A Tale of 25 Billion Choices

Decoding the demands of omnishoppers

In the turbulence of Latin American markets and the seemingly endless digital scroll of e-commerce, a complex narrative unfolds — one where 25 billion products sold represent a story deeper than mere transactions. It’s a story of desires, needs, and aspirations for 131 million households navigating the omnichannel landscape.

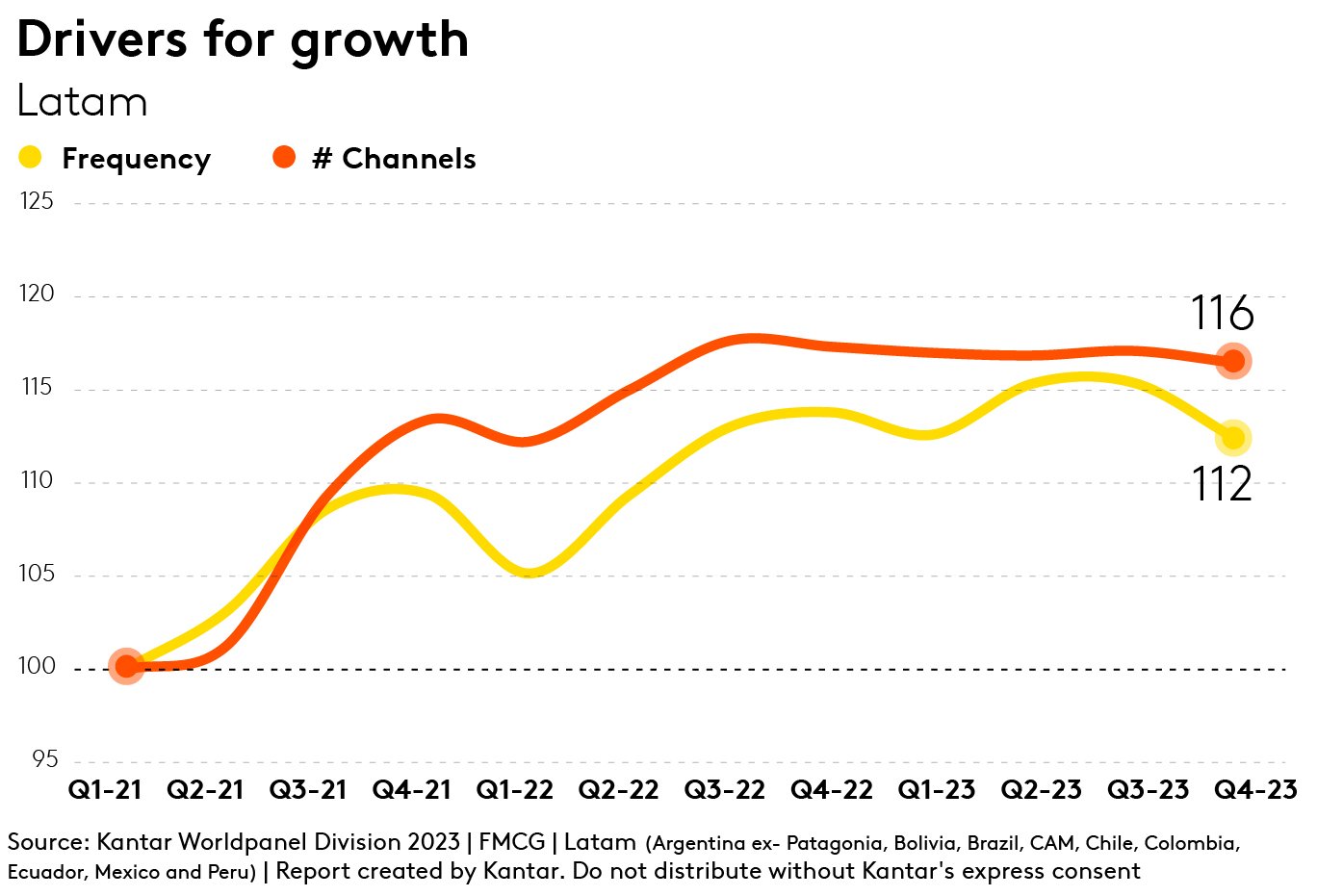

There’s no doubt those households have witnessed and activated change, but over the last two years, we've also seen a phase of cross-channel consolidation within Latin America's retail ecosystem. The lines of frequency and channels have come closer together even as inflation pushed further ahead.

Think of it as a mosaic of consumption occasions, each one a microcosm of decision-making. This isn't just about what's on the table; it's about the confluence of price, quality, and convenience, a delicate balance that households across Latin America juggle with every purchase. With an average of 195 shopping occasions per household annually, each decision is made inside a broader chameleon-like narrative of resilience and adaptability. And each decision is across a vast retail channelscape.

So what have these cross-channel decisions entailed? Our data delineates the propulsion factors of the Latin American omnichannel market. In it, we see the oscillation in purchasing frequency and the diversity of channel utilisation. But we also see clear signs of stabilising trends.

In 2021, the pandemic sparked something we’ve long been tracking and analysing - wider use of shopping channels as people spent time in lockdown and working from home. The trend continued as economic challenges and rising living costs grew throughout the second half of 2022, and shoppers became more channel-agnostic as they sought out the best value.

However, in recent times, the chameleon shoppers made another adjustment. They slowed their habits of exploring new channels, and the preferred channels reached a plateau — a trend that extends into the current year. We’ve begun to characterise this plateau as "omnichannel consolidation." It is an era indicative of the market's gradual equilibrium and consumer adaptation to new purchasing rhythms, especially as they orchestrate their spending to offset price rises.

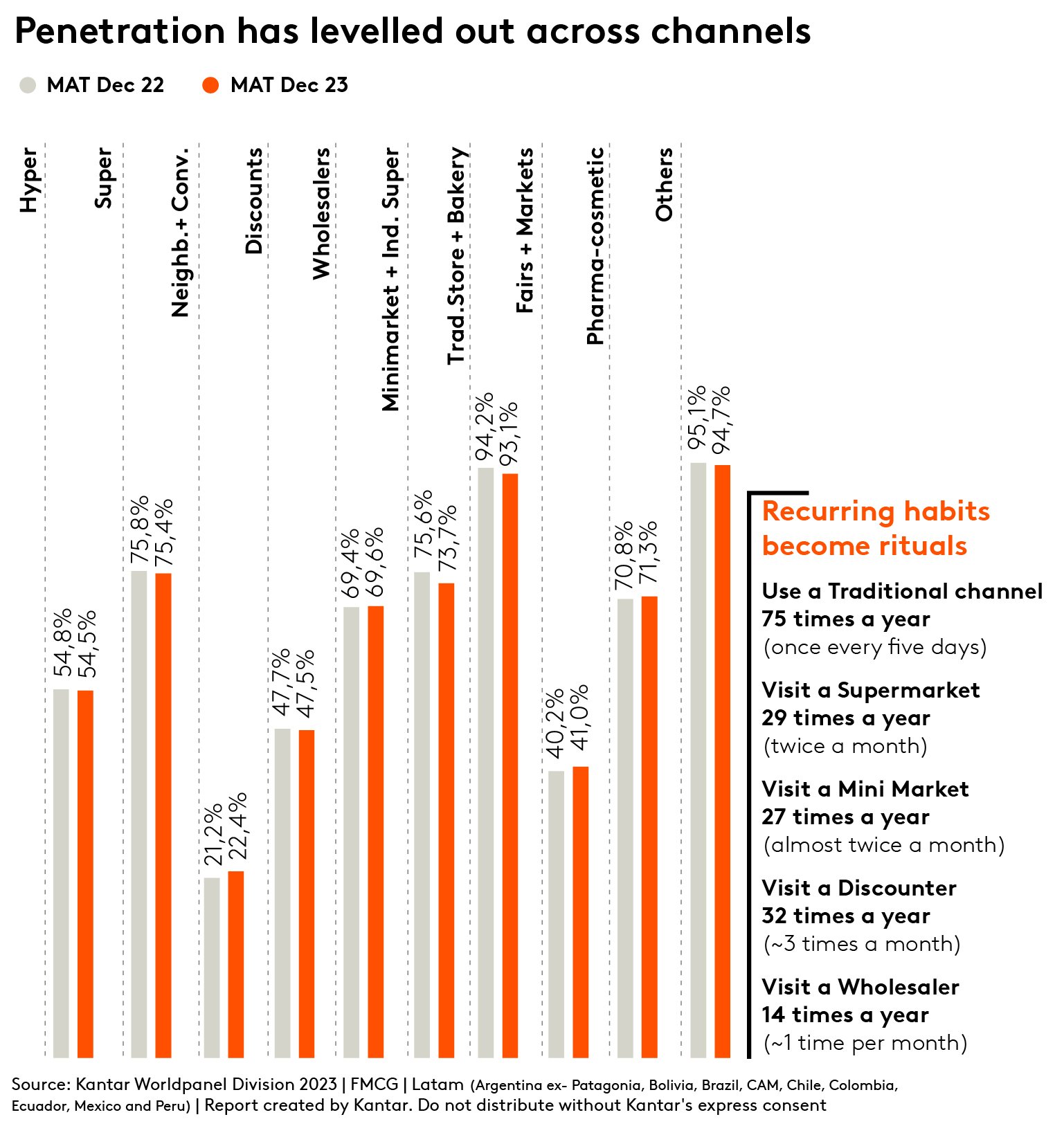

Traditional channels, including bakeries, still retain a substantial foothold with over 70% penetration. But a nuanced narrative is unfolding even around this dominant retail channel, and a stable channel environment doesn’t mean an easy channel environment.

Habits around channel repertoire are now recurring – they are becoming rituals. Hence the more stable channel penetration numbers. What does this mean and what are the implications? It means consumers are now applying more consistency and hierarchy to their shopping behaviour. Channels that were once nascent, such as discounters, now account for an average of 32 shopping trips per year.

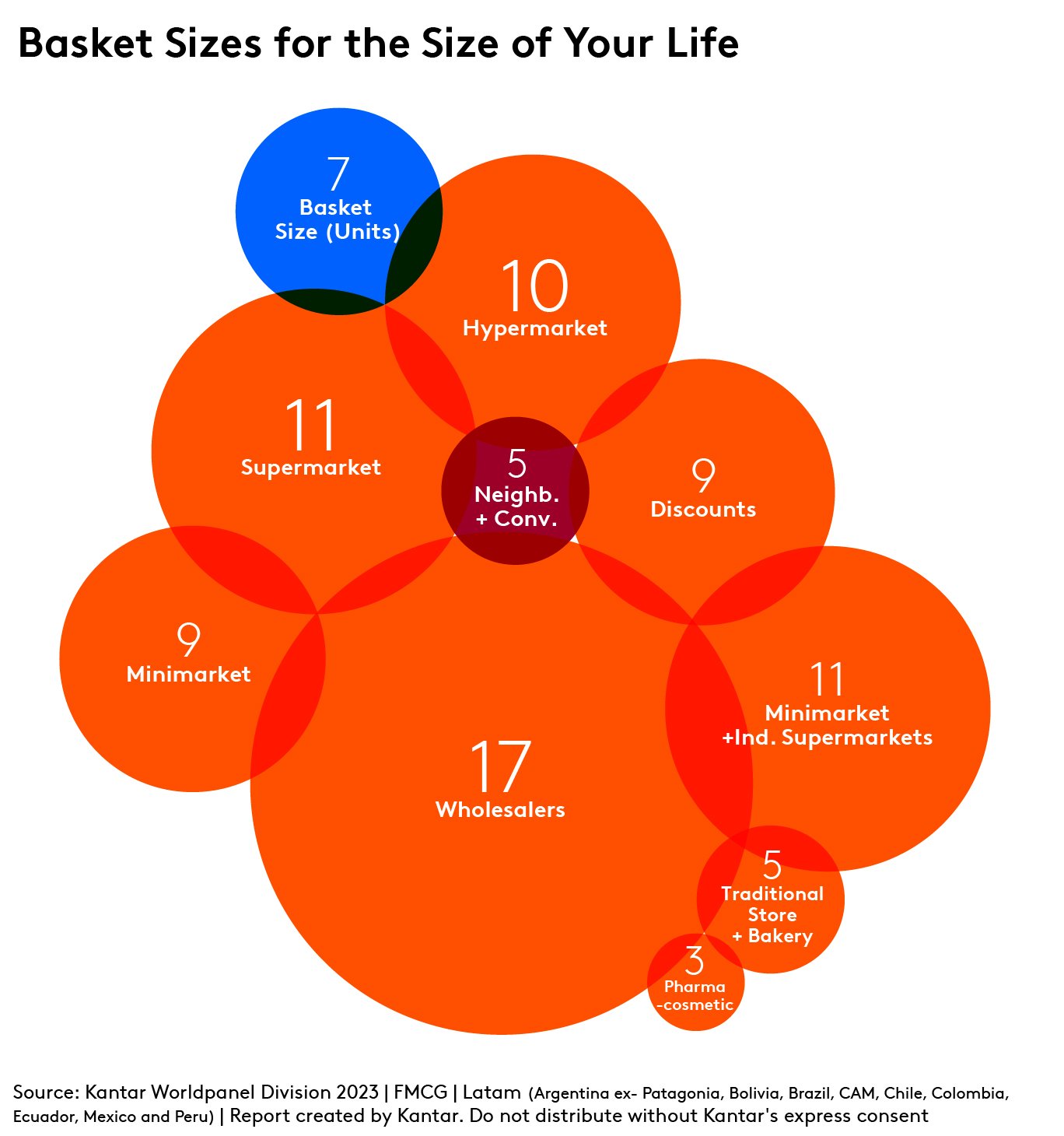

Such a dynamic, of course, means basket changes aplenty. Unsurprisingly, category management is now a bigger priority than ever as we see basket sizes rebalance.

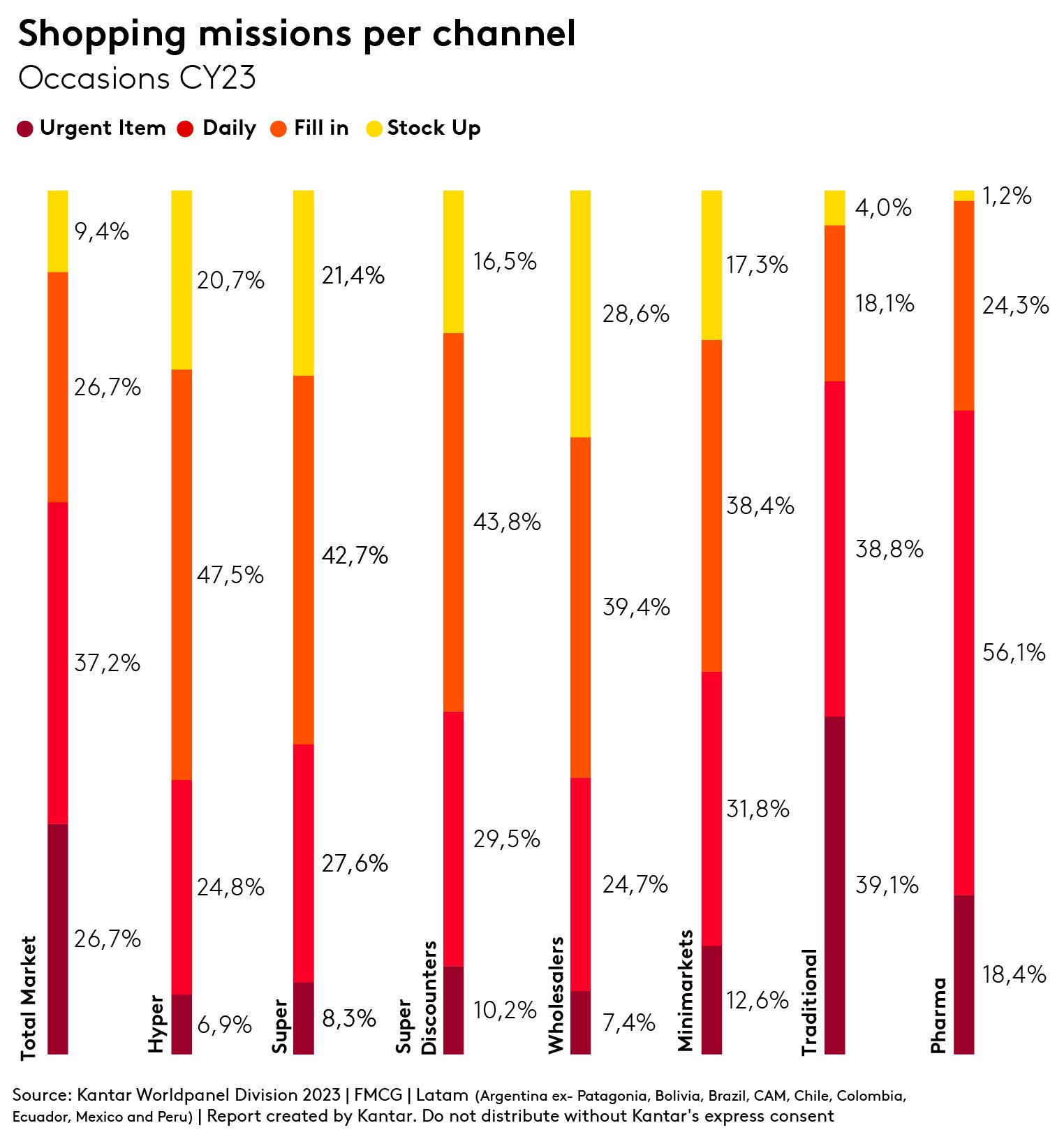

Of course, not all store visits are created equally. For example, as we can see in the graph, although the number of visits is similar between hypermarkets and wholesalers, their shopping missions are notably different. Hyper, supermarkets, and discounters are mainly for "Fill-in" purchases, while wholesalers are more concentrated in "Stock Up." Minimarket and traditional trade outlets are for daily or urgent needs. However, these channel roles are continually evolving, and the retail landscape is dynamically adjusting along with the shifting preferences of our chameleon consumers.

Mercurial and cunning, navigating the retail terrain with aplomb, the chameleon shoppers of Latin America orchestrate billions of retail transactions each year. As they adapt to the times, the form of each transaction increasingly matters, morphing tactics to extract maximum value from their inflation-stricken wallets.

They've become experts at finding the best deals and are willing to traverse a wide range of retail channels to stretch their budget further. They adapt, facing tough situations like supply chain problems or changes in weather that can raise food prices.

These chameleon shoppers are smart and resilient. When prices rise, they turn to places where they can save money, and when certain items are hard to find, they explore other stores that might have what they need. Their loyalty isn't just to one store or brand but to smartly take care of their household needs.

They’re increasingly settling on a core set of channels that, together, meet their needs.

The leap into the digital realm is perhaps the most striking adaptation. Once limited by access and infrastructure, today's Latin American consumer is increasingly digital-first, with a significant portion of these being mobile transactions. This shift is underpinned by an expanding digital payment landscape, which has democratised access to online markets for a wider section of the population. With this, we have also seen an increasing trend among our digitally connected consumers to research products online before purchasing them in physical stores.

Access to credit cards and digital wallets has emerged as a game-changer in the omnichannel environment. There has been an increase in consumer spending that can be attributed to easier credit and spending instruments. This access has also enabled consumers to make larger, more strategic purchases online, further blending the lines between online and offline shopping experiences.

Beyond economic tactics and digital adoption, Latin American shoppers display a nuanced understanding of the retail ecosystem. They are not merely reacting to changes but are actively shaping their shopping journeys. They use online research to compare prices, seek out reviews for quality assurance, and engage in community groups to exchange tips on finding the best deals. This behaviour reflects a deep-seated cultural adaptability, where the value of a purchase is measured not just in currency but in the satisfaction of outsmarting the system.

In synthesising these trends, it becomes clear that the chameleon shopper is not a passive participant in the retail ecosystem but a dynamic force driving change.

A digital native who thrives on the convenience of one-click purchases. She shops across other channels, but for her, e-commerce is more than a platform; it's a way of life. She navigates deals with precision, her shopping cart a harmonious blend of 'Fill In' staples and 'Stock Up' savings.

Elena’s example speaks to the growing digital marketplace and Mexico's leap into e-commerce, where choice and convenience meet at the crossroads of technology. However, she also uses digital platforms to price compare across all channels

Carlos is a ‘value seeker’, the hero of his household budget, each visit to the store is a quest for better prices with minimal sacrifice on product or quality.

In the aisles of his local discounter in Colombia, he weighs the scales of brand preference against private label savings, his loyalty card a shield against inflation.

Carlos' journey across all retail channels is driven by price, but he increasingly finds himself using discounters. His life offers a reflection of the real-life tensions of a shopper balancing quality, cost, and the satisfaction of returning home with a bag of well-priced goods.

Meticulous mum, Juliana, orchestrates her big monthly shop, balancing the demands of her career and kids with the needs of her pantry. She’s increasingly drawn to wholesalers for their balance of brand variety, and promotional deals.

Her shopping list a finely-tuned symphony of meal plans and household needs. Juliana's balancing act gives us insight into the life of a Brazilian shopper where wholesalers offer a haven of variety and bigger pack sizes. Of course, there are days she is forced to opt for convenience channels to grab last minute items, or quick treats.

The preference for wholesalers in Brazil is underpinned by a combination of economic necessity and strategic choice. Consumers are drawn to these venues for several reasons:

Cost Savings: The primary draw of wholesalers is the potential for significant cost savings when purchasing in bulk.

Convenience: By stocking up in fewer, larger trips, families can reduce the time and energy spent on frequent shopping excursions.

Value of Bulk Purchasing: There is an inherent value found in buying larger quantities, which can offer per-unit cost advantages that are critical in a tight economic environment. To accommodate rising demand, wholesalers are also moving new store locations to more inner-city neighbourhoods.

As the channel landscape in Brazil stabilises, the role of wholesalers solidifies, becoming a habitual part of the shopping routine for budget-conscious consumers. This trend is reflective of a broader shift in consumer behaviour, where efficiency and value are prized.