BDS One Year On

Understanding Shopper Shifts, Loyalty Challenges, and Growth Opportunities in a Changing Consumer Landscape

Following the events of 7 October 2023, the conflict between Hamas and Israel escalated significantly, leading to the resurgence of the global Boycott, Divestment, and Sanctions (BDS) movement. Malaysia has emerged as one of the most ardent supporters of the BDS movement, highlighting the necessity of evaluating its ramifications on Malaysia’s FMCG (Fast-Moving Consumer Goods) market. This evaluation is vital to understanding the challenges faced by the industry and identifying strategies to either mitigate these challenges or seize emerging opportunities for growth.

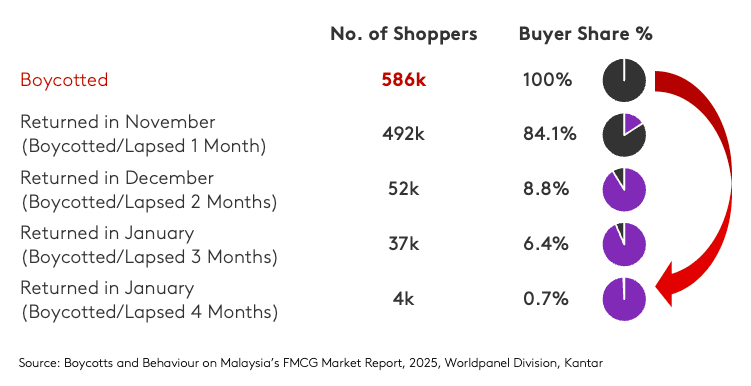

The boycotts were initially significant, with 586,000 shoppers lapsing in the first month, accounting for 8.8% of pre-boycott buyers. Before the boycotts, manufacturers targeted by the movement had 6.6 million buyers.

However, this boycott period was relatively short-lived. Over time, all shoppers eventually returned to purchasing from at least one boycotted multinational corporation (MNC) by February. This suggests that while the boycott had a noticeable impact in the early stages, it did not lead to a permanent shift in consumer behaviour but rather a temporary disruption.

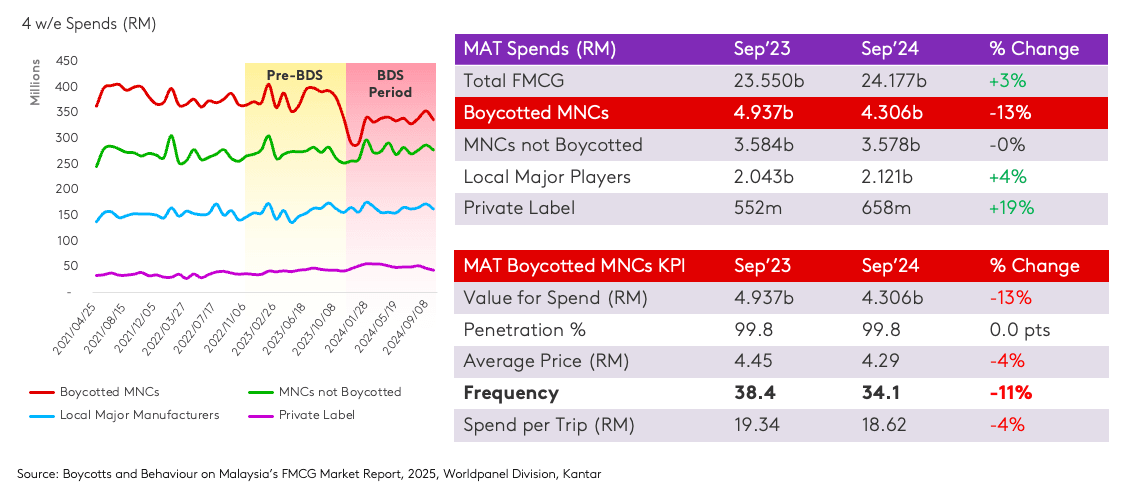

While consumers continued to buy from boycotted MNCs, their purchasing patterns underwent significant changes. They reduced their spending, made fewer shopping trips, and opted for smaller quantities. In contrast, other manufacturer types either maintained their market positions or recorded notable growth during the same period. This juxtaposition underscores the competitive shifts in the FMCG landscape.

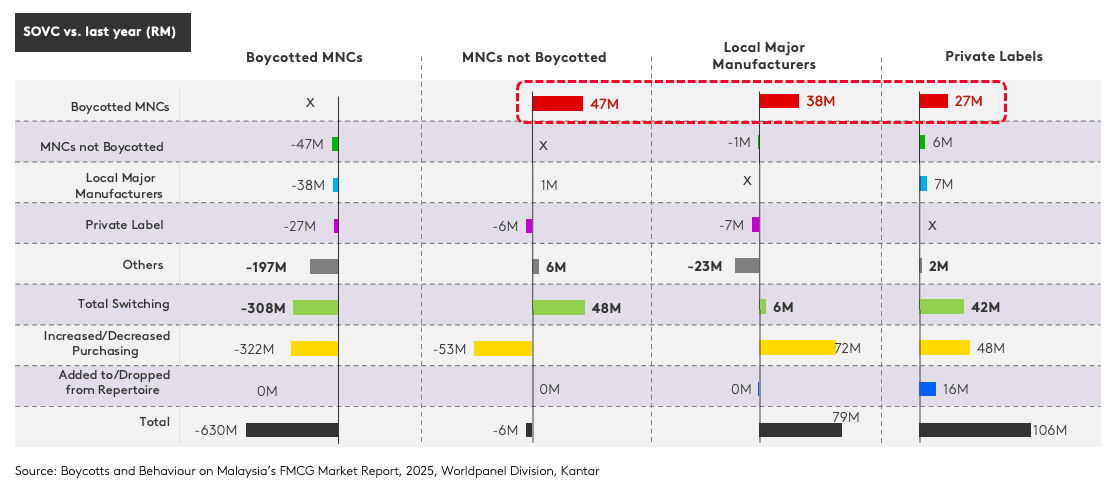

The downturn experienced by boycotted MNCs was primarily driven by two factors: a reduction in overall purchasing and a significant degree of switching. Rival manufacturers were the clear beneficiaries, capitalising on the switching gains.

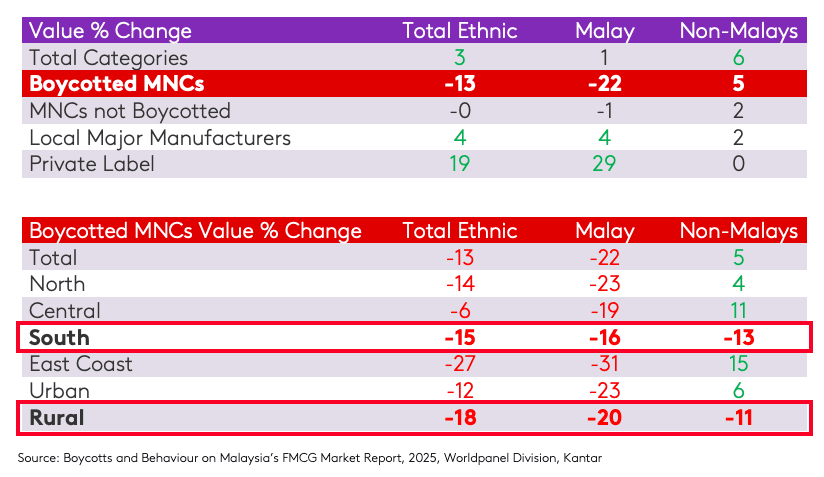

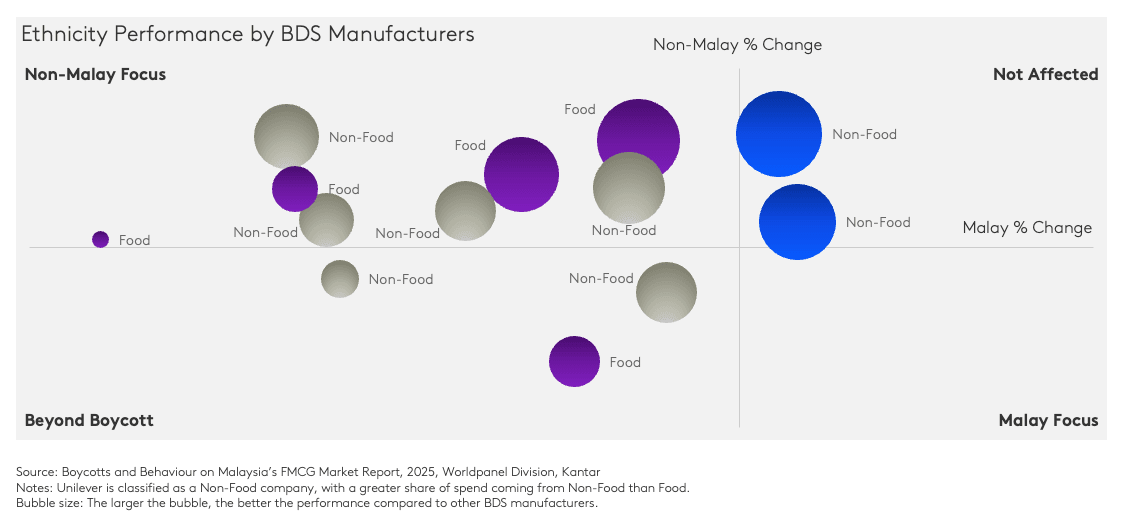

However, the impact of the BDS movement was not uniformly distributed across Malaysia. The movement was predominantly led by Malay households, who showed a preference for local manufacturers and private labels. Meanwhile, non-Malay shoppers, who make up less than 40% of Malaysia’s population, increased their spending on boycotted MNCs. A common trend observed across ethnicities was a decline in purchasing in rural areas and the southern region, which has a largely rural demographic similar to the East Coast. However, the South is showing signs of recovery recently, indicating a potential rebound in these areas.

During this period, only two boycotted MNCs recorded growth, both of which operated in the non-food sector. However, being in the non-food category did not guarantee immunity from decline. Several non-food companies also experienced setbacks, even among non-Malay shoppers.

This highlights that retaining non-Malay consumers was critical for the survival of boycotted MNCs, reinforcing the need for a deeper understanding of diverse consumer behaviours and the factors influencing brand loyalty in the wake of the boycott movement.

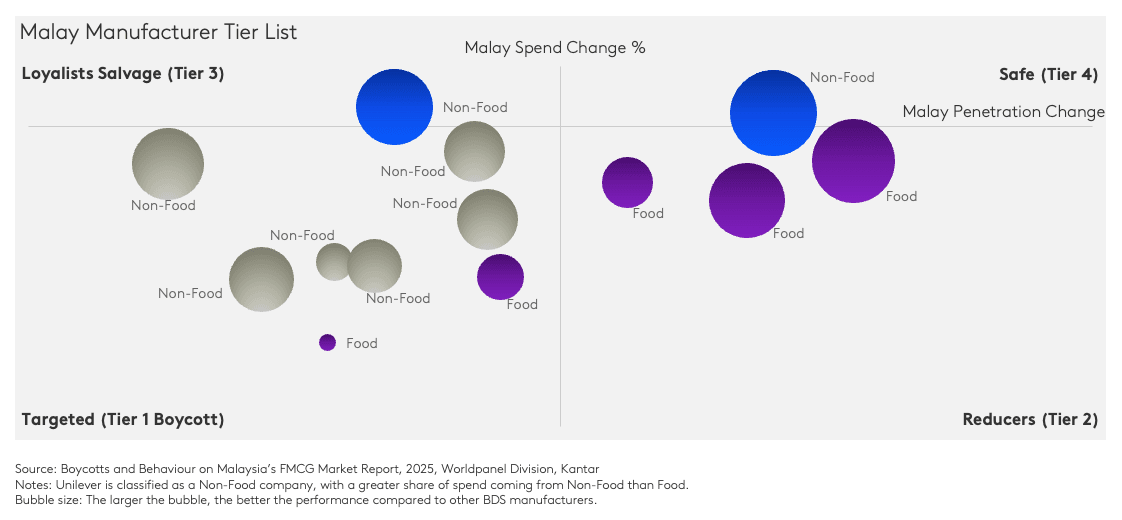

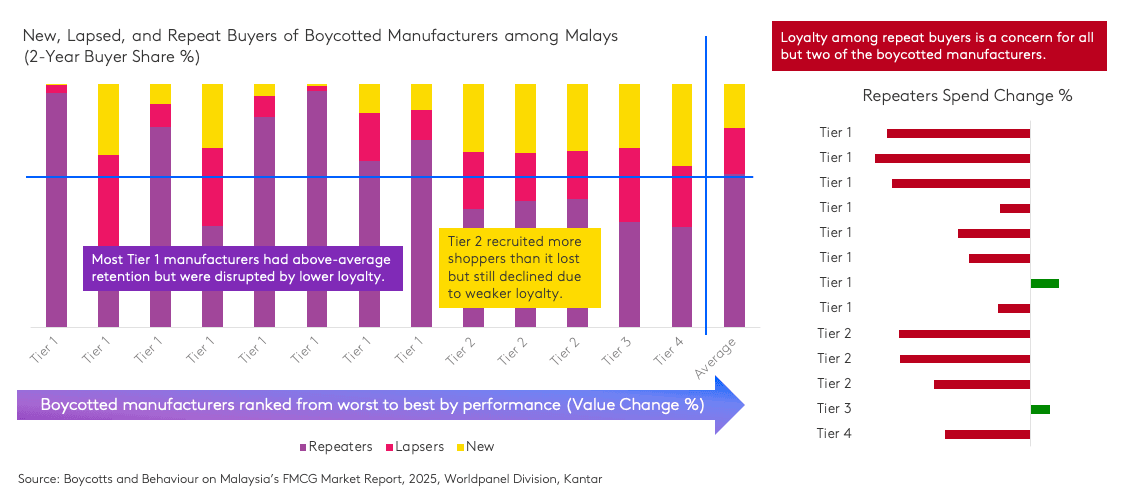

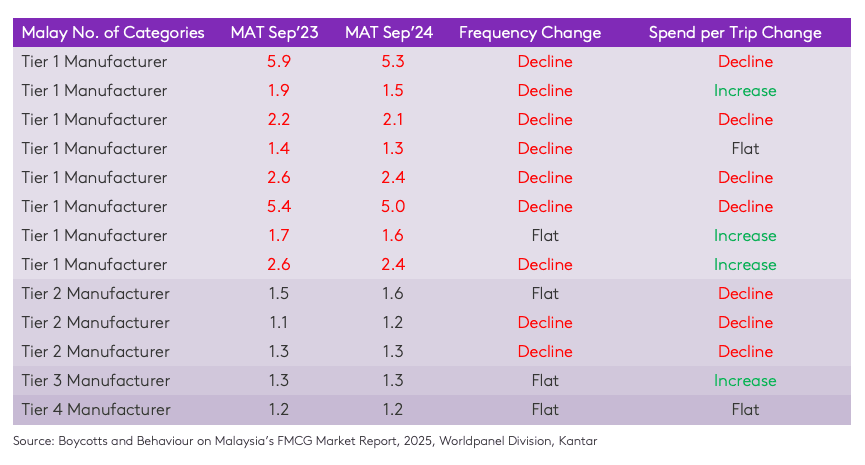

The effects of the boycotts varied significantly across manufacturers. Most boycotted MNCs experienced declines in both shopper numbers and loyalty. However, the impact differed between food and non-food categories. Shoppers were more likely to completely stop purchasing from boycotted non-food brands,

whereas boycotted food manufacturers managed to retain or even grow their shopper base, albeit with much lighter purchasing behaviours. For certain manufacturers, loyalty played a crucial role, allowing some to maintain or even grow despite losing shoppers. This underscores the complexity of consumer responses to the boycott, where retention strategies and purchase intensity became critical factors in determining long-term brand resilience.

Loyalty emerged as a critical factor during this period, with declines observed across the board for boycotted MNCs. While shoppers may have stopped purchasing specific brands within a boycotted MNC’s portfolio, high overall retention rates indicate that they continued buying other products within the same portfolio. This suggests that boycotts did not lead to a complete exit but rather a selective shift in purchasing behaviour. Interestingly, some MNCs with above-average retention rates were still among the most boycotted, highlighting the complexity of consumer responses. To navigate this challenge, it is crucial to identify products with stronger retention rates and leverage these as key assets for recovery and brand resilience.

This report serves as an introduction to the comprehensive analysis of the challenges and opportunities facing boycotted MNCs in Malaysia. Key areas for further exploration include:

Identifying categories where shoppers lapsed and those that mitigated declines,

Assessing whether a focus on more affordable or premium SKUs is optimal,

Evaluating the effectiveness of promotional strategies deployed by boycotted MNCs over the past year,

Highlighting retail outlets with the greatest potential for growth, and

Defining short-term key performance indicators (KPIs) to support the recovery and resilience of boycotted MNCs.

Understanding shopper behaviour and market dynamics will help you navigate challenges and grow sustainably.

Contact our experts for more details.