabric softener segment, brands that can increase accessibility to their premium ranges and reach shoppers with sachet packs in general trade channels can boost penetration and still grow.

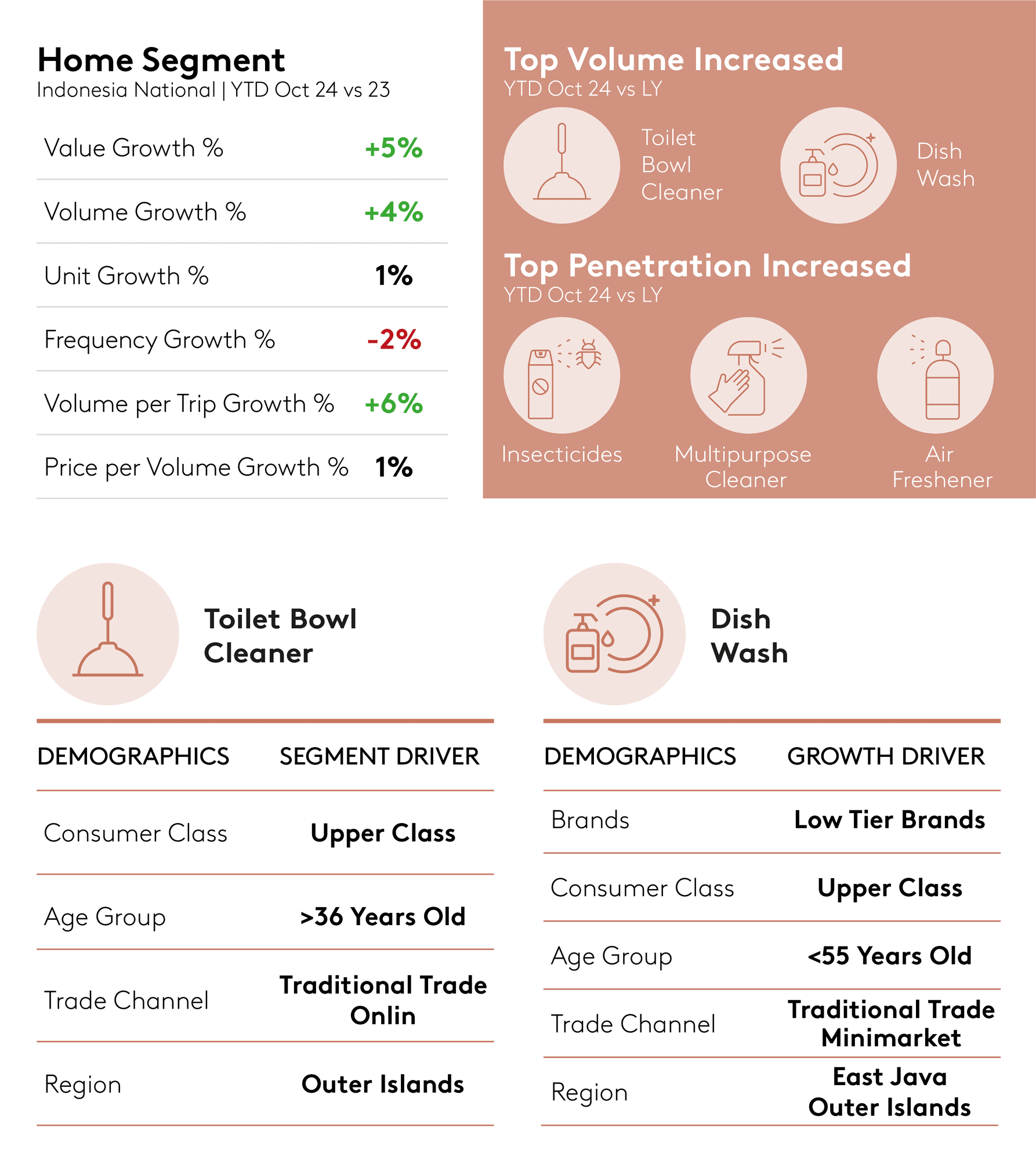

Growth in the home category is being driven by bigger basket sizes, suggesting that upsizing purchases to get better value for money is prominent, especially in the dishwash segment, the backbone of this category. The most notable growth in dishwash comes from upper-class shoppers and those aged under 55, mainly in East Java and the outer islands.

Innovation in the home category is well received by consumers when it introduces increased functionality, such as in multipurpose cleaners. New assortments which offer multiple functions, such as dishwash and detergent in one product, are appreciated and help to enlarge brands’ buyer base. On the other hand, in the insecticide category, ensuring that the core assortment delivers effective benefits might work better to drive growth.

In a nutshell, growth opportunities in the home category lie in embracing multifunctionality. Products that serve multiple purposes or accommodate multiple needs can gain real traction with consumers.

Despite the challenges posed by macroeconomic pressures, the home care sector remains an essential part of Indonesian households’ FMCG baskets. The category will continue to be a staple for shoppers, but will require adjustments if brands are to navigate these pressures effectively. In particular, they must strategically manage their assortments to maintain a well-balanced and effective portfolio.

Shoppers are also open to innovations that offer clear, tangible benefits. Introducing a premium assortment can also serve as a strategic advantage if the brand extends availability to general trade channels and offers sachet packs. This approach ensures that premium products are not only affordable but also widely accessible.

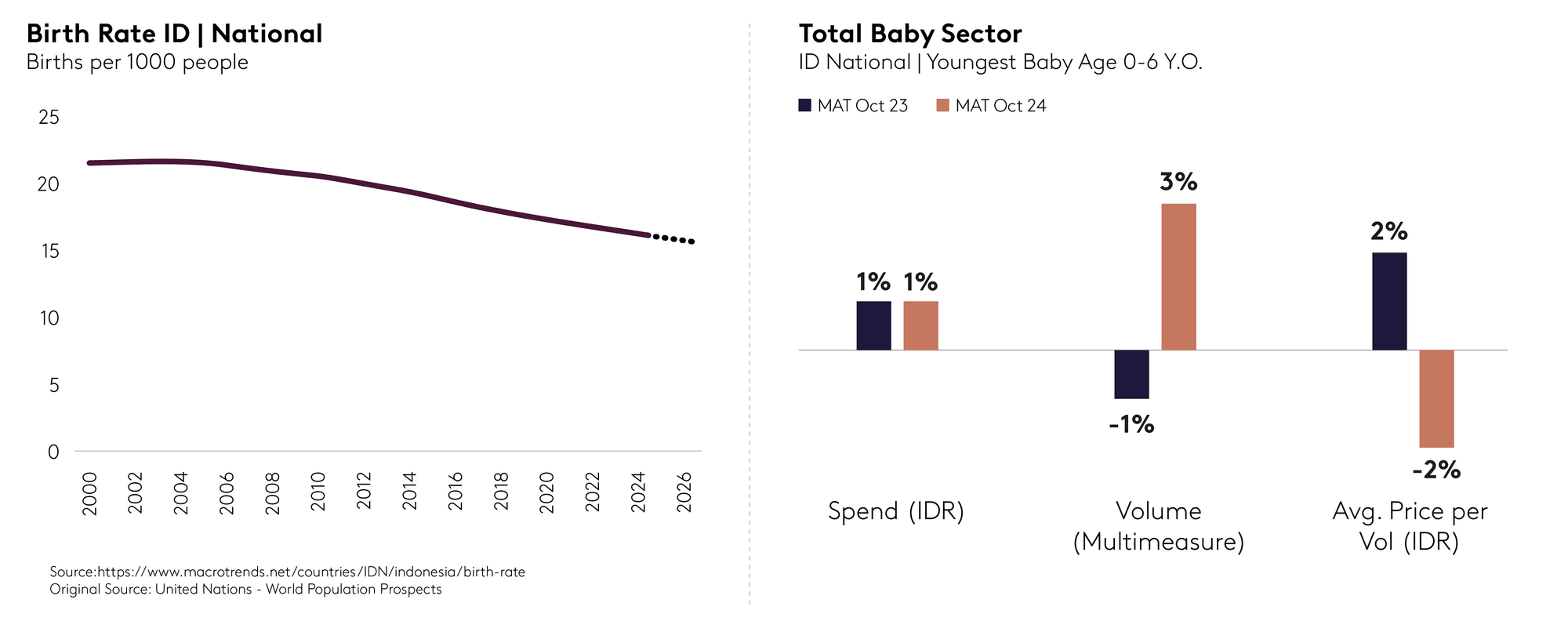

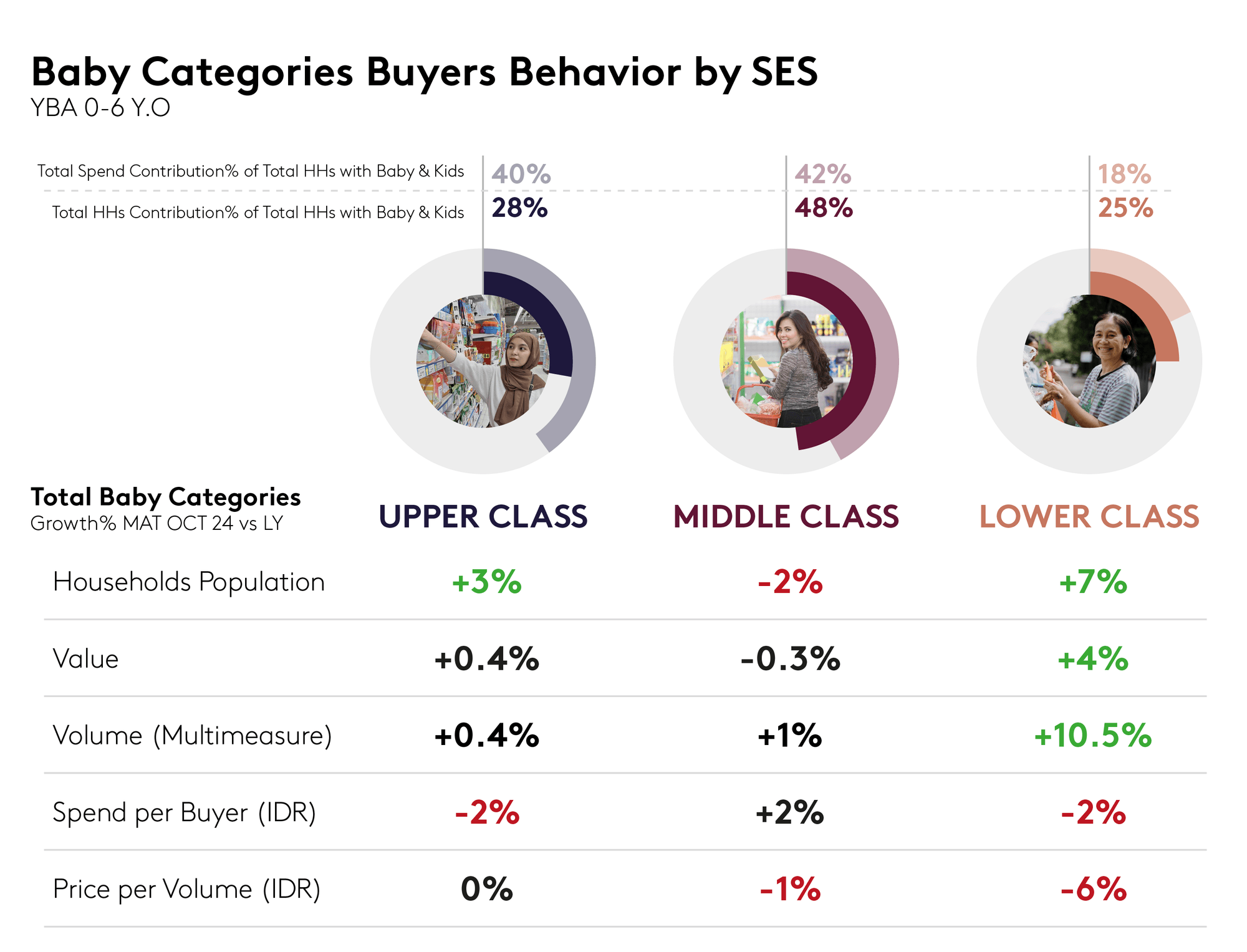

Despite Indonesia’s declining birth rate, the baby sector has shown resilience with modest value growth of 1%, similar to last year. Performance is lowest among Middle class -0.3% value, while the fastest growth is seen in lower-class households at 4%. These consumers may have extra cash to spend following help from the government, yet downtrading is prevalent as they opt for more affordable brands.

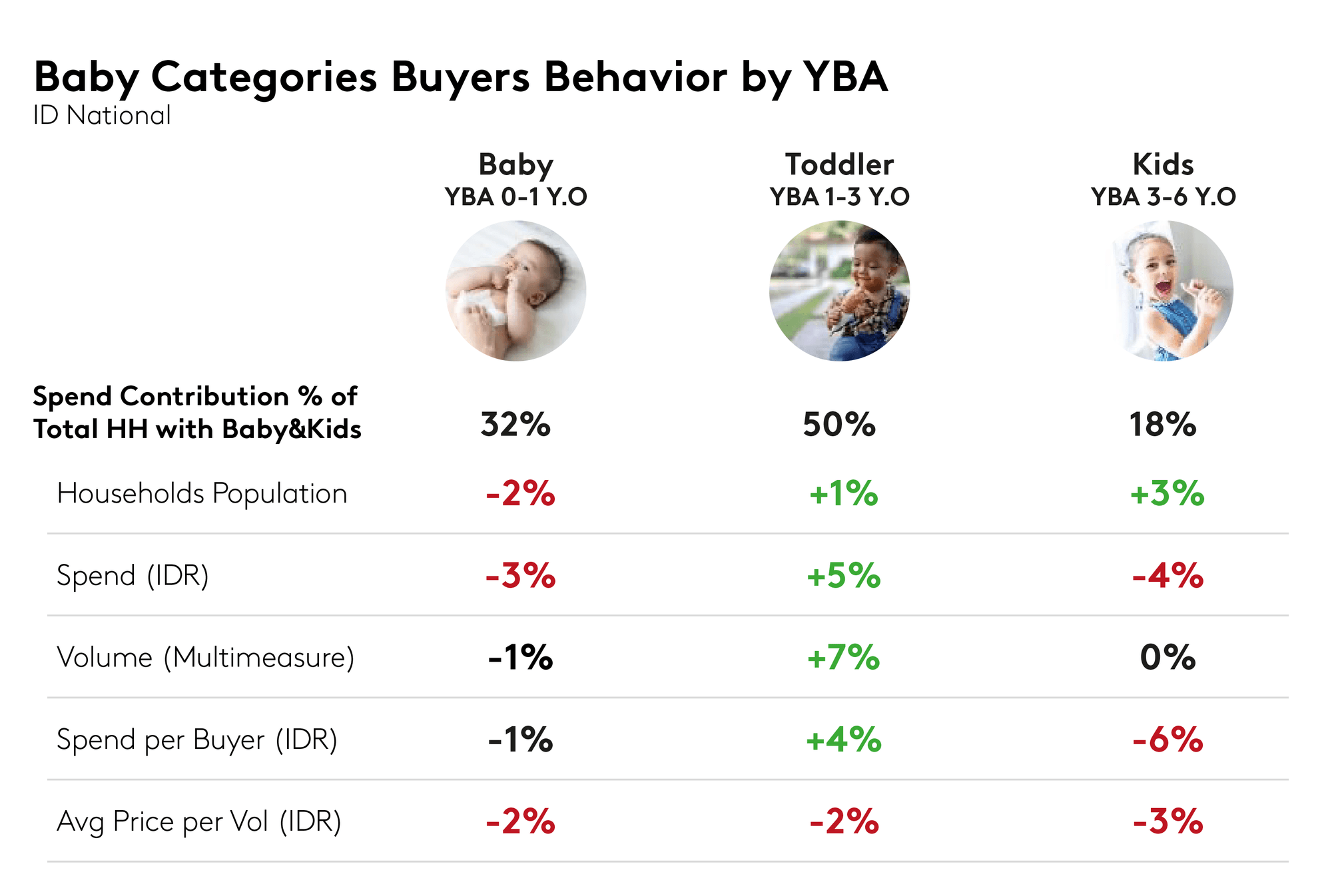

Households with newborns remain a critical entry point for brands, though their growth is slowing due to fewer births. Greater opportunities, however, lie within the toddler segment, which grow value at 5% due to higher spend per buyer.

This suggests a key area within which baby brands can leverage future growth.

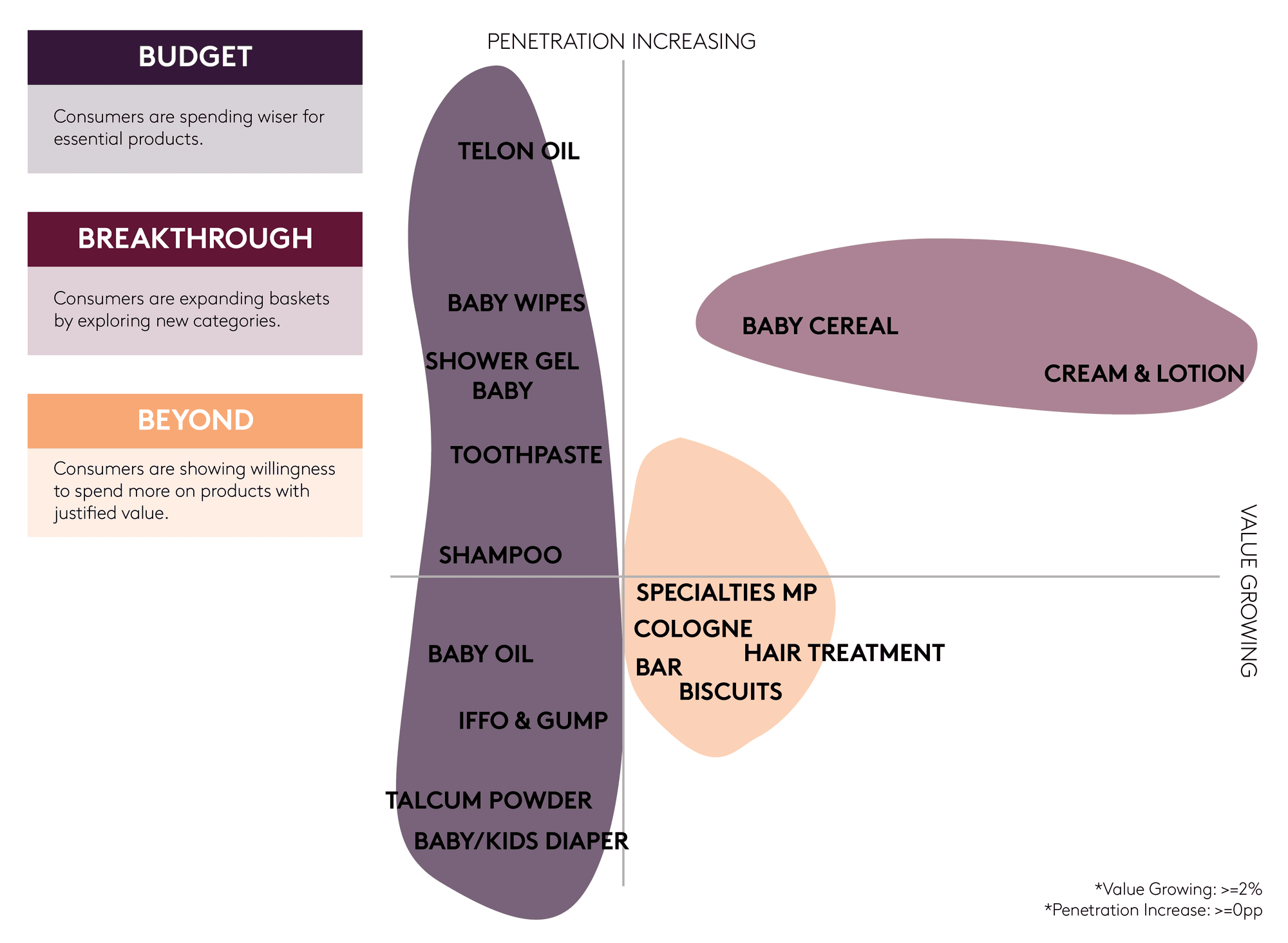

Looking deeper into each category in the baby sector, growth in essential categories such as baby milk powder and baby personal care has been challenging as shoppers reallocated their spending priorities. However, some essential categories, including baby biscuit and specialty milk powder, are managing to grow value as shoppers are willing to spend more to gain extra benefits, which justify a premium price. Some other categories are managing to grow both penetration and value by offering innovation that taps into the white space in the sector, such as baby cereal and cream & lotion.

The milk powder segment has become the backbone of the essentials category, contributing 46% of the total value of the baby sector. In this segment, shoppers are adjusting their spending by choosing either lower-priced products or larger pack sizes to maximise value. Brands that are affordable – with an average price index of between 60-80 – are growing their buyer base in upper class as well as middle class households who are challenged the most. Brands that can offer bigger pack sizes can also grow faster than the market, as they offer better value for money.

On the other hand, premium brands that can clearly justify their price and offer added benefits could also outpace overall market growth. The shift toward affordability does not hinder the potential for brands to achieve growth by leveraging their premium portfolios, as there remains a segment of the population that is willing to trade up for superior quality.

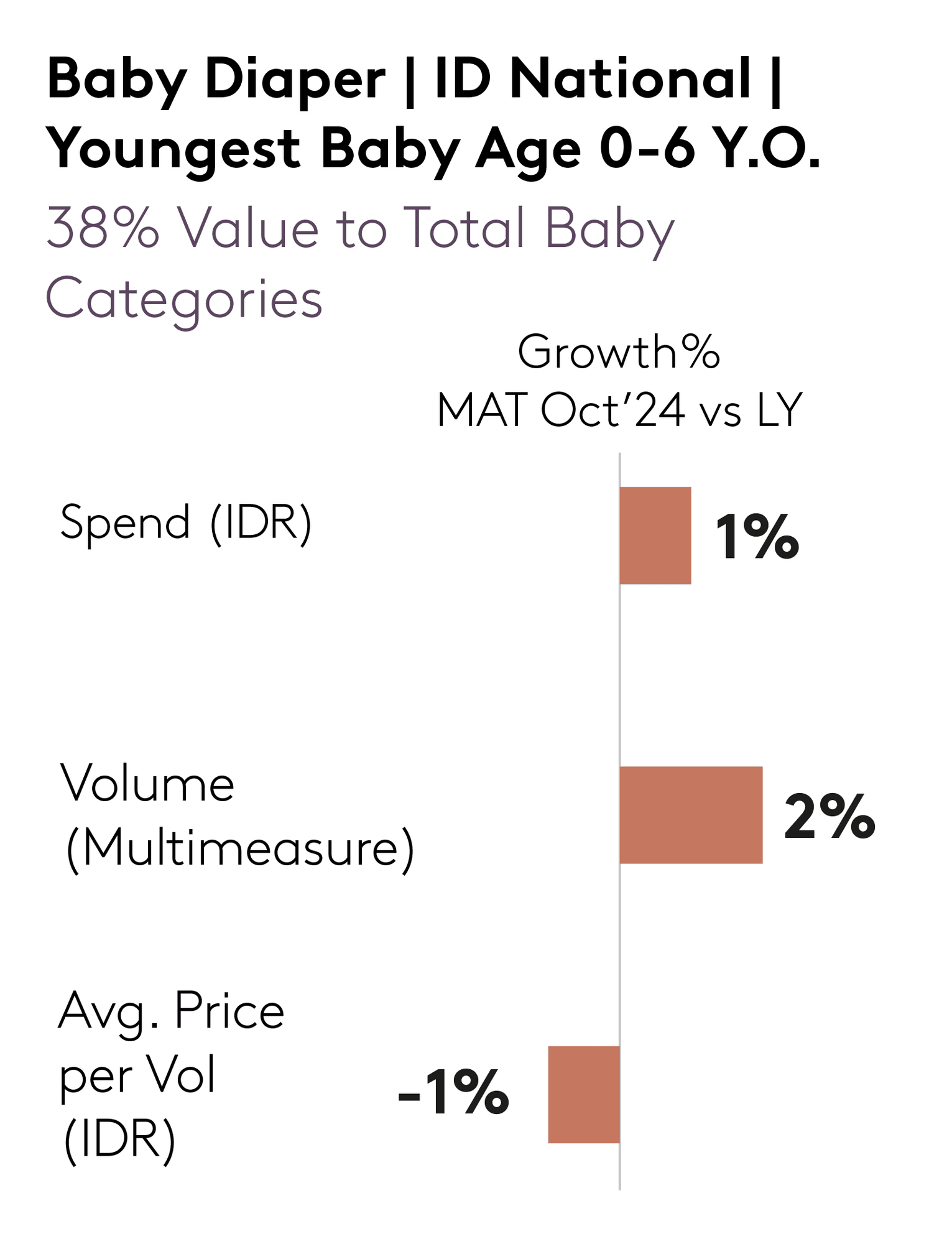

Diapers remain an indispensable necessity, with 38% value contribution to the total baby sector. Value growth is observed at both ends of the market spectrum. Affordable brands attract budget-conscious buyers, mainly middle-class shoppers, while premium options appeal to those seeking superior performance and quality, demonstrating that both segments can thrive by addressing distinct consumer needs.

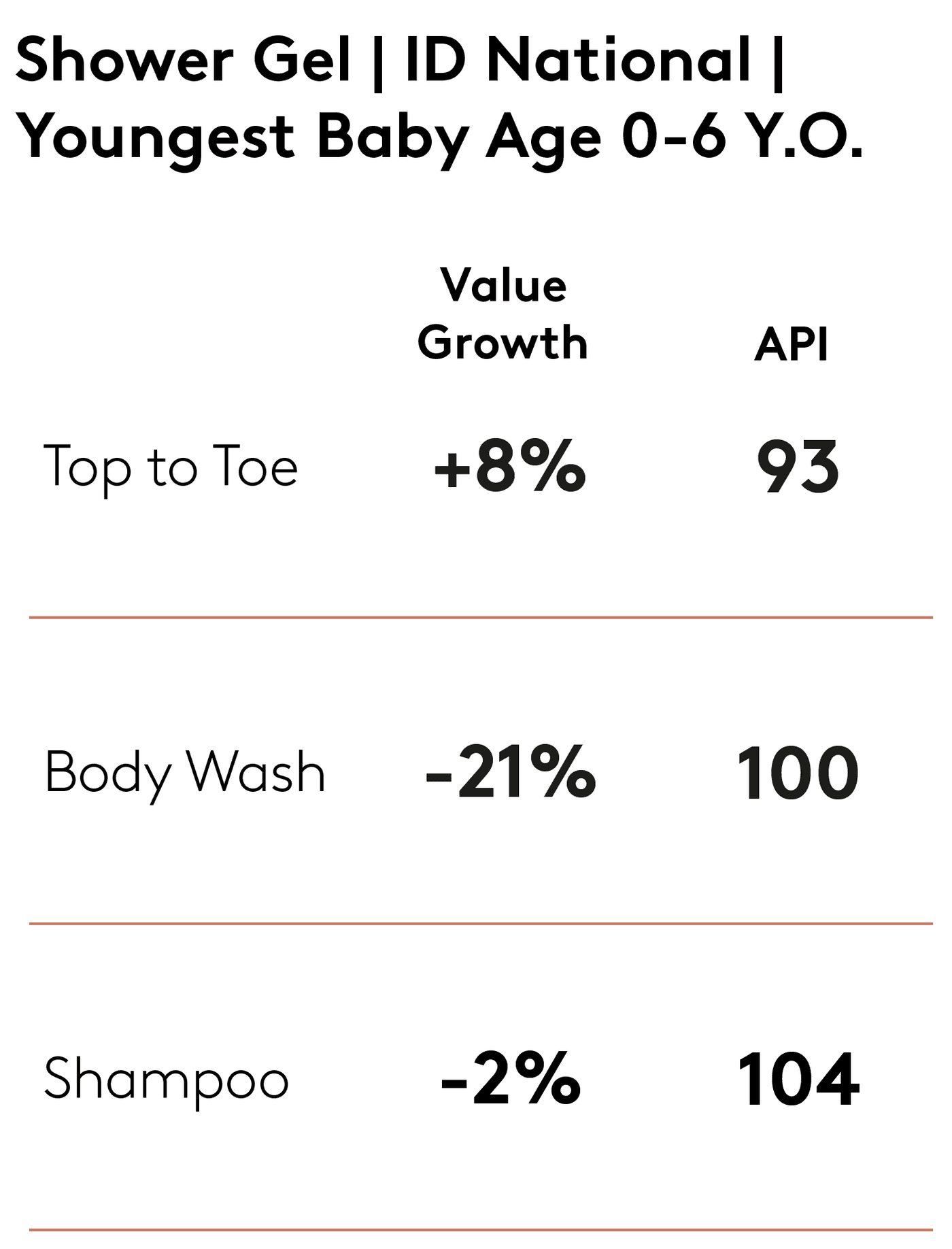

In baby personal care, such as shower gel, shoppers are adjusting their spending to opt for better functionality, such as multi-benefit products like top-to-toe formulations, which grow at 8% at the expense of other personal care products like body wash (-21%) and shampoo (-2%). What’s more, 10% of Indonesian baby personal care buyers only buy top-to-toe products, and don’t purchase any other categories for body cleaning. Brands that provide this assortment are gaining traction, highlighting the increasing demand for value-for-money options that combine convenience and functionality.

Shoppers – mainly those in the upper-class SES – are willing to spend more on products that deliver clear, justified value, particularly in categories related to baby care. Mothers, mindful of the importance of their baby’s skin care and nutrition, are prioritising products that promise superior benefits, making them more open to higher price points in these segments.

For example, a premium baby biscuit with a price 18% higher than average has achieved double-digit value growth by leveraging higher spending from shoppers. Meanwhile, a hair lotion brand with a price index of 158 has attracted more than 100,000 new households by providing the clear benefits of natural and gentle formulations that ensure safety for babies’ sensitive skin.

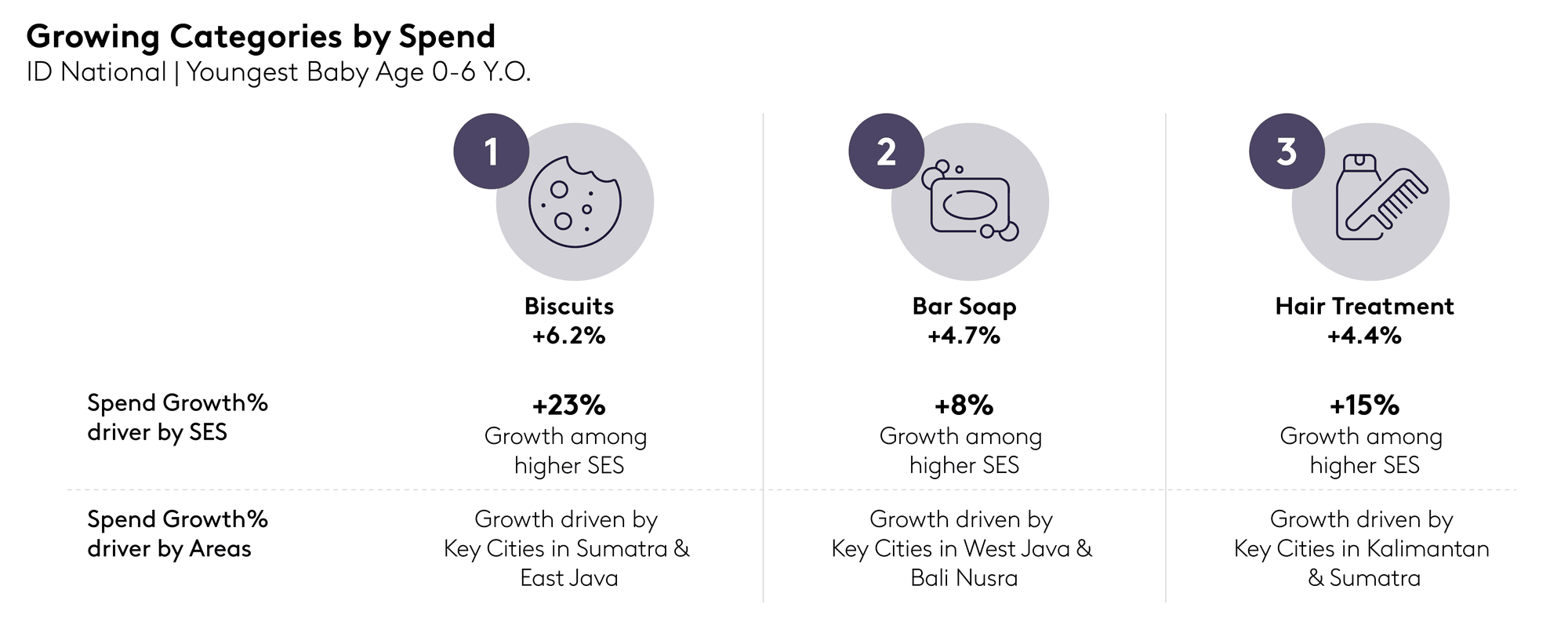

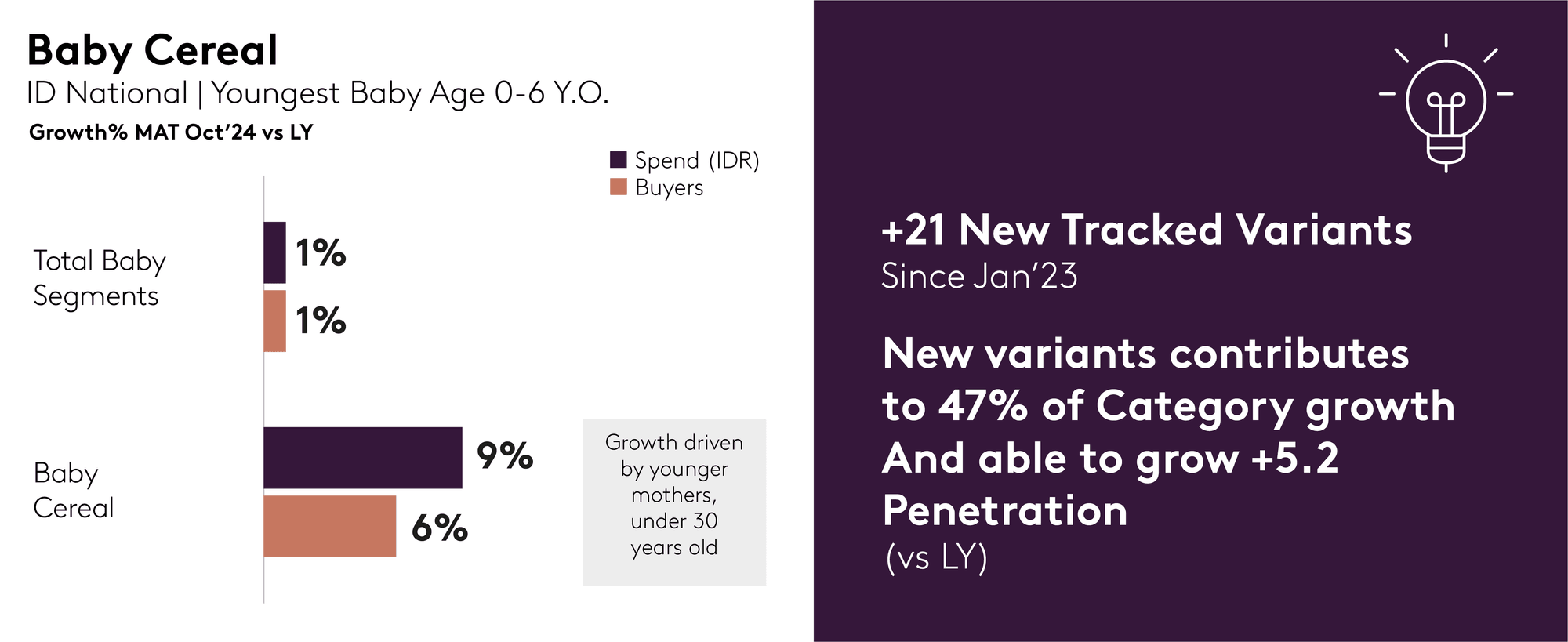

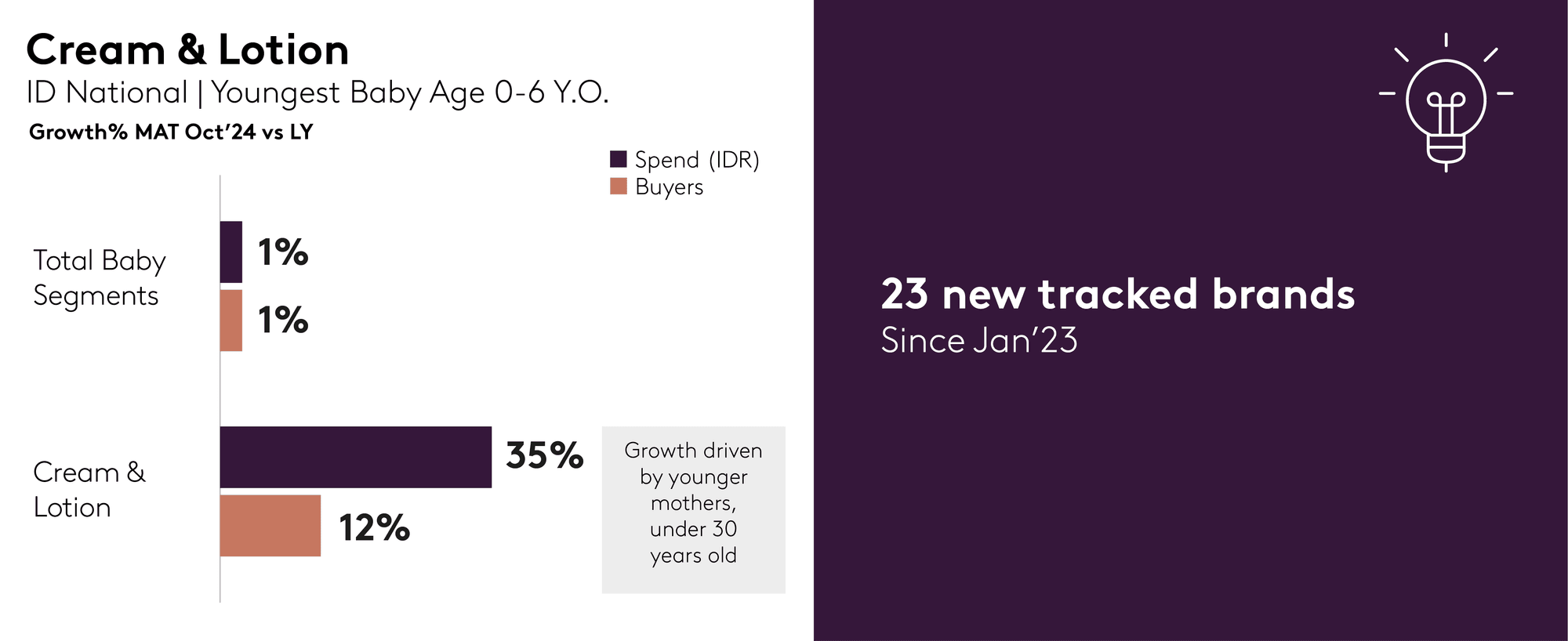

Consumers are broadening their shopping baskets by exploring innovations, and this is fuelling growth across various segments. In baby cereal, there have been 21 new variants launched to date since January 2023 – and combined these have contributed up to 47% of the total category growth, as well as increasing category penetration by more than 5pp.

Similarly, the cream & lotion category is experiencing a surge in shopper recruitment thanks to the introduction of 23 new brands choices, including notable contributions from indie players. Growth is particularly prominent in the online channel, and mainly among younger shoppers under 30 years old.

Enhance value for money by offering budget-friendly options. Brands can appeal to cost-conscious consumers by providing affordable pack sizes and highlighting features or benefits that justify their pricing. Maintaining a balanced portfolio is essential to capture value-driven shoppers while ensuring a diverse range of options for different consumer needs.

Emphasise premium benefits to justify product value. To tap into consumers' willingness to spend, brands should focus on educating shoppers about the unique advantages of their products. Highlighting added health benefits in baby care and nutrition categories can strengthen consumer trust and justify premium pricing, encouraging shoppers to invest in quality.

Leverage emerging needs and channels for growth. Shoppers are exploring new baby care categories, creating growth opportunities. Brands should focus on innovation to meet emerging needs. While bricks-and-mortar stores remain vital, digital platforms offer growth potential, especially with younger mothers who are driving demand. Optimising digital presence through targeted marketing and online offerings can help capture this audience.

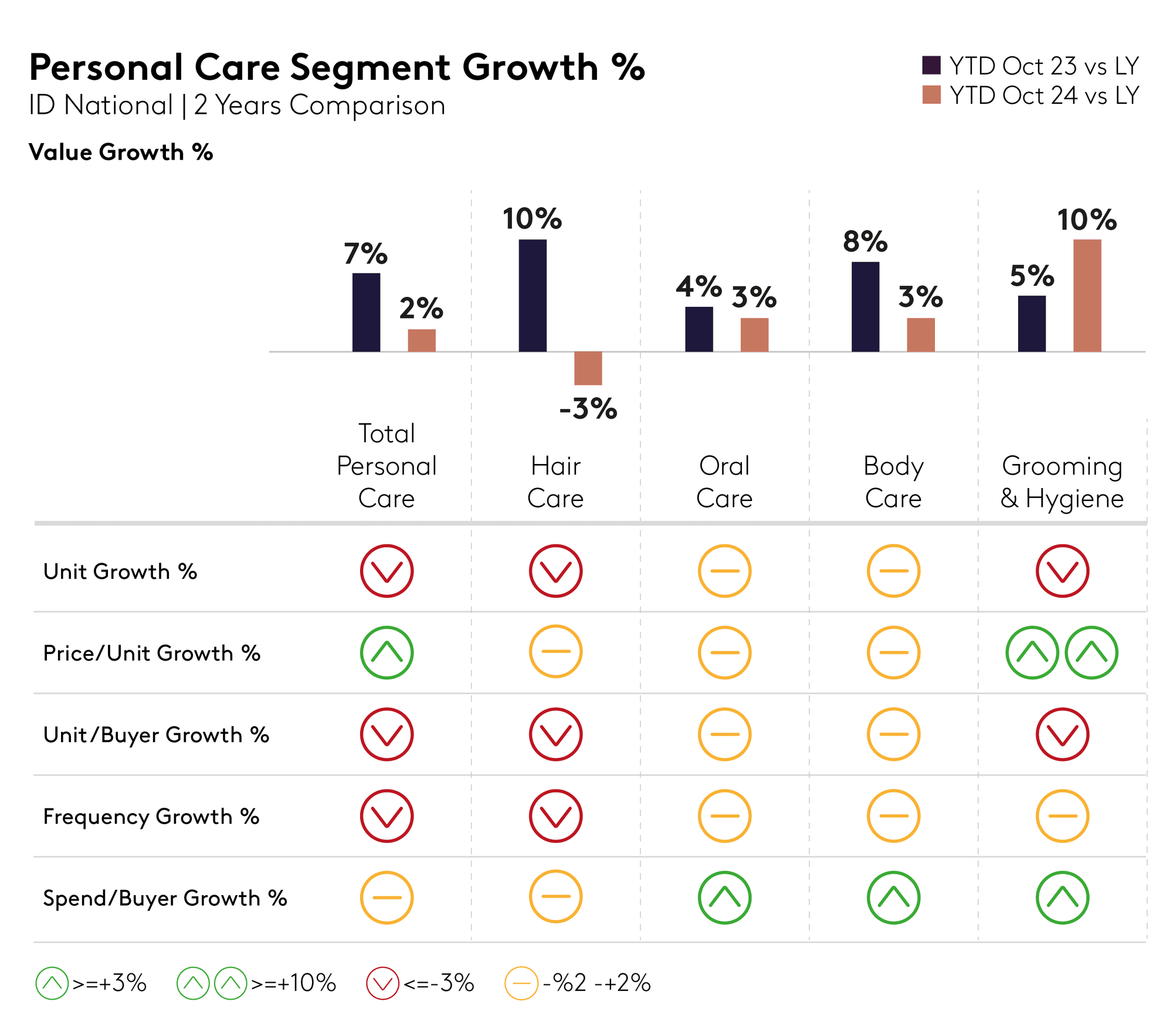

As Indonesian households adjust their FMCG spending, they are deprioritising the personal care sector – especially those in middle and lower SES. As a result, growth is slowing down. This makes providing better value for money more essential than ever for personal care brands when it comes to recruiting shoppers.

Shoppers are opting for channels that offer heavy promotions, such as modern trade and online. Boosting promotions might be another way of helping them to find better value, on top of upsizing. However, there are also opportunities to unlock growth through providing advanced benefits and more natural ingredients.

Across the personal care categories, growth is slowest in hair care, while the oral and body care segments grow modestly at 3% this year, a slower rate than last year. On the other hand, improved price and unit growth in the grooming & hygiene segment, with its smaller buyer base, grow faster than the rest of the sector – suggesting that premiumisation might drive growth in the segment.

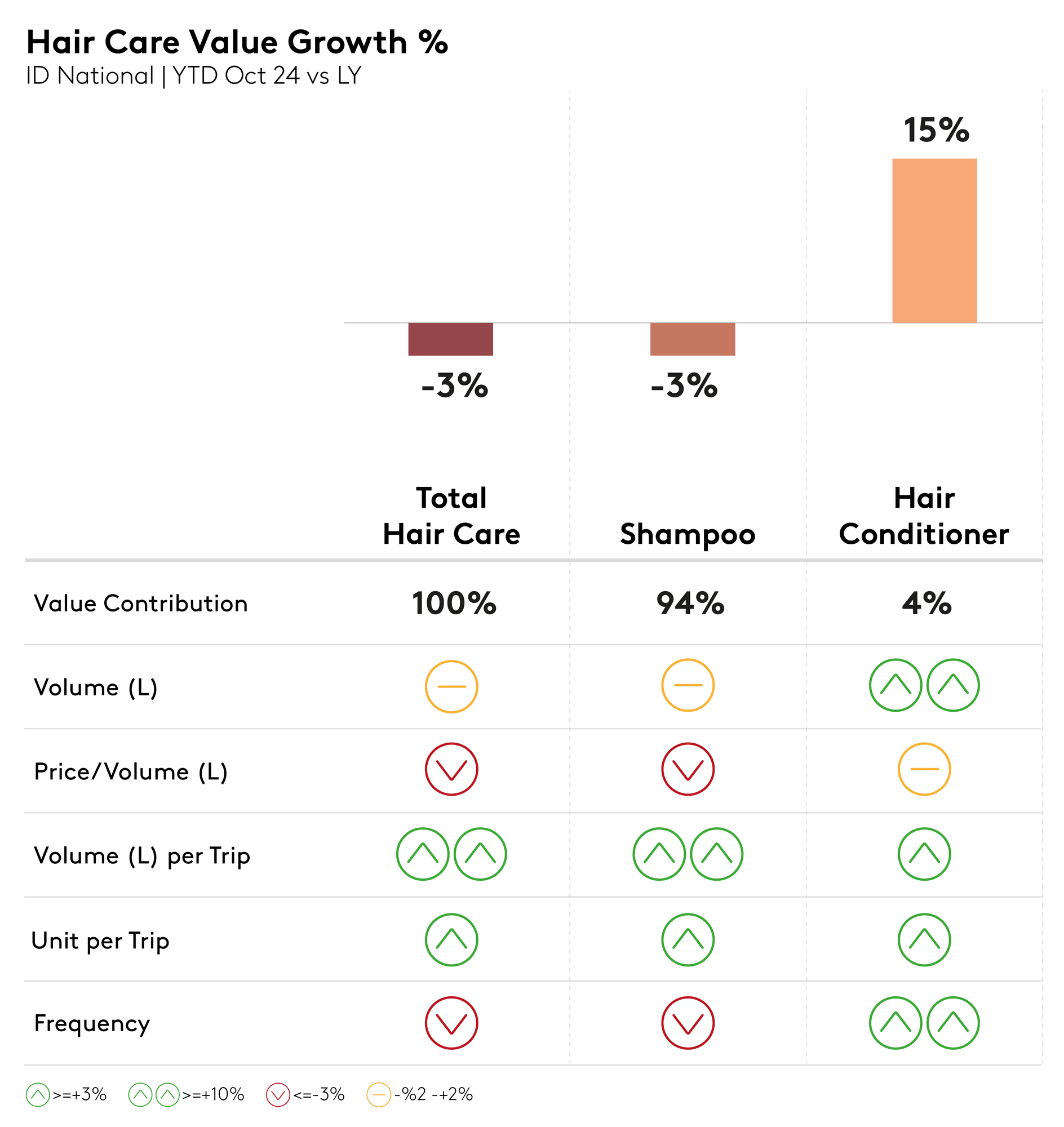

Hair care has long been the backbone of Indonesia’s personal care sector, with the major contribution to value coming from shampoo, and growth for this category is challenging. In contrast, conditioner has grown but its value contribution to the overall hair care category is only 4%, and just one in 10 shampoo buyers also purchase conditioner, suggesting this would have a very limited impact on overall hair care growth.

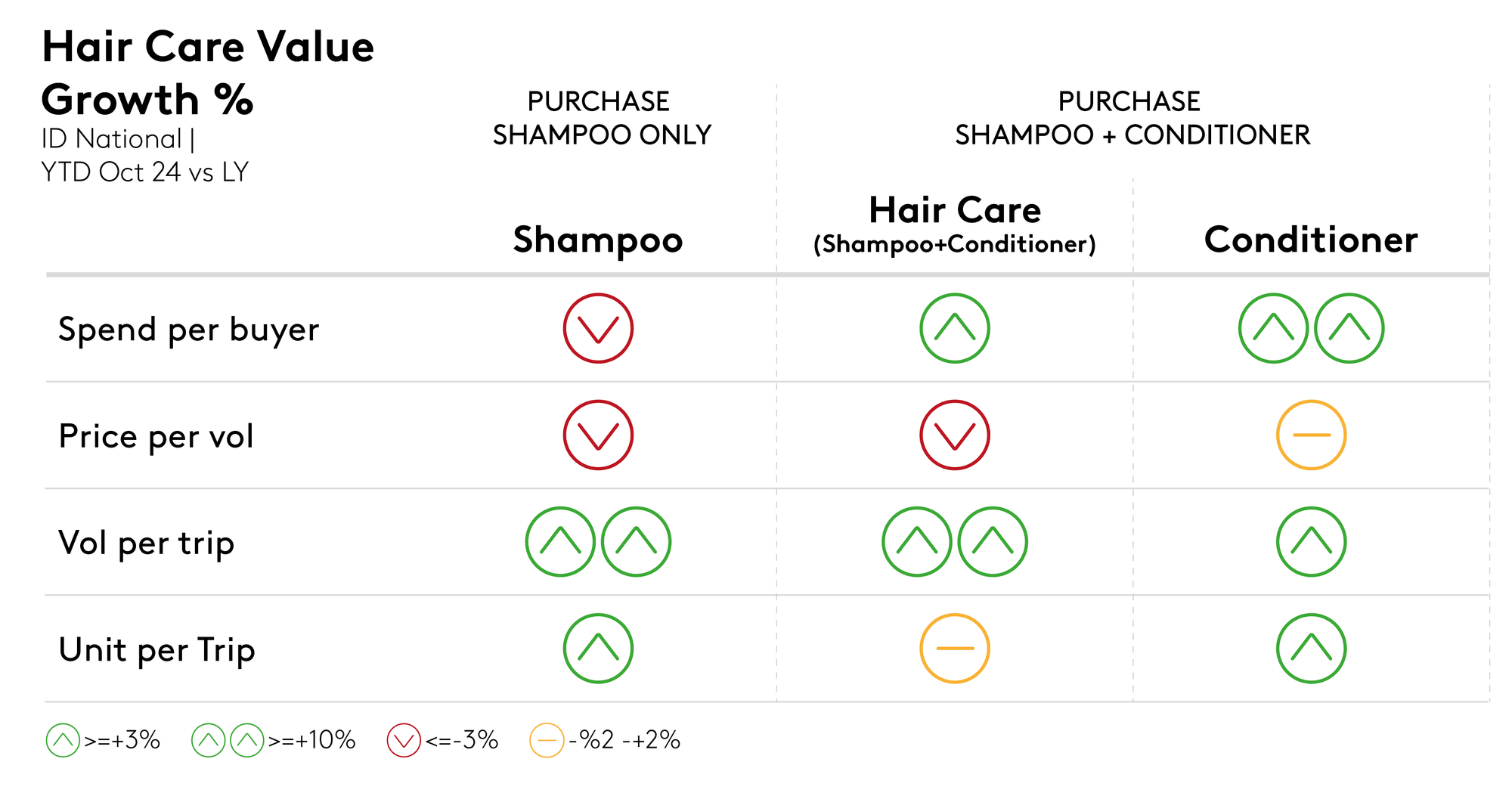

Despite this, the shoppers that buy both shampoo and conditioner are willing to spend more on hair care, indicating that driving higher spending through dual purchase is possible by clearly justifying the benefit of using both shampoo and conditioner.

As shampoo has bigger buyer base with more than 90% penetration, encouraging them to add conditioner to their shopping basket, and extending the benefits of hair care can be a leverage for growth. With sachet pack dominates in the shampoo segment, and providing access to conditioner through introducing sachet packs might be a necessary strategy to expand the buyer base.

Besides, with the increasing trend of modern hair style such as using more hair dryer/stylist, hair colour, the needs for hair care beyond shampoo might increase, suggesting an opportunity for brands to improve the hair care regime.

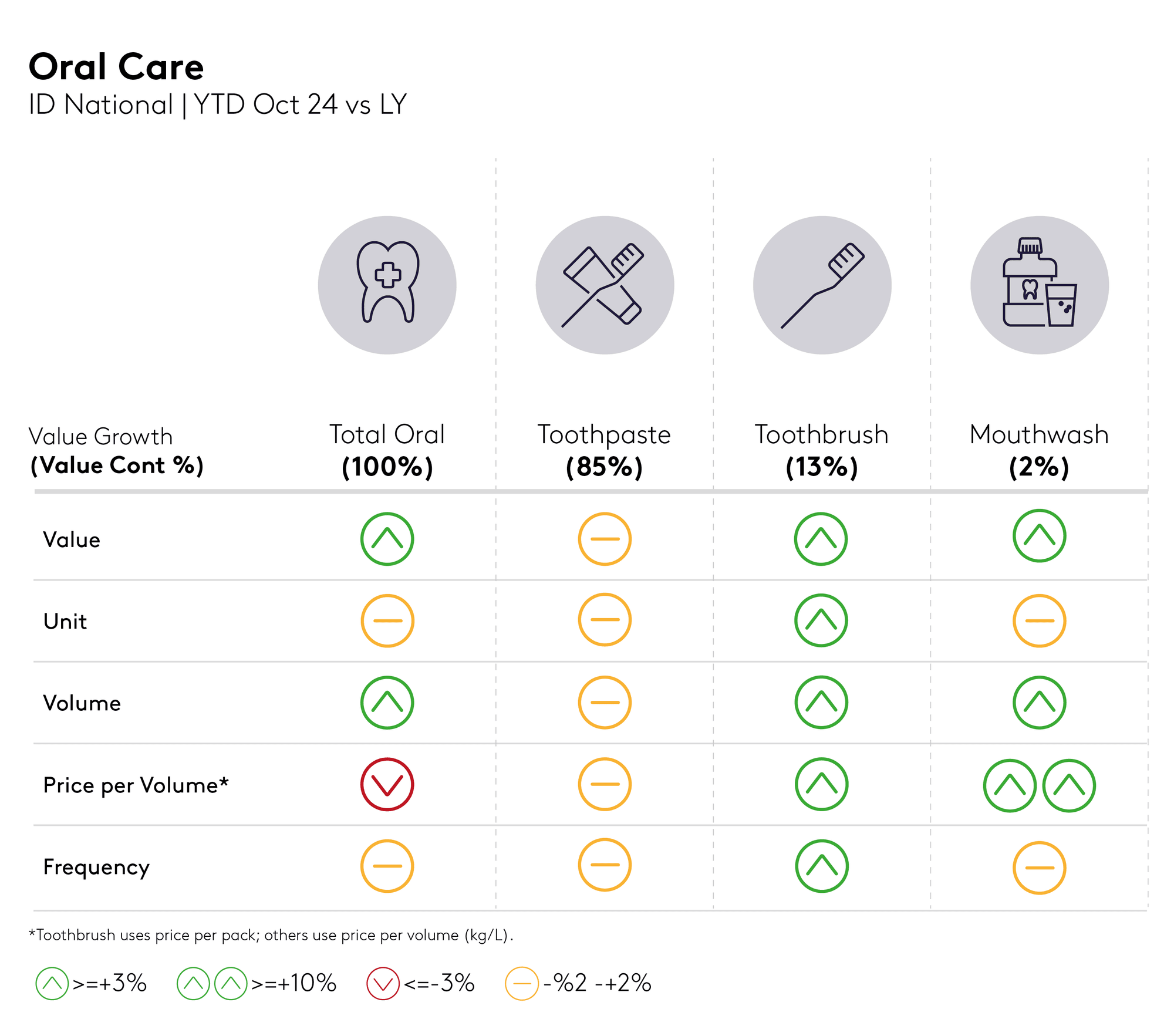

Toothpaste is the dominant segment in the oral care category, and its growth potential is limited. As a staple product, shoppers demand extra benefits from toothpaste, indicating that they might be willing to spend more in the category. Brands that offer benefits such as natural & herbal ingredients, or freshness, could grow their buyer base faster than basic toothpaste. As a result, driving higher spending for toothpaste might be achieved through leveraging multi-benefit products on top of the basic assortment.

Growth in oral care is driven mainly by the toothbrush and mouthwash segments, but in a lower value contribution, hence limited impact. Multipacks of three toothbrushes can grow faster than single packs, suggesting that better value for money can boost penetration. Toothbrush brands can leverage this trend by providing multipack options to increase basket size.

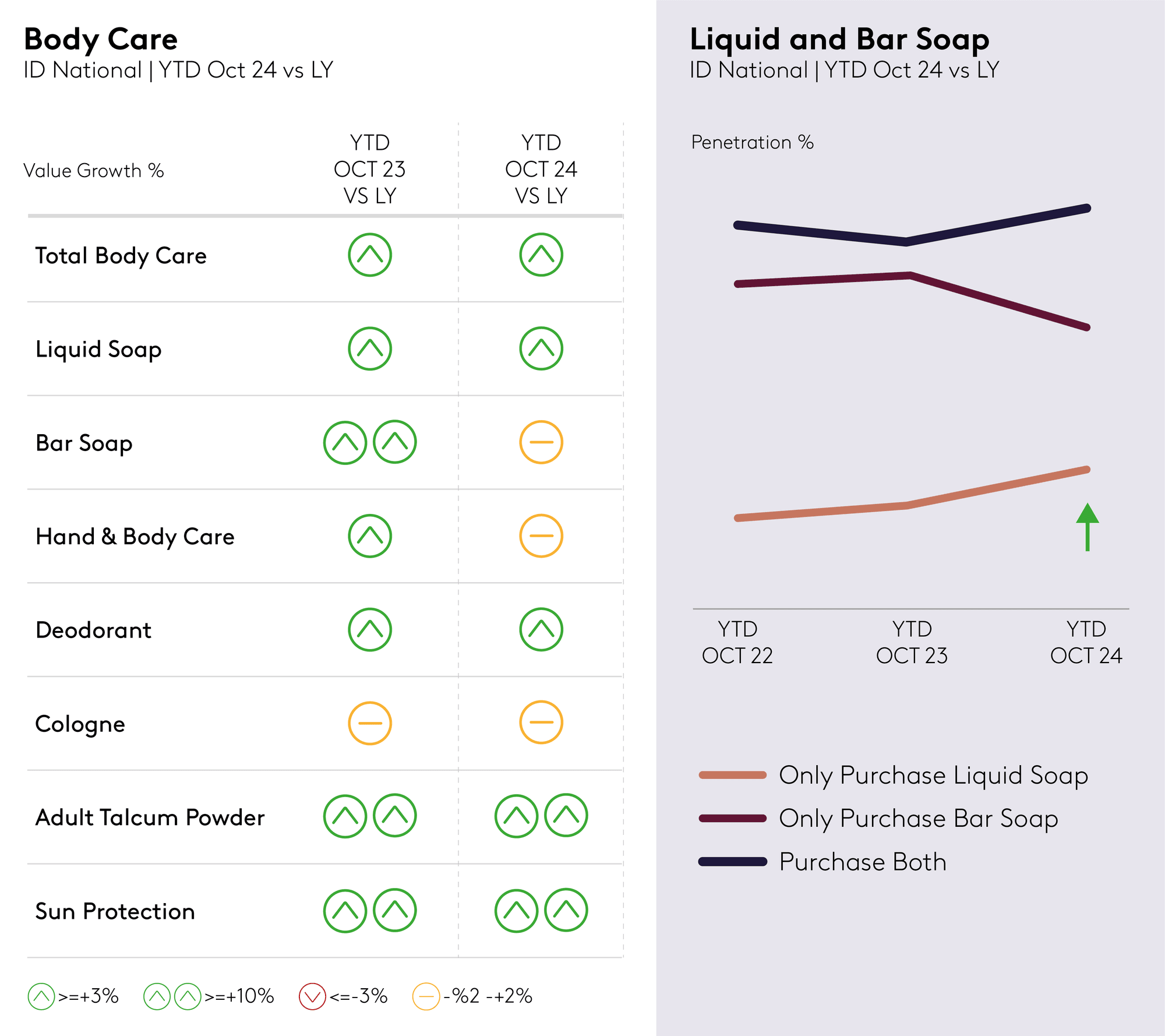

Almost all segments in the body care category have managed to grow in value, with some doing so through increased penetration. In the soap segment, Indonesian shoppers are expanding their basket sizes by purchasing both liquid and bar soaps, rather than completely switching from bar to liquid soap.

Growth in bar soap is driven by products with unique benefits, such as antibacterial properties, extra vitamins, and natural ingredients. Shoppers are willing to extend their purchasing to address needs beyond basic cleansing. For liquid soap, the inclusion of additional benefits has accelerated growth, particularly when these benefits align with skincare properties, such as enhanced skin nourishment and extra cleansing.

Natural benefits also play a significant role in the deodorant segment. Products that are gentle on the skin and formulated with advanced natural ingredients appeal to shoppers and help recruit new buyers. Deodorants that are free from alcohol and harmful chemicals are also gaining traction. Innovations that offer not only added benefits but also extra care for the skin have proven effective in attracting shoppers.

In addition to expanding assortments through innovation, making core variants more accessible can drive growth in the deodorant category. Brands that have introduced more affordable formats, such as sachet packs, have seen faster buyer growth among mid- to low-income shoppers.

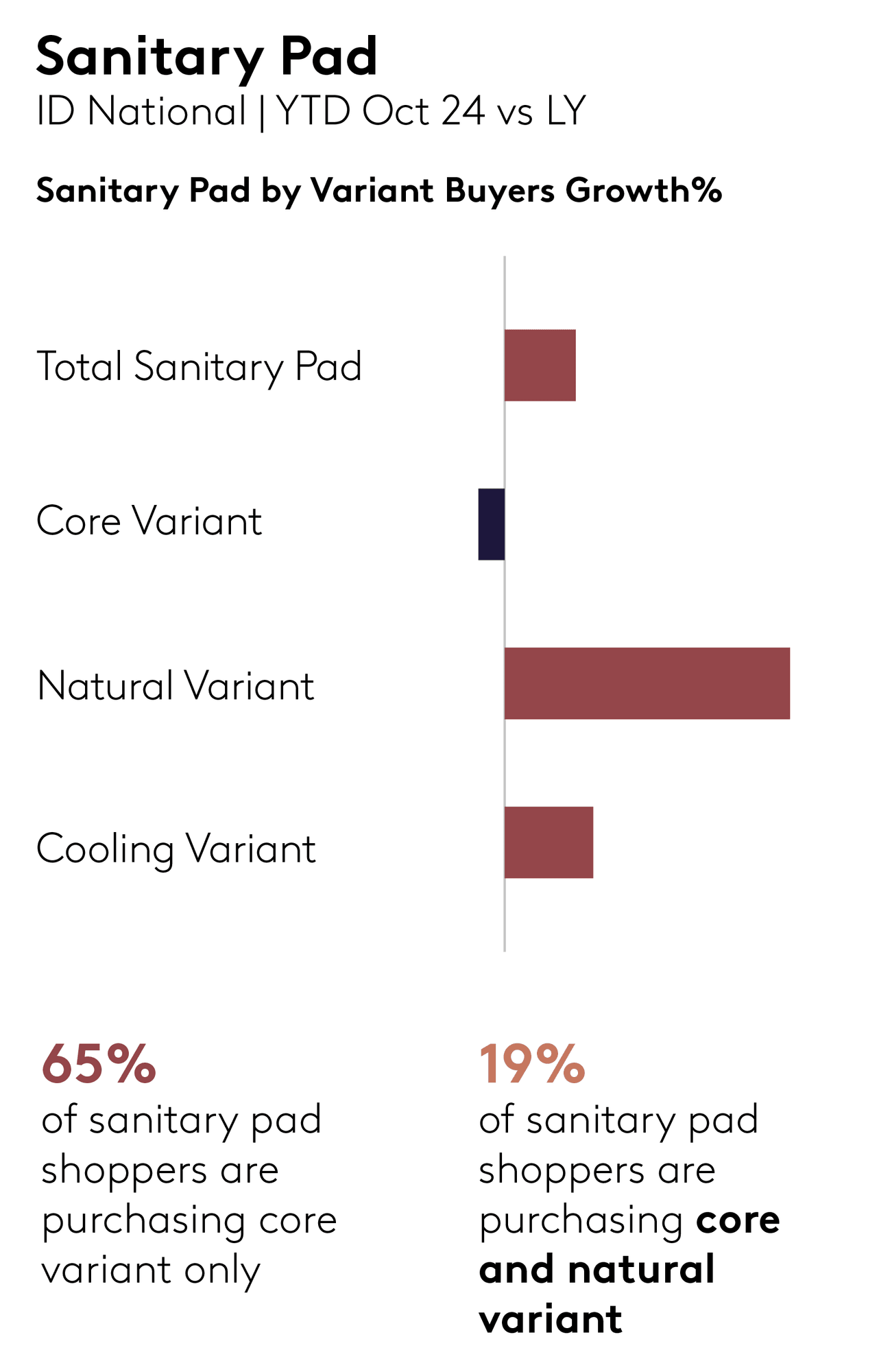

The demand for hygiene care, mainly for sanitary pads, is undergoing a noticeable shift as shoppers increasingly prioritise products with advanced features that cater to their specific needs. Natural variants can grow faster than others, suggesting that innovation in this area is well received and there might be untapped demand for more natural benefits. In fact, two out of 10 sanitary pad shoppers in Indonesia purchase both core and natural variants.

In addition, cooling effects have become a sought-after benefit, appealing to consumers desiring freshness and comfort, especially in warmer climates. Non-allergenic properties are also gaining traction as shoppers become more mindful of their skin's health and sensitivity, reflecting a heightened awareness of product safety and dermatological care.

This evolving demand highlights the importance of innovation in the hygiene care category, where brands that focus on delivering enhanced benefits can not only meet consumer expectations but also foster loyalty and expand their market presence. By addressing these emerging preferences, brands have an opportunity to stand out in a competitive market and cater to a more discerning shopper base.

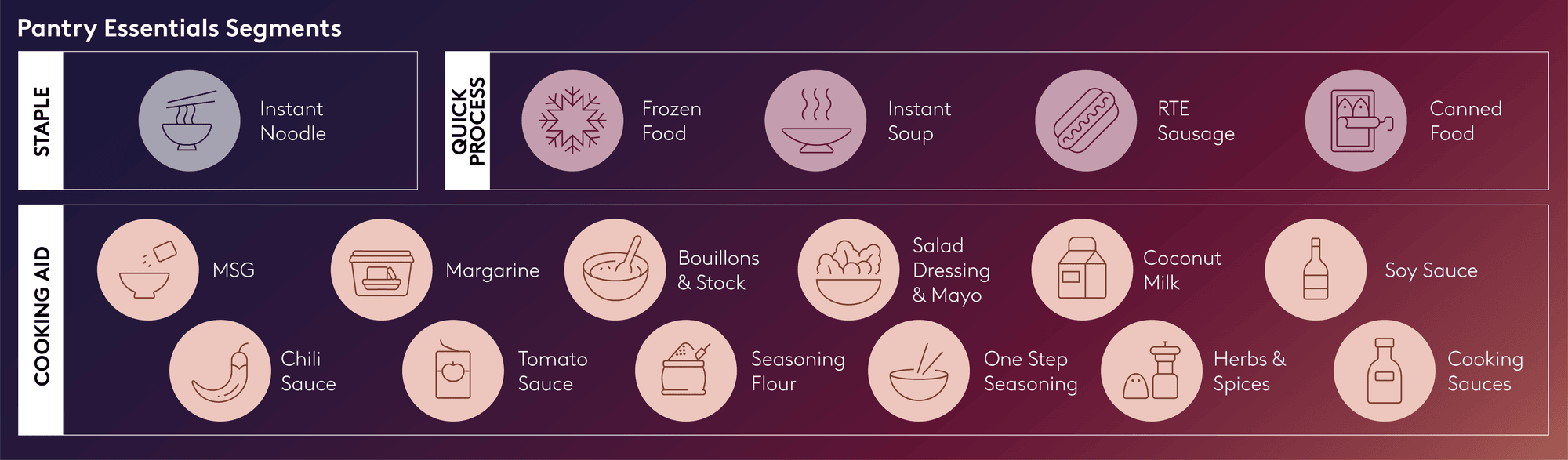

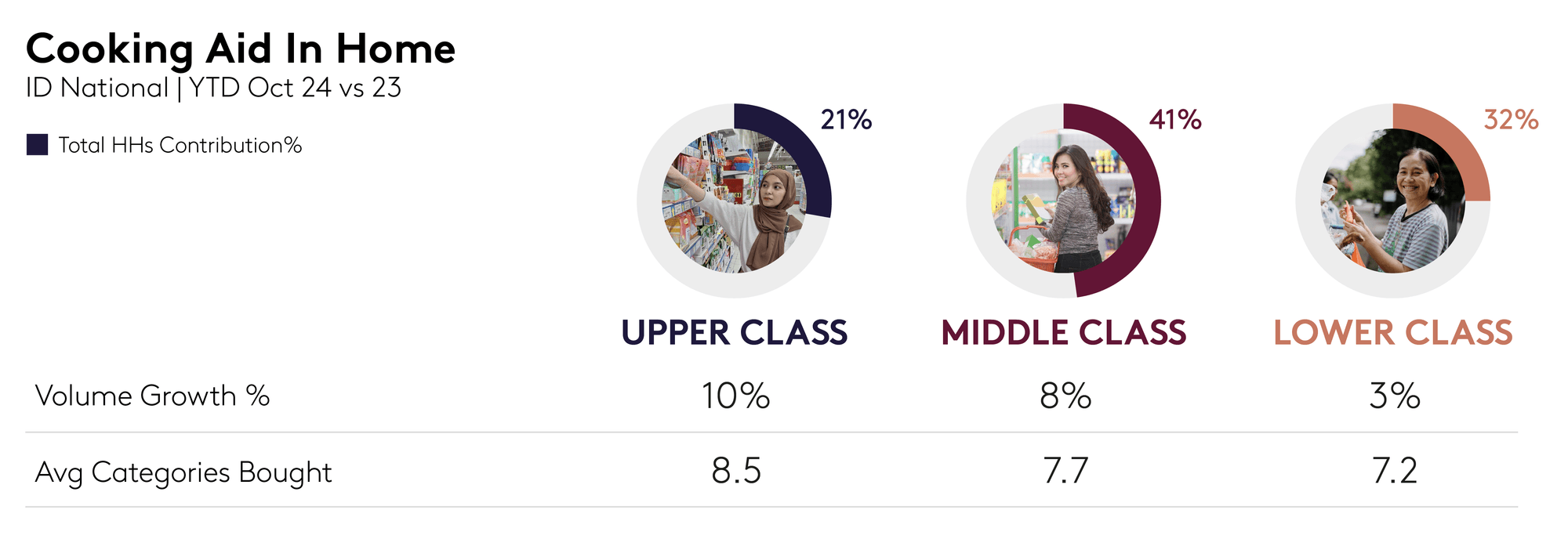

Indonesia’s pantry essentials sector reveals evolving consumer behaviours, shaped by a blend of value-seeking and a desire for functionality. Divided into three primary categories – staple products, quick-process products, and cooking aids – this sector reflects changing priorities across different socio-economic classes.

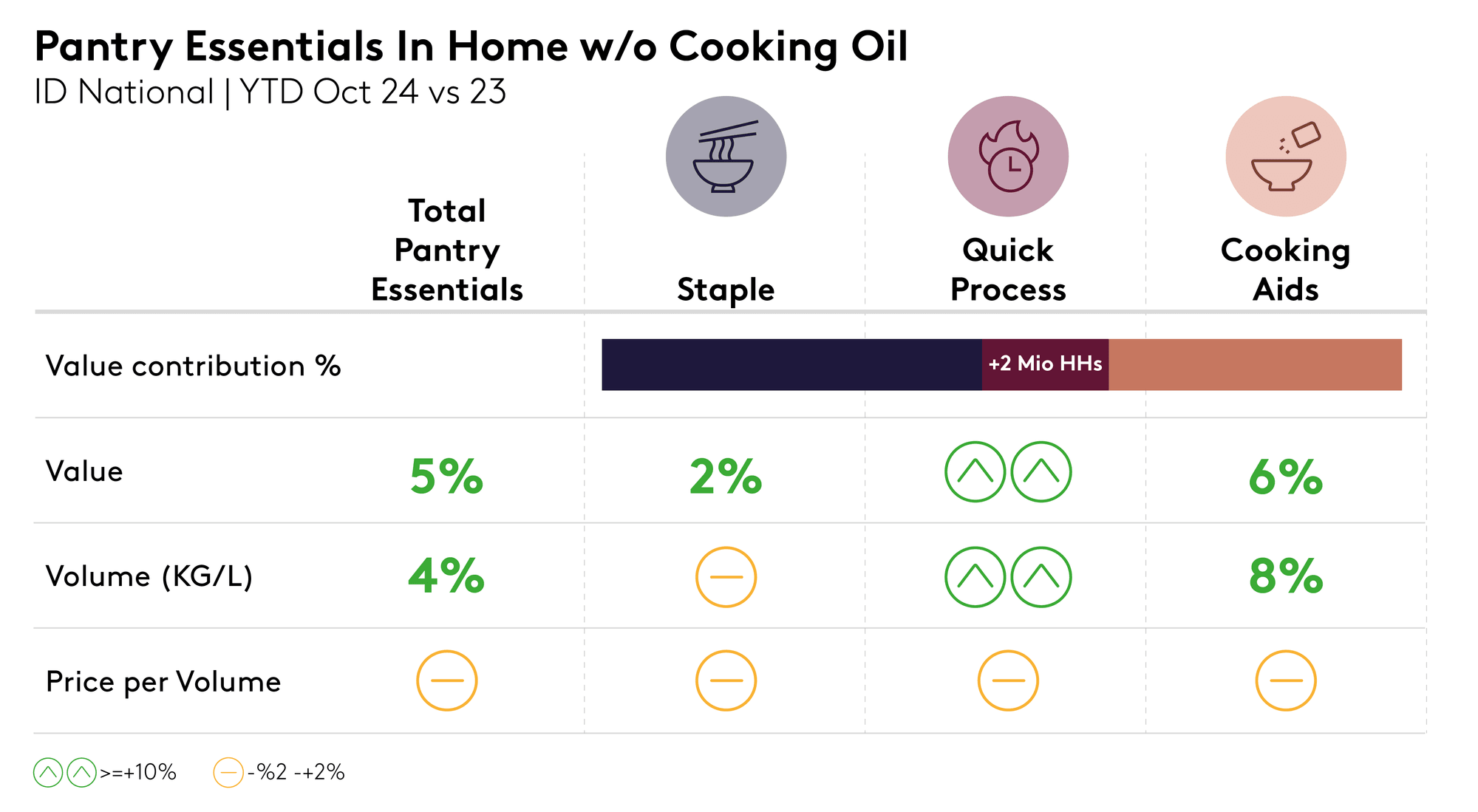

In 2024, the pantry essentials sector saw value growth of 5%, driven by stabilised prices and a shift towards maximising value. Consumers across all classes began purchasing larger pack sizes to get more for their money. This trend is particularly notable in the growing popularity of practical, quick-process products like canned food and one-step meals, which cater to the demand for functional, time-saving solutions.

In addition, socio-economic dynamics are influencing category preferences: upper-class shoppers are focusing on cooking aids, while the middle- and lower-classes are increasingly opting for quick-process products, which experienced double-digit growth in 2024. This diversification in spending priorities indicates a broad-based recovery across the pantry essentials market.

The insights from 2024 emphasise a growing trend toward maximising value and convenience, setting the stage for strategic growth in 2025. Let's dive into some key trends that are shaping this sector.

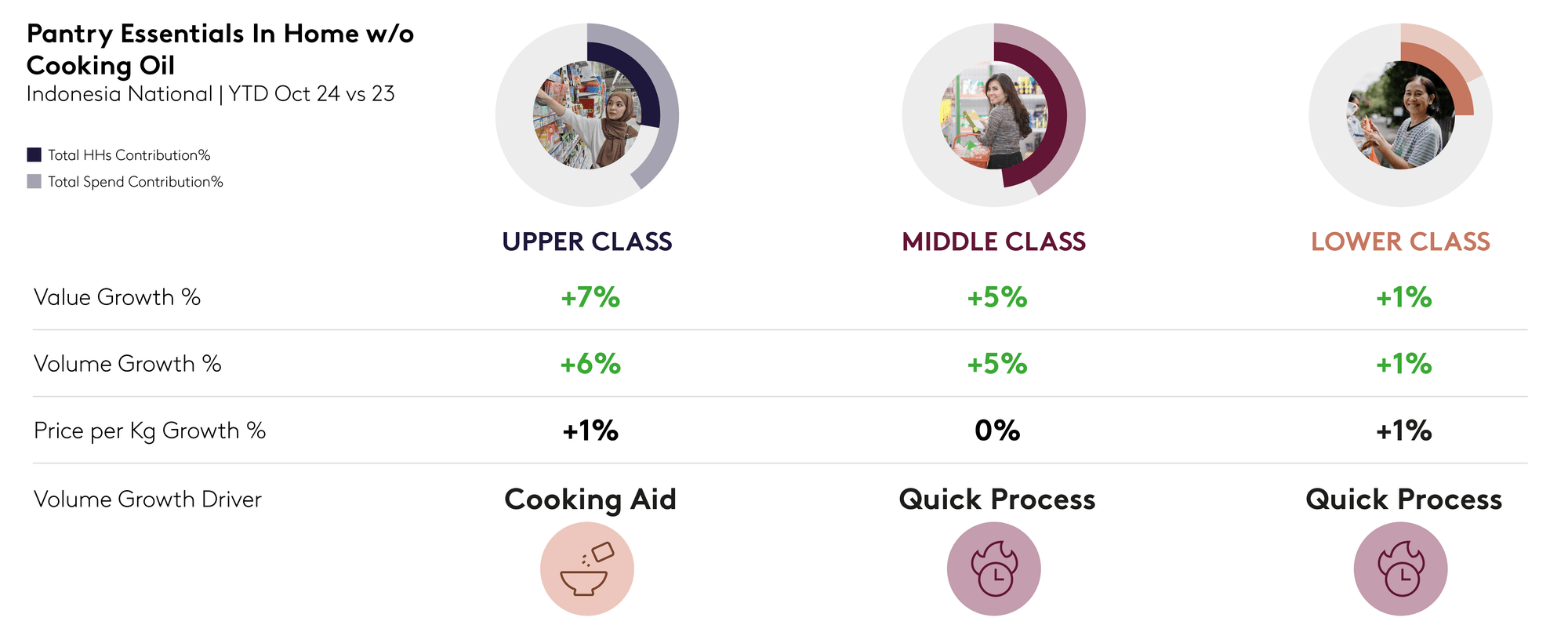

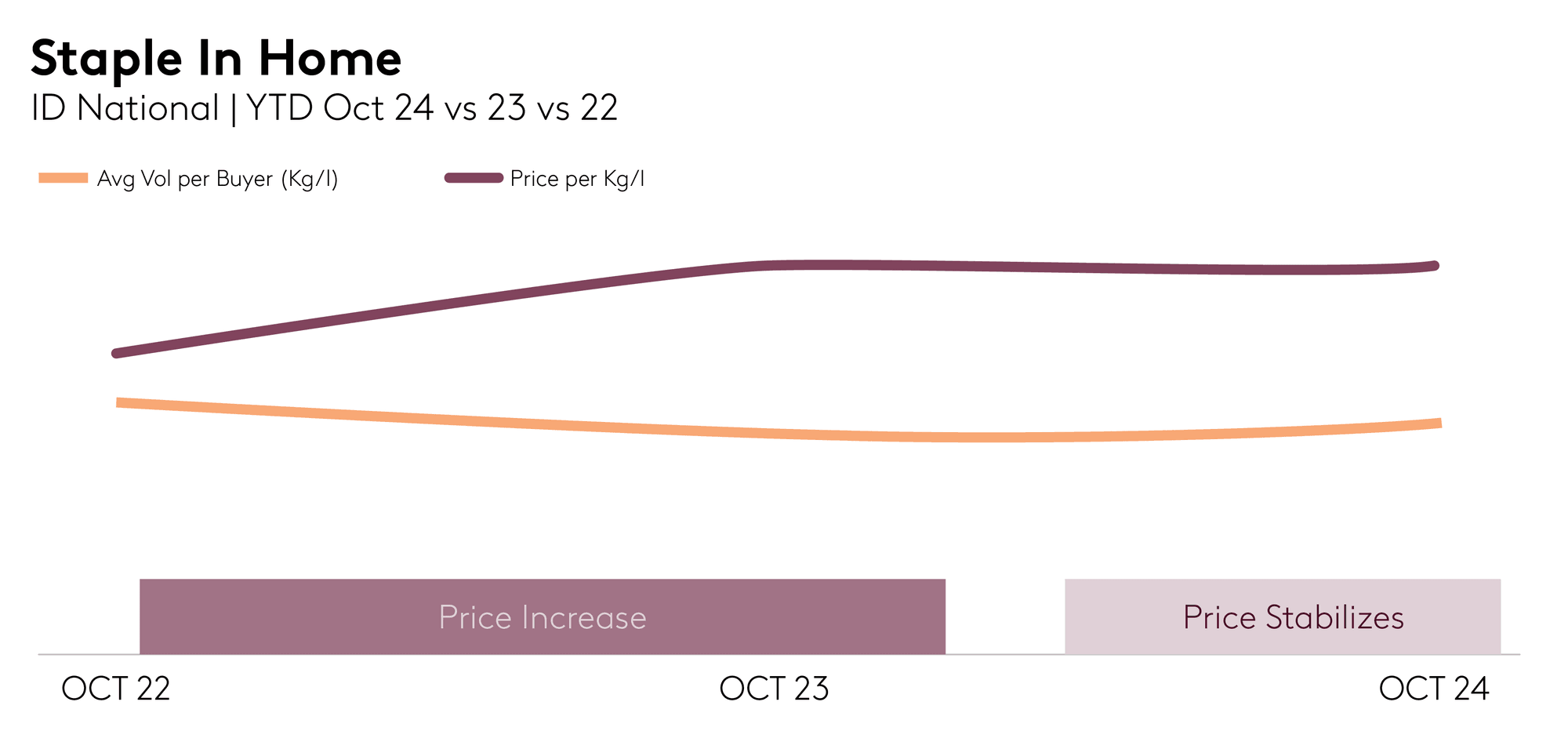

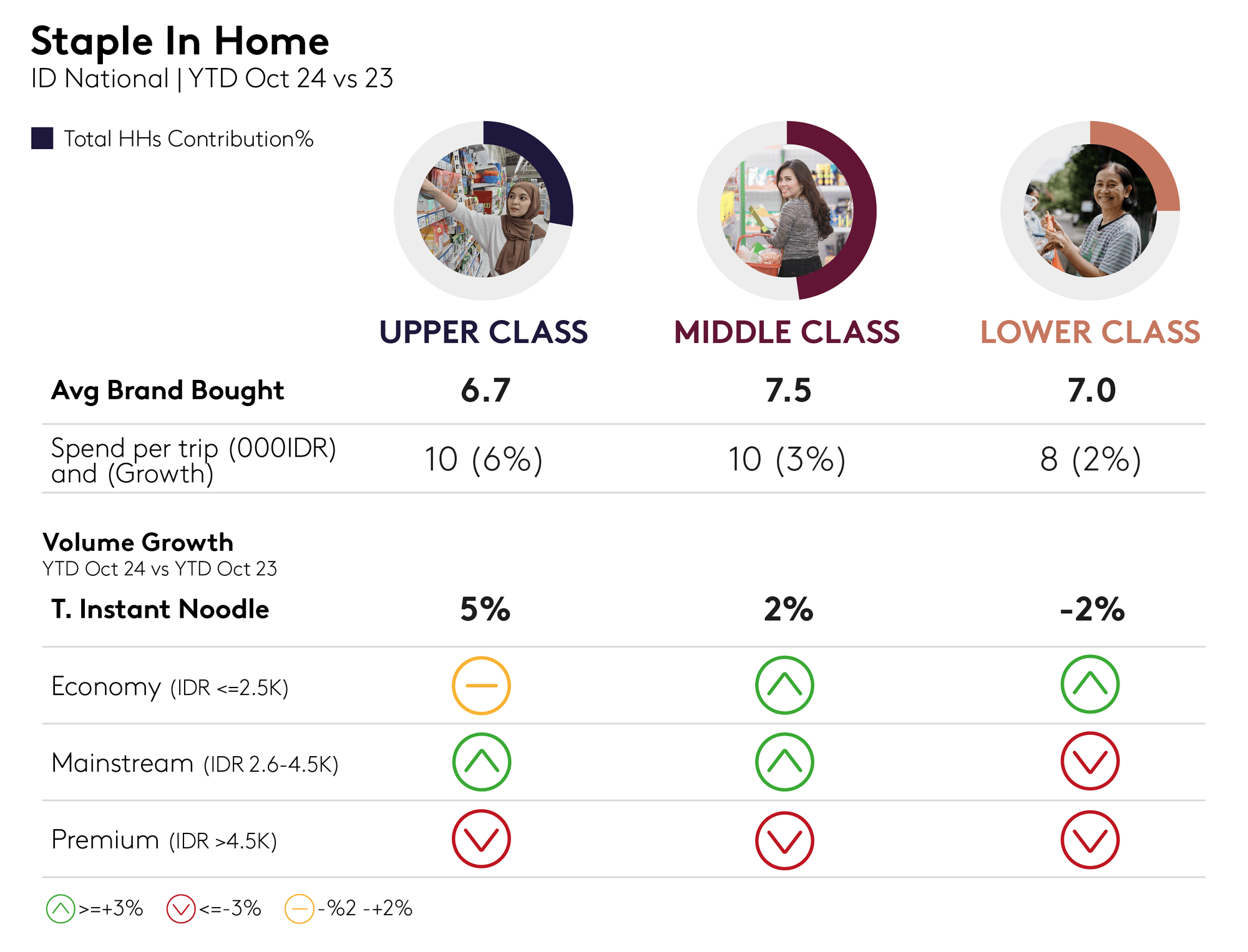

The staples category rebounded in 2024, recovering from last year’s inflation-driven decline as price stabilisation encouraged increased consumption. Volume per trip is now growing faster than before, signalling a healthier market. This recovery is led by Indonesia’s upper- and middle-classes, though their brand preferences vary significantly. Upper-class shoppers tend to favour mainstream brands, though opportunities for upgrading remain due to their higher spending capacity. Conversely, the middle- and lower-classes are exploring more affordable options, leaning towards mainstream and low-end brands.

For brands, the key to thriving in this saturated segment lies in balancing growth and affordability. Mainstream brands can capture upper-class shoppers by offering premium upgrades, while Economy brands should focus on maintaining affordability to retain middle- and lower-class consumers. Brands that can navigate these diverse preferences will be well-positioned to capitalise on the recovery in the staples category.

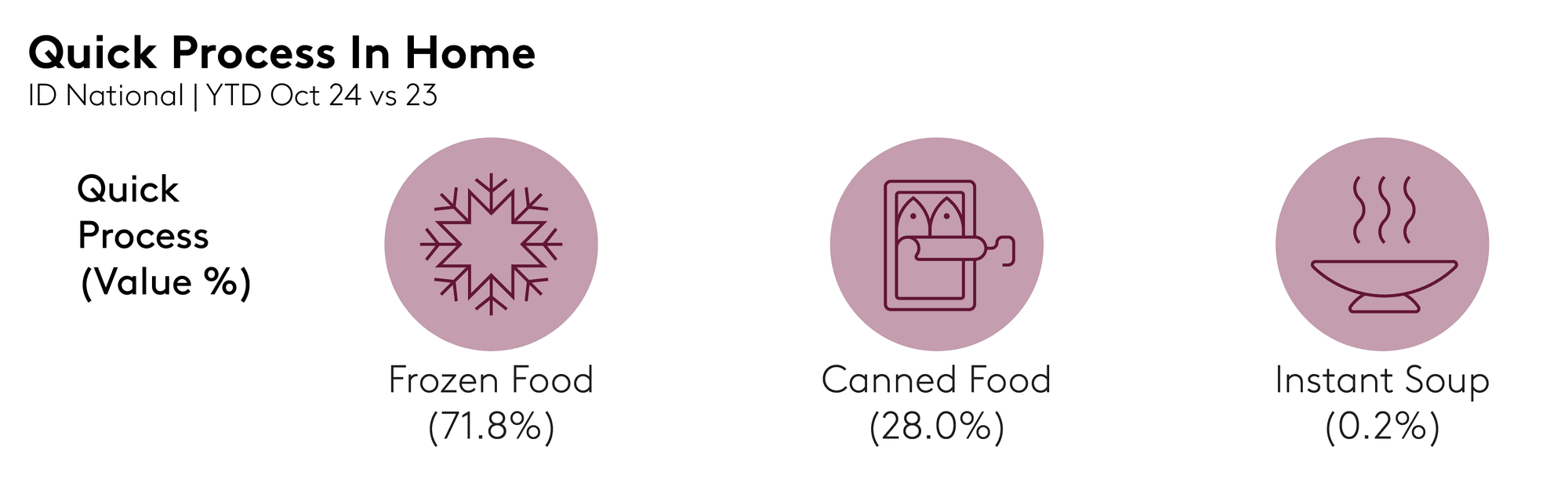

The quick-process segment is thriving, fuelled by shoppers’ growing preference for convenience and practicality. Canned food is leading the charge, with rapid growth driven by a larger buyer base and increased shopping frequency. However, frozen food is also expanding, as shoppers opt for larger, value-for-money packs, driving volume per trip. This highlights the segment's appeal, blending practicality with innovative taste offerings.

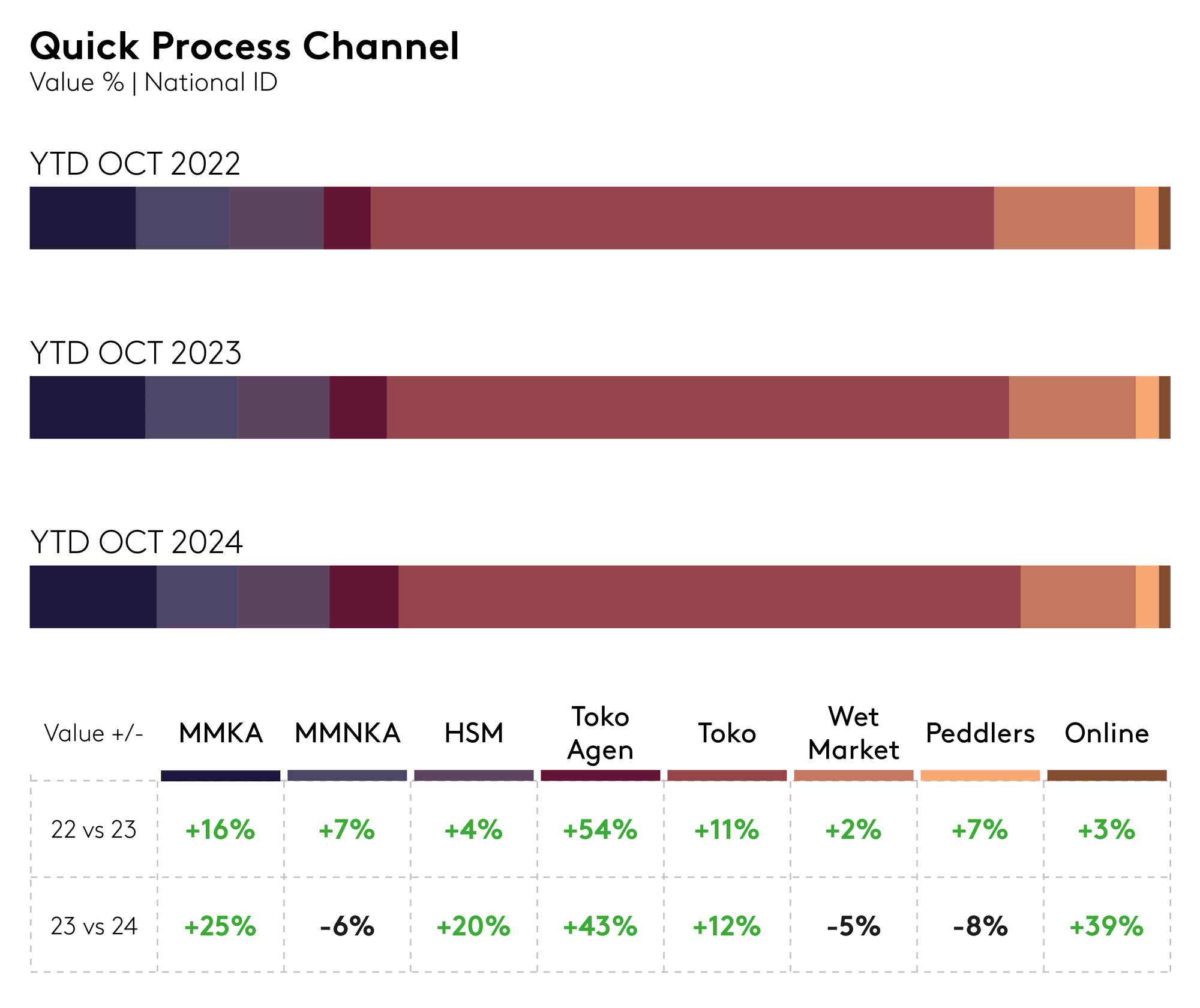

In terms of retail channels, minimarket key accounts and hyper/supermarkets are significant drivers for canned food. Meanwhile, Toko Agen is boosting the frozen food market, with the largest contribution to the segment’s overall value, demonstrating the need for brands to strategise across multiple channels. Brands can capitalise on these trends by tailoring their offerings to meet the specific demands of each channel, ensuring relevance and accessibility for different shopper cohorts.

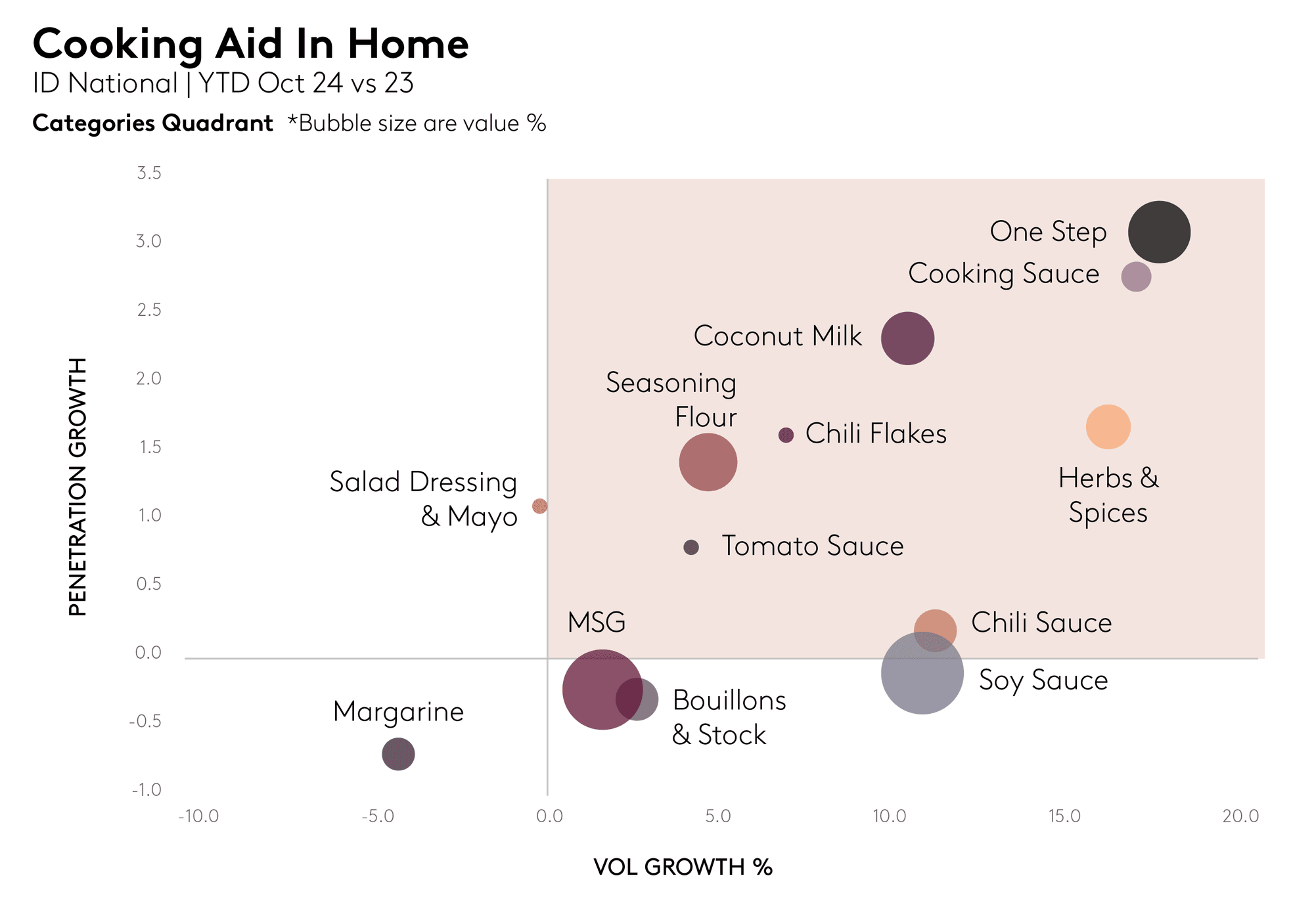

The cooking aid category is on an upward trajectory, with one-step meals emerging as a star segment. This reflects shoppers' growing preference for functional and time-saving products. Notably, the middle- and lower-classes are driving the rise of one-step meals, even as upper-class shoppers remain more experimental, exploring a broader range of categories.

Seasoning brand Desaku’s bumbu marinasi serbaguna variant exemplifies this trend, appealing to all consumer groups. For brands, embracing functional features and catering to the diverse preferences of different socio-economic classes is key. While upper-class consumers seek variety and innovation, the middle- and lower-classes represent a crucial market for essentials and convenience. Brands should focus on developing products that balance these demands, fostering growth in both experimental and functional categories.

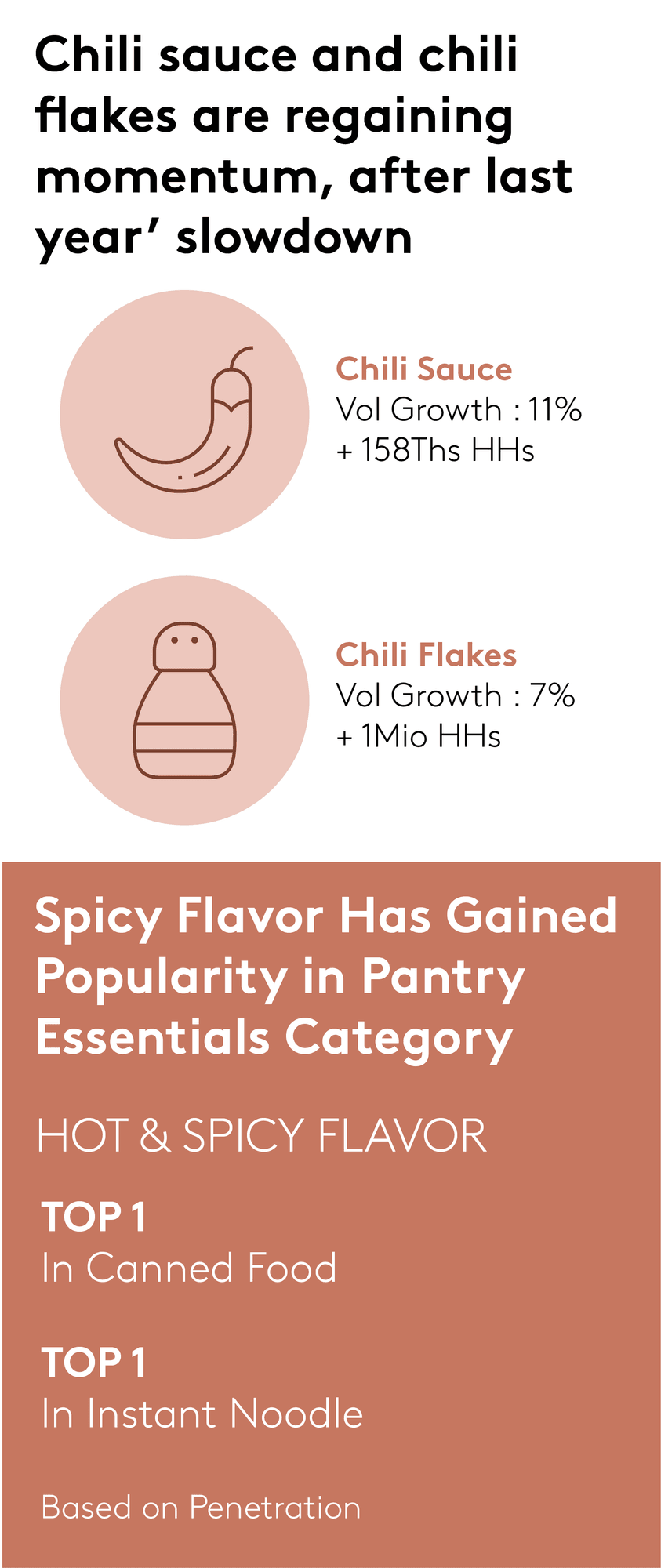

Indonesian consumers love bold flavours. There’s been a noticeable shift from salty to spicy, savoury, and garlic flavours, driven by the viral spicy food challenges on social media. This has led to a resurgence in chilli sauce and chilli flakes, with both segments achieving impressive growth and an expanded buyer base.

Spicy flavours now dominate key categories like canned food and instant noodles, presenting a golden opportunity for brands. By innovating with bold, exciting, and flavourful products they can tap into this growing trend, satisfying consumer cravings and staying ahead in the competitive market.

The Indonesian pantry essentials market is set for continued growth in 2025, driven by shifting consumer preferences and a focus on value and functionality. Staple products are recovering as price stabilisation boosts consumption, with both mainstream and emerging brands finding opportunities across various socio-economic classes. Quick-process products, particularly canned and frozen foods, will maintain their upward trajectory due to the ongoing demand for convenience.

In the cooking aid category, the demand for functional products like one-step meals is rising, especially among middle- and lower-class consumers seeking time-saving solutions. This presents opportunities for brands to innovate with essential and experimental offerings. The trend towards bold, spicy flavours also opens doors for differentiation.

In 2025, pantry essentials brands must align their products with evolving consumer needs and leverage innovation to drive growth.

The beauty industry is booming worldwide, with growth happening at a remarkable pace. In Indonesia, the beauty market is thriving as consumer demand continues to evolve. The challenge for beauty manufacturers now lies in identifying where to focus their efforts to maximise growth and stay ahead of the competition.

By understanding key trends and consumer behaviour, brands can strategically position themselves for success in this dynamic and ever-expanding market.

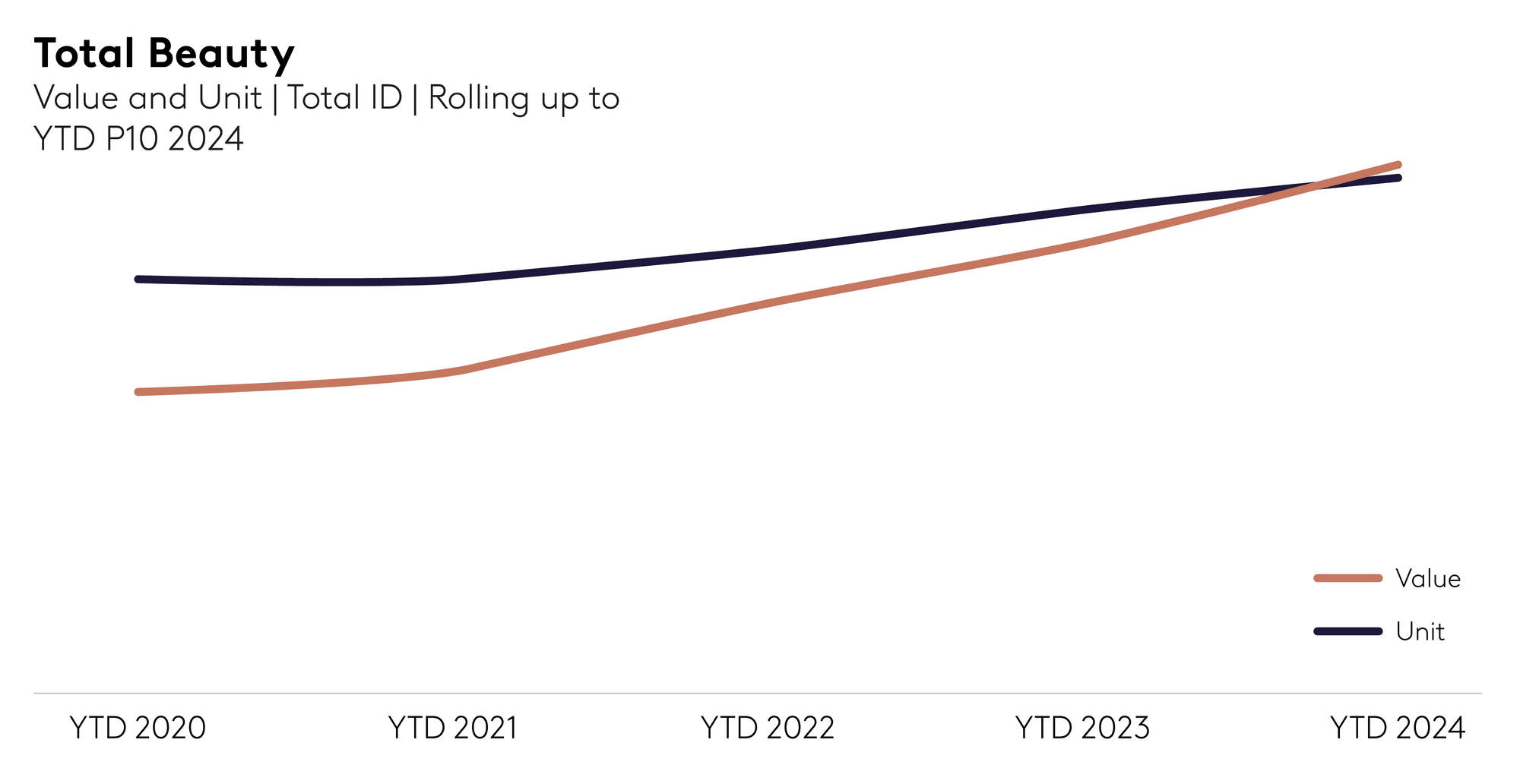

Indonesia's beauty market is fuelled by a diverse consumer base. Over the past five years, growth has been consistent across various metrics, with consumers purchasing more frequently, spending more, and buying higher volumes. These trends indicate a shift towards greater investment in beauty routines, with consumers seeking products tailored to their needs. This broad-based growth offers opportunities for beauty manufacturers to cater to diverse segments and drive continued market expansion.

A key driver of this transformation is accessibility. In today’s digital age, consumers expect quick access to information and products, and the beauty industry is responding with greater fulfilment of these demands. New and digital beauty brands are emerging alongside established giants, creating a dynamic landscape in which both large and small brands can thrive.

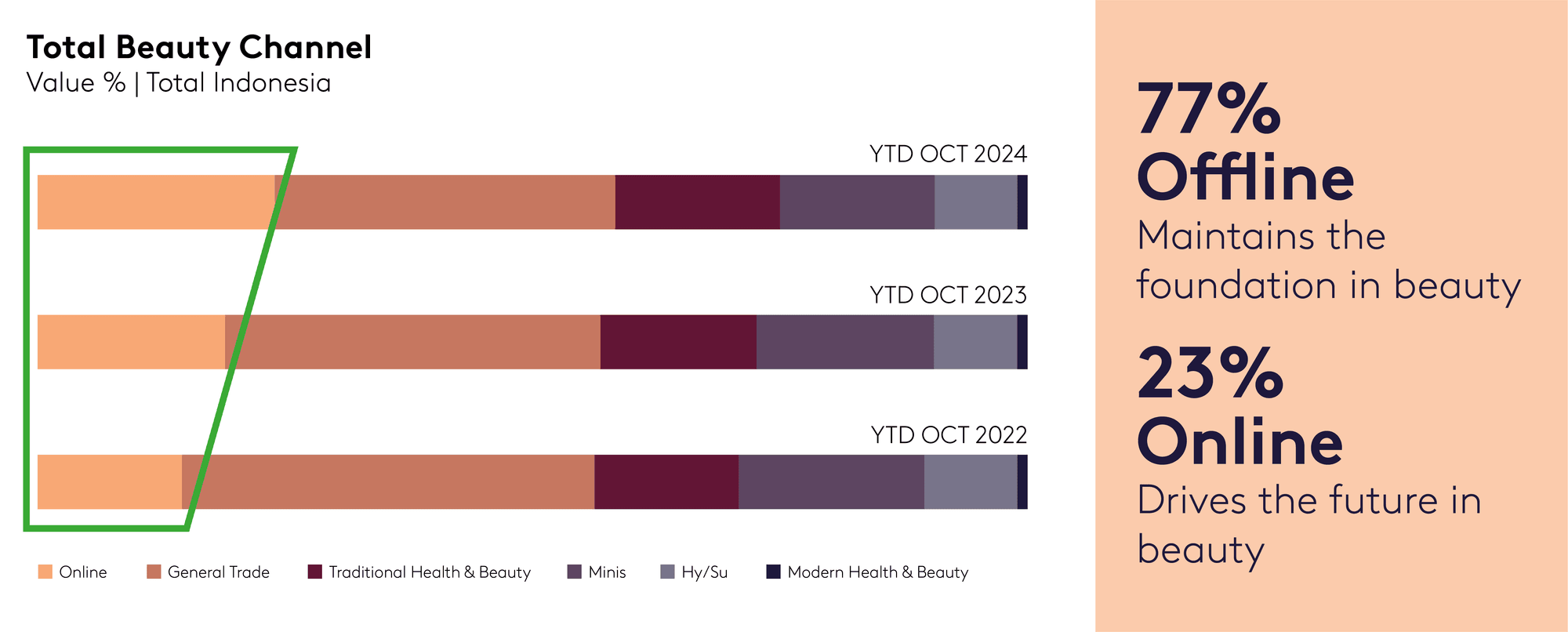

Consumers are increasingly shopping for beauty products across both online and offline channels. While online platforms are transforming beauty shopping, offline channels still account for 77% of the market.

Health & beauty stores, in particular, have become key hubs for offline shoppers, offering both availability and affordability. These stores are attracting more buyers, who are spending more, through delivering a seamless in-person shopping experience that resonates with those who value tangible product interactions.

On the other hand, online channels are reshaping the future of beauty shopping, driving growth with their convenience and appeal to tech-savvy consumers. The retention rate of online beauty shoppers has never been higher, with many consumers repeating their purchases and engaging more deeply with brands. This shift reflects the growing importance of beauty in daily life, as consumers seek products that cater to their specific needs and preferences through digital platforms.

By balancing their online and offline strategies, brands can effectively expand their reach and capitalise on the growing beauty market in Indonesia.

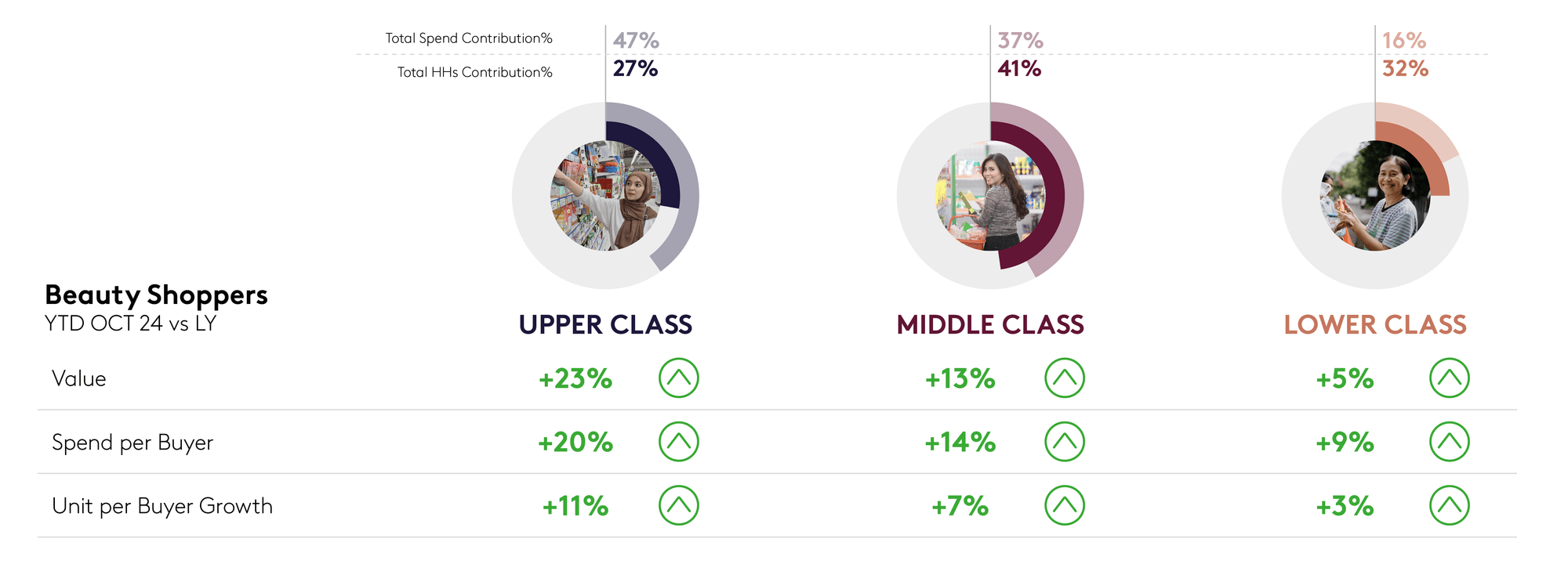

The beauty market in Indonesia is witnessing positive momentum across all socio-economic segments (SES), with upper-class shoppers leading the way in growth and spending. Known for their sophisticated spending habits, these consumers continue to invest in premium beauty products, pushing the boundaries of consumption despite levels of engagement that were already high. This group remains lucrative, consistently driving demand for high-end brands and advanced beauty solutions.

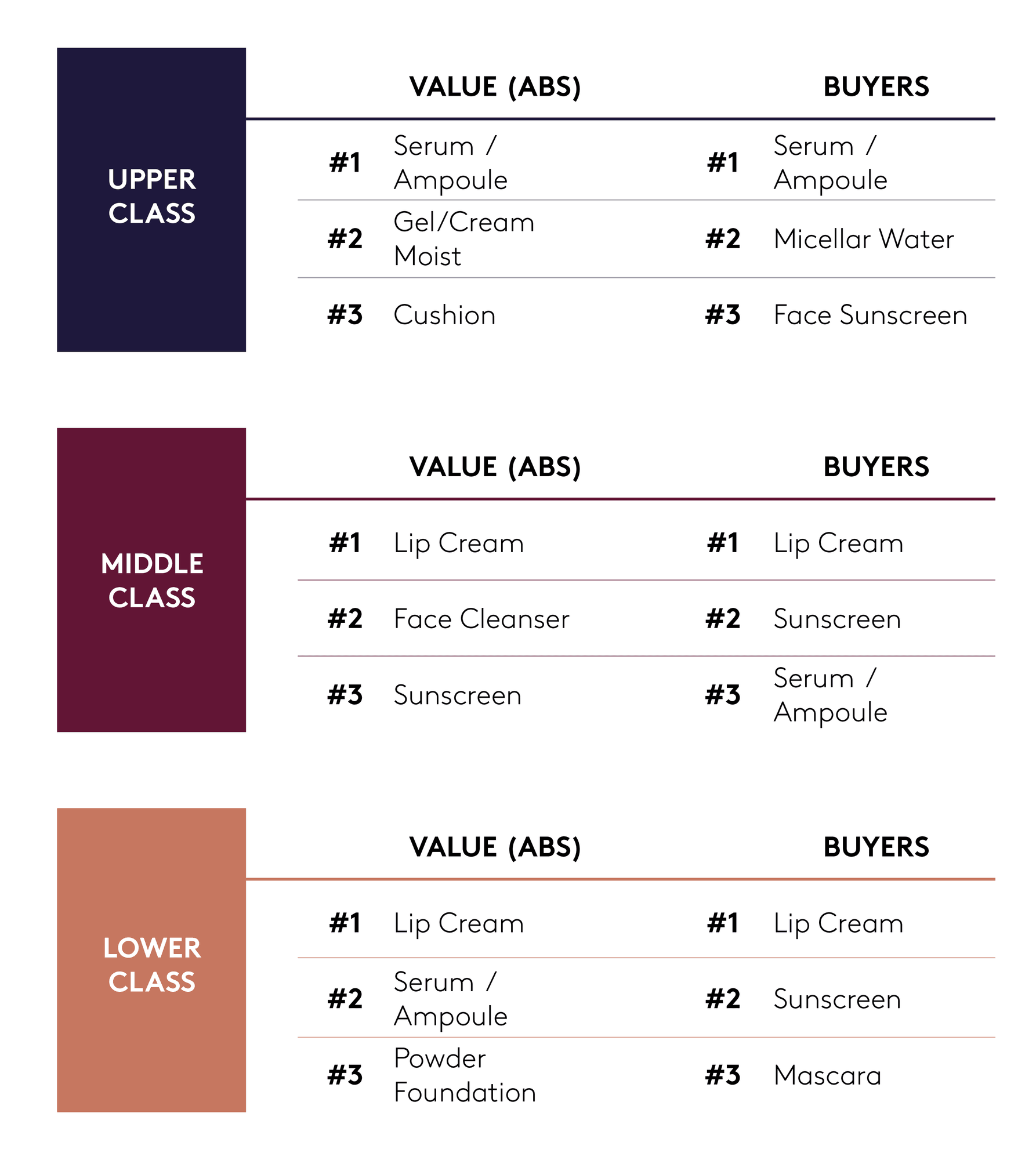

Products like serum/ampoule and lip cream have become favourites across social classes, with the upper-class showing a preference for premium options, as they further enhance their beauty routines with sophisticated and innovative offerings.

Meanwhile, middle-class shoppers are catching up, increasingly willing to expand their budgets as long as the products deliver value for money. These value-seeking consumers are becoming more discerning, focusing on products that meet their specific needs and expectations. Essential beauty items such as face cleansers and sunscreens remain staples, while lip cream continues to be a popular choice.

For lower-class consumers, known as trial generators, spending is more cautious but steadily growing. This group is still exploring new products and testing what works for them at an affordable price. Budget-friendly skincare and cosmetics provide a gateway into the beauty market, enabling these consumers to engage with beauty in a cost-effective manner.

The expanding budgets across all SES segments highlights the growing inclusivity and diversity within the beauty industry, offering ample opportunities for brands to cater to varying needs and preferences.

As we look ahead to 2025, the beauty industry in Indonesia is on a continued upward trajectory, with the past five years showcasing consistent growth. This trend shows no signs of slowing down, indicating that the market's potential remains strong.

Consumers are increasingly investing in their beauty routines, driving demand for a wide range of products that cater to diverse needs. Brands that can adapt to these evolving preferences and stay ahead of emerging trends will be well-positioned for success. The rise of online shopping is reshaping the beauty landscape, with digital platforms offering greater convenience and personalised experiences for tech-savvy consumers. However, offline channels will still play a significant role, as in-person shopping provides a unique opportunity for customer interactions and experiences that online platforms cannot replicate.

In addition, spending power is growing across SES with consumers in all groups showing a willingness to invest in beauty. Each segment presents different opportunities, but the overall trend suggests a growing market where beauty products are increasingly accessible to a wider audience.In this thriving market, beauty brands must strategically define their place by embracing both the rise of digital platforms and the enduring importance of offline experiences. With the growing inclusivity across SES groups and diverse consumer needs, there is a significant opportunity to empower beauty growth by delivering tailored, innovative products that resonate with every segment.

Impulse categories include ready-to-drink (RTD) beverages and ready-to-eat (RTE) snacks. These are consumed directly as impulse purchases out-of-home (OOH), and also as in-home (IH) purchases. Both occasions offer opportunities for brands to optimise the sector’s significant potential through different routes to market.

Impulse categories are a major contributor to FMCG, representing a substantial portion of consumer spending. The sector accounts for 40% of overall FMCG value in urban Indonesia across both in-home and out-of-home occasions, generating over 150 trillion rupiah by MAT October 2024. In total, four out of 10 FMCG purchases in the RTE and RTD segments are made OOH.

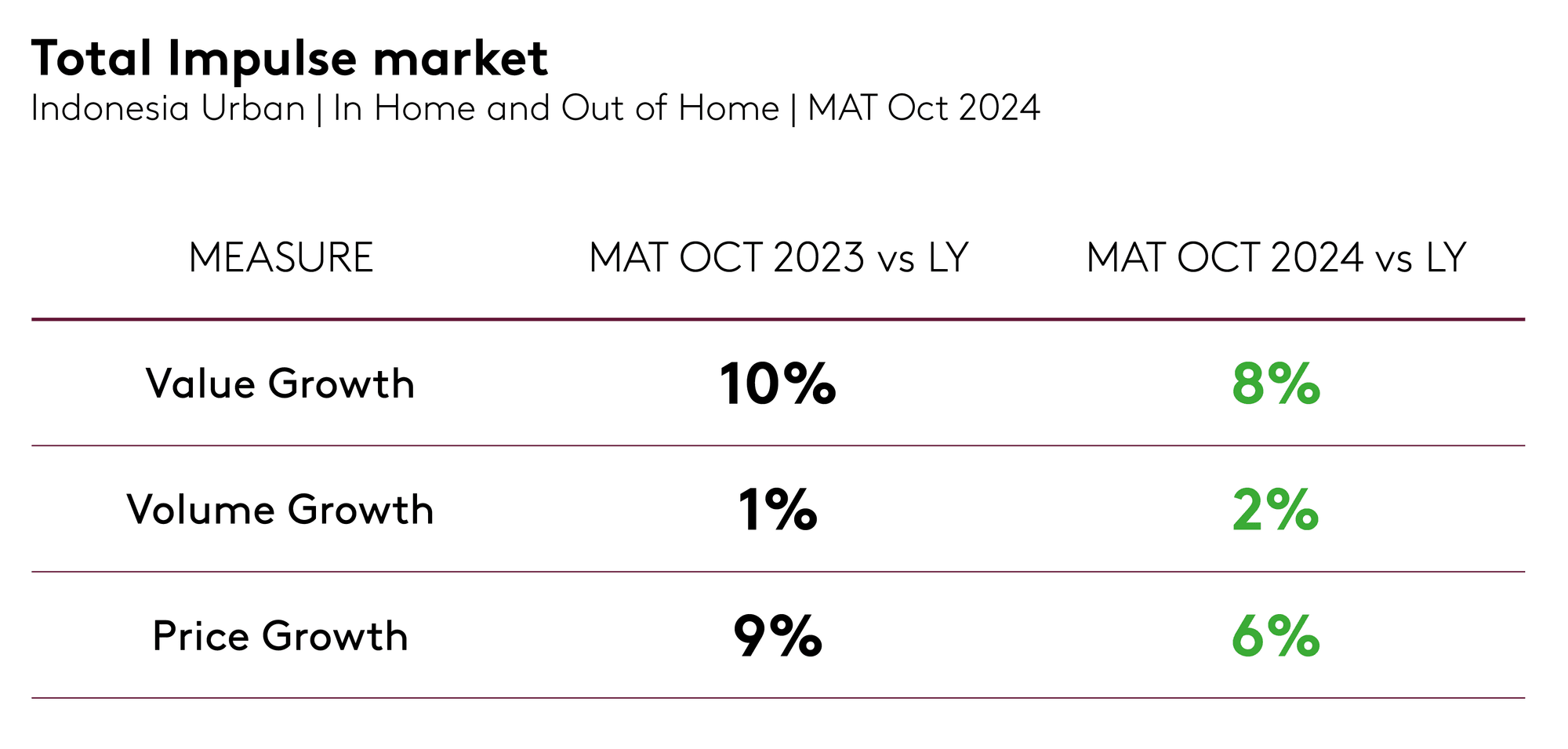

With an 8% growth in value in the last year, the impulse sector has outperformed the FMCG average, a stable growth from the previous year’s 10% rate which was driven mainly by price hikes. Despite price increases remaining a primary driver, the resurgence is evident in volume as well as value, with a 2% increase.

The OOH market in Indonesia shows great promise, as consumers return to pre-pandemic routines, increasing their demand for convenient, on-the-go options. Indonesians are significant OOH purchasers, particularly in the beverage sector, and especially non-dairy beverages due to their refreshing nature.

To win in the snacking and beverages sector, brands must excel in understanding consumers' shopping behaviour around impulse purchases and how it differs from categories driven by planned purchases.

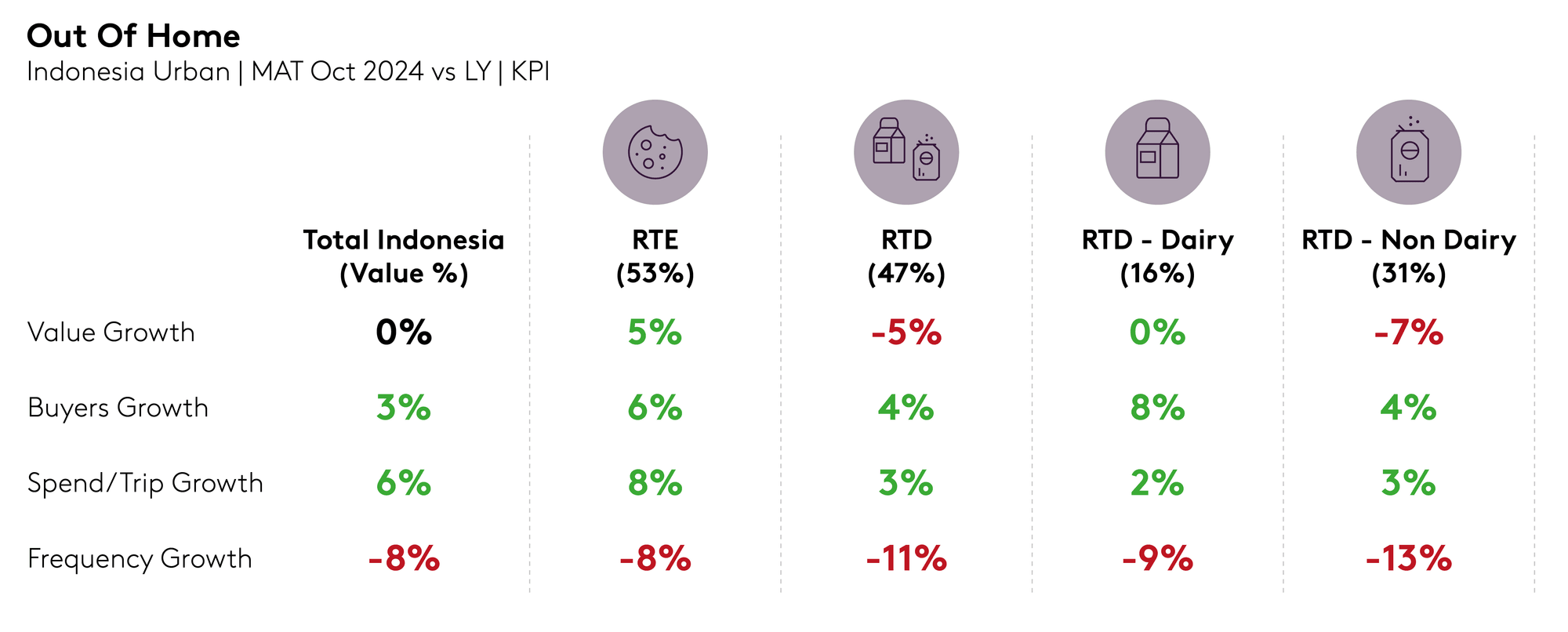

While both in-home and out-of-home purchases are growing, in-home performed more strongly in 2024, with growth visible across buyers, spend per trip, and frequency. OOH purchases exhibited more modest growth, with buyer and spend per trip growth offset by declining purchase frequency.

There are four key strategies that will help brands to win in Indonesia’s FMCG OOH market in 2025.

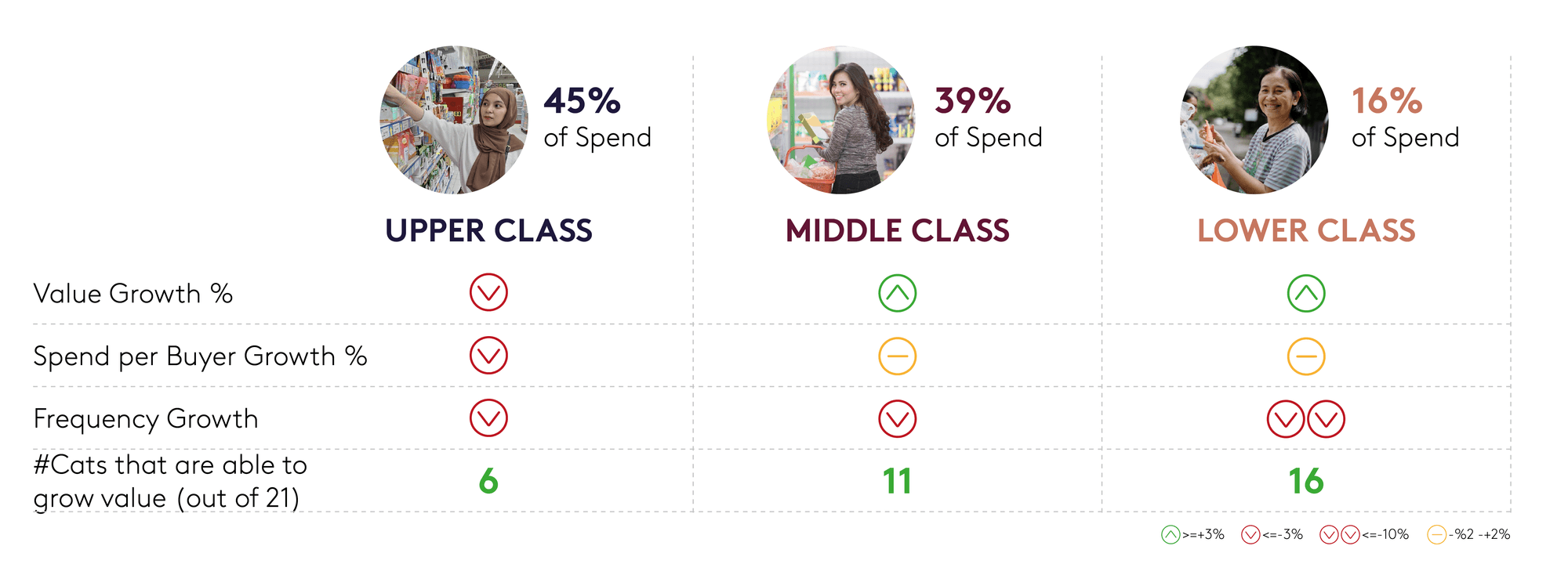

1. Leverage upper-class contribution

Households from the upper SES contribute nearly half of the total spend in impulse categories, and this is holding back overall sector performance due to a decline in purchase frequency and spend per buyer. While economic pressures more visibly affect the middle and lower SES, upper-class consumers are also adjusting their spending patterns. This has led to growth in only six out of 21 categories within this group, compared to 11 for the middle SES and 16 for the lower SES.

Interestingly, while upper-class spending on packaged impulse categories shows a negative trend, their overall expenditure, especially on dining out, remains positive. This indicates a shift towards spending on cafes, restaurants, and unpackaged beverages from channels such as mobile coffee and tea vendors, which are expanding rapidly. The trend highlights the growing competition between packaged impulse categories and dining-out occasions, emphasising the need to reignite excitement.

2. Recognise how priorities vary across age groups

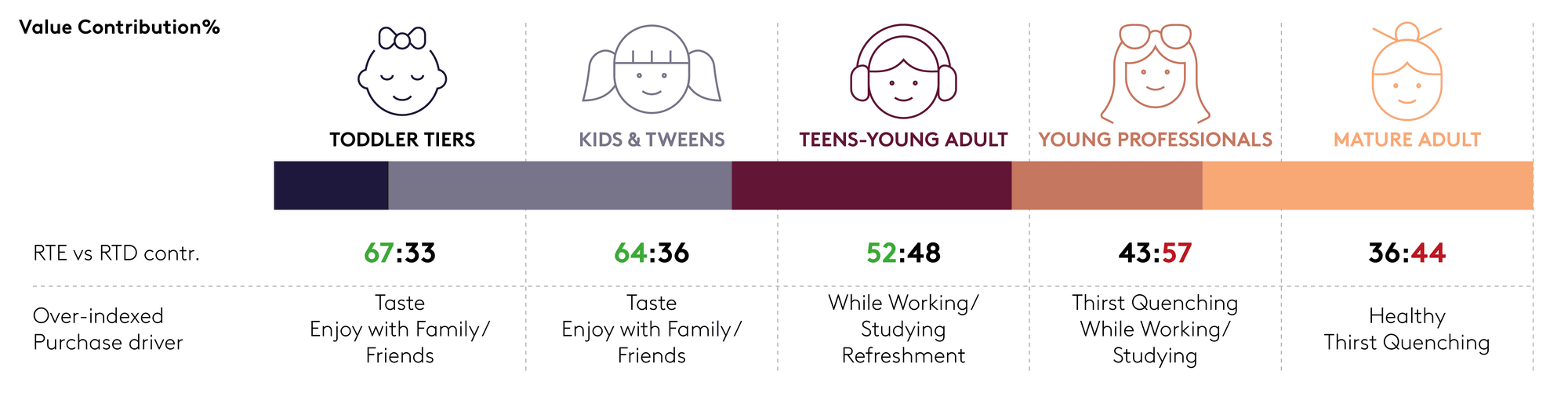

Different age groups show distinct spending priorities in impulse purchases. Younger consumers allocate two-thirds of their spending to RTE categories. This proportion declines as consumers age, with mature adults assigning two-thirds of their OOH spend to RTD beverages. This underlines the importance of providing hunger-satisfying products for younger consumers, and thirst-quenching options for older consumers.

Taste is a critical purchase driver for tweens and younger consumers. As consumers grow older, motivations like accompaniment during activities such as working or studying, refreshment, and ‘pick-me-up’ start to over-index. Health as a purchase driver is over-indexed among the mature cohort.

The rollout of government-funded school lunches could significantly impact spending behaviour among kids and tweens, who currently make 40% of their impulse purchases during school time, mainly on hunger-satisfying products like liquid milk and biscuits.

3. Offer options that support health

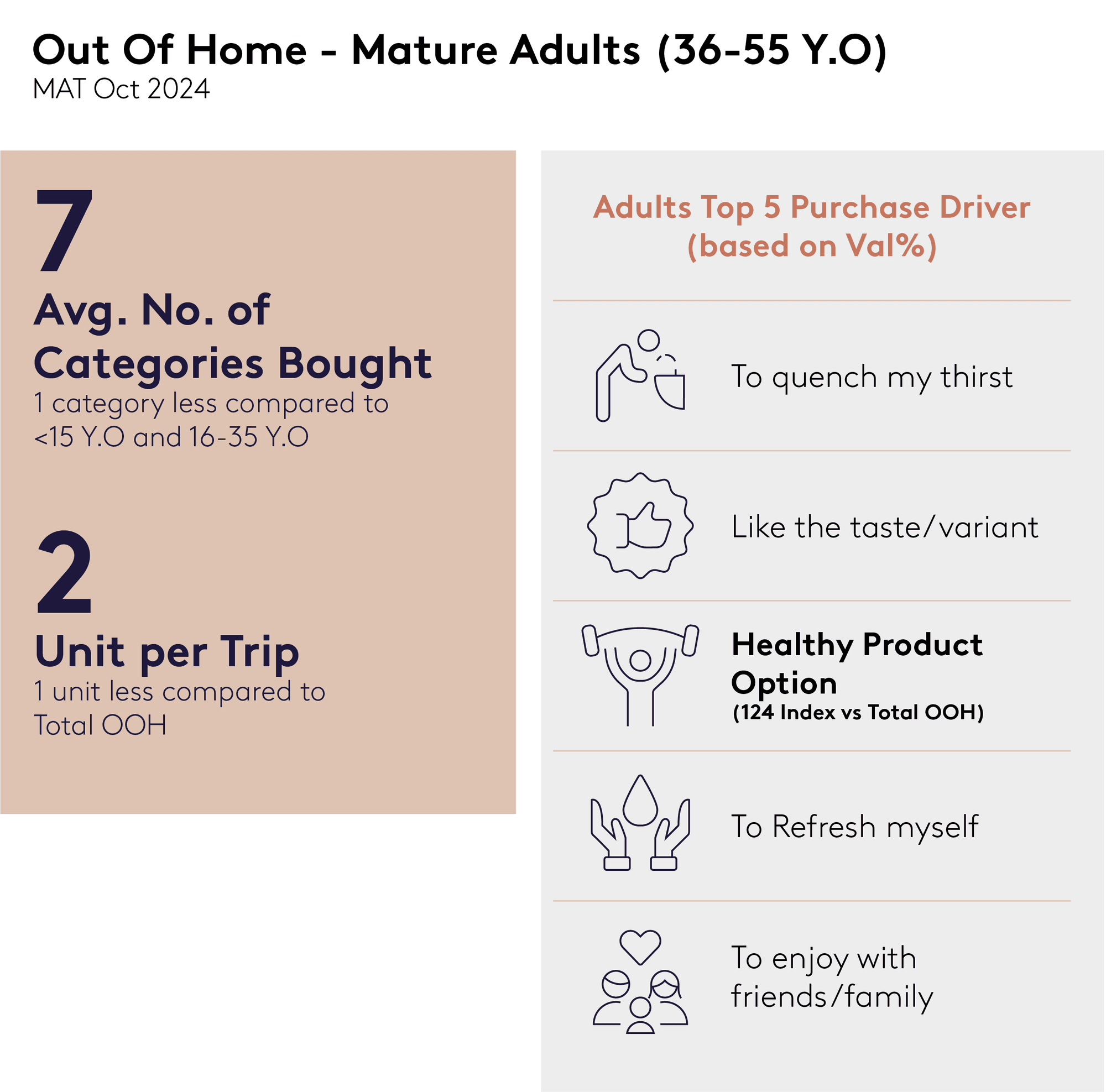

As shoppers age, their spending on OOH categories tends to decrease, with a growing preference for healthier products. This shift presents an opportunity for manufacturers to cater to mature adult shoppers by emphasising health-focused value propositions. Brands that highlight health benefits can better align with this demographic's priorities.

Key purchase drivers for adult shoppers include quenching thirst, taste preferences, and health consciousness. Refreshment and social enjoyment also play pivotal roles in their decisions. By offering products that balance these factors – particularly health and taste – manufacturers can effectively capture the interest and loyalty of this mature consumer group.

4. Balance exploration with innovation

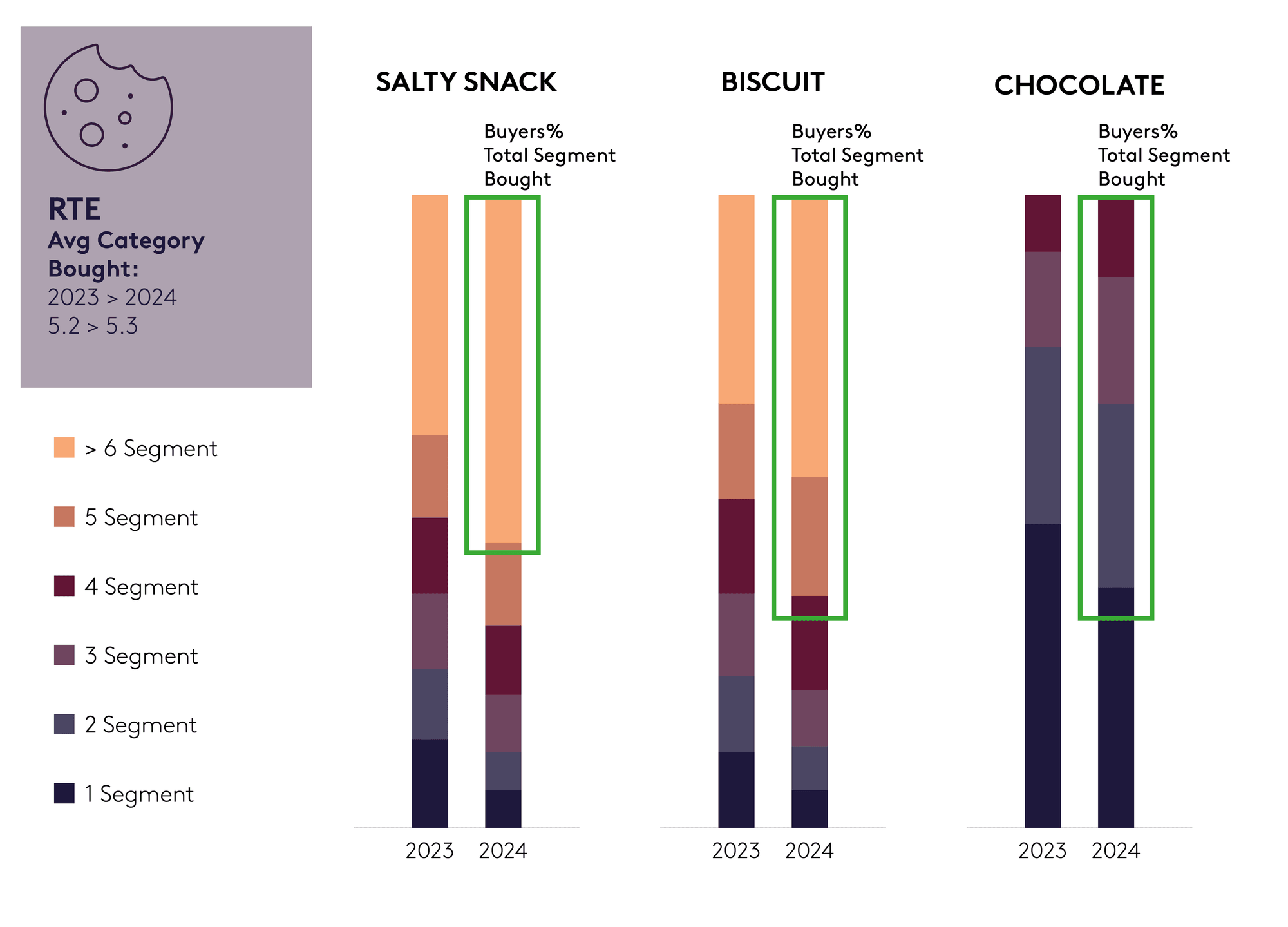

Indonesian consumers are highly explorative in impulse categories, especially snacking, and this trend is growing. An increasing proportion are purchasing multiple segments in biscuits, salty snacks, and chocolates. This highlights the necessity of keeping consumers engaged and excited.

However, the trend also indicates that consumer loyalty is not guaranteed. Maintaining loyalty will become increasingly challenging without ongoing innovation and portfolio expansion, especially within the snacking space.

In 2025, the Indonesian OOH market is set to evolve with a focus on health-conscious and innovative products that cater to the diverse needs of different consumer segments. Brands will need to capitalise on the growing demand for healthier options among mature adults, while continuing to engage younger consumers through taste-driven and hunger-satisfying products.

The competitive landscape will further intensify as dining-out occasions and unpackaged beverages gain traction, pushing packaged impulse categories to innovate and reignite consumer excitement.

The ability to understand consumer behaviour across different SES and age groups will also increase in importance. Tailoring products to meet the specific needs of each demographic will be crucial. In addition, maintaining consumer loyalty will require a constant stream of new and engaging products, with brands needing to balance exploration and innovation to stay ahead in this dynamic market.