Rhythm of Retail

Winning the wallets of the channel changers

But what does the true pulse of the market look like? In truth, it’s a maze; a vibrant interplay of channels and growth drivers sculpting a retail landscape worth over $200 billion in sales.

Traditional trade outlets, celebrated for their local connections and personal touch, continue to be influential, highlighting the enduring appeal of human-centric retail experiences. Yet, simultaneously, the retail landscape in the region is becoming more sophisticated and mature. This evolution is marked by an ongoing increase in discounters and e-commerce platforms, which in large part reflects a shift in preferences towards greater value and convenience. As always, the chameleons are on the move.

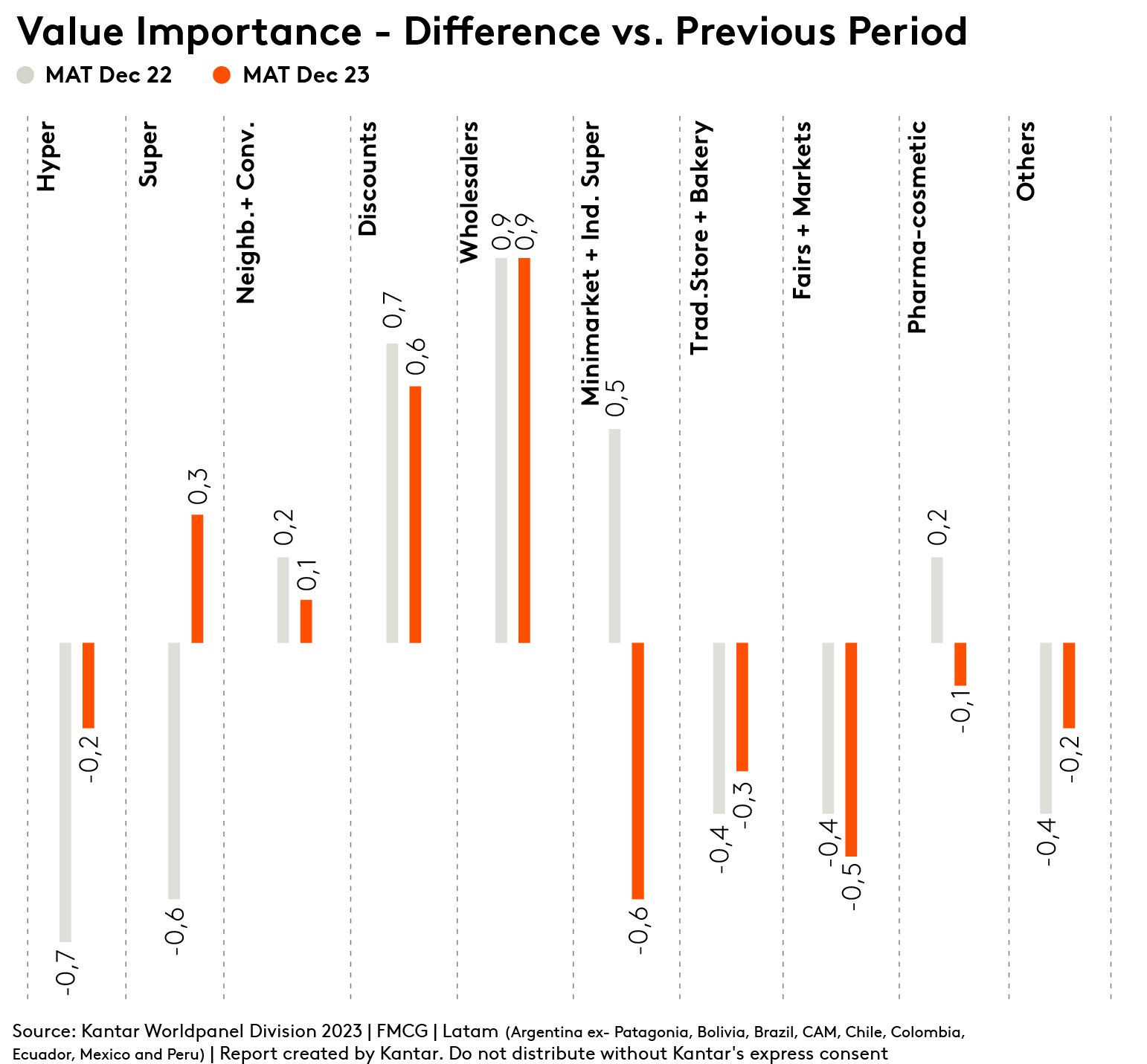

Like it, or not, value perception has become the north star across different channels, and our data illustrates the importance of this navigation point: wholesalers and discounters are rising in stature, perceived by consumers as bastions of better value for money.

Conversely, the giants of retail — hypermarkets and supermarkets — and the niche sector of pharmacies display a downward trajectory in value importance, hinting at a consumer pivot towards more economical shopping avenues, particularly pronounced in countries grappling with the heaviest inflation loads.

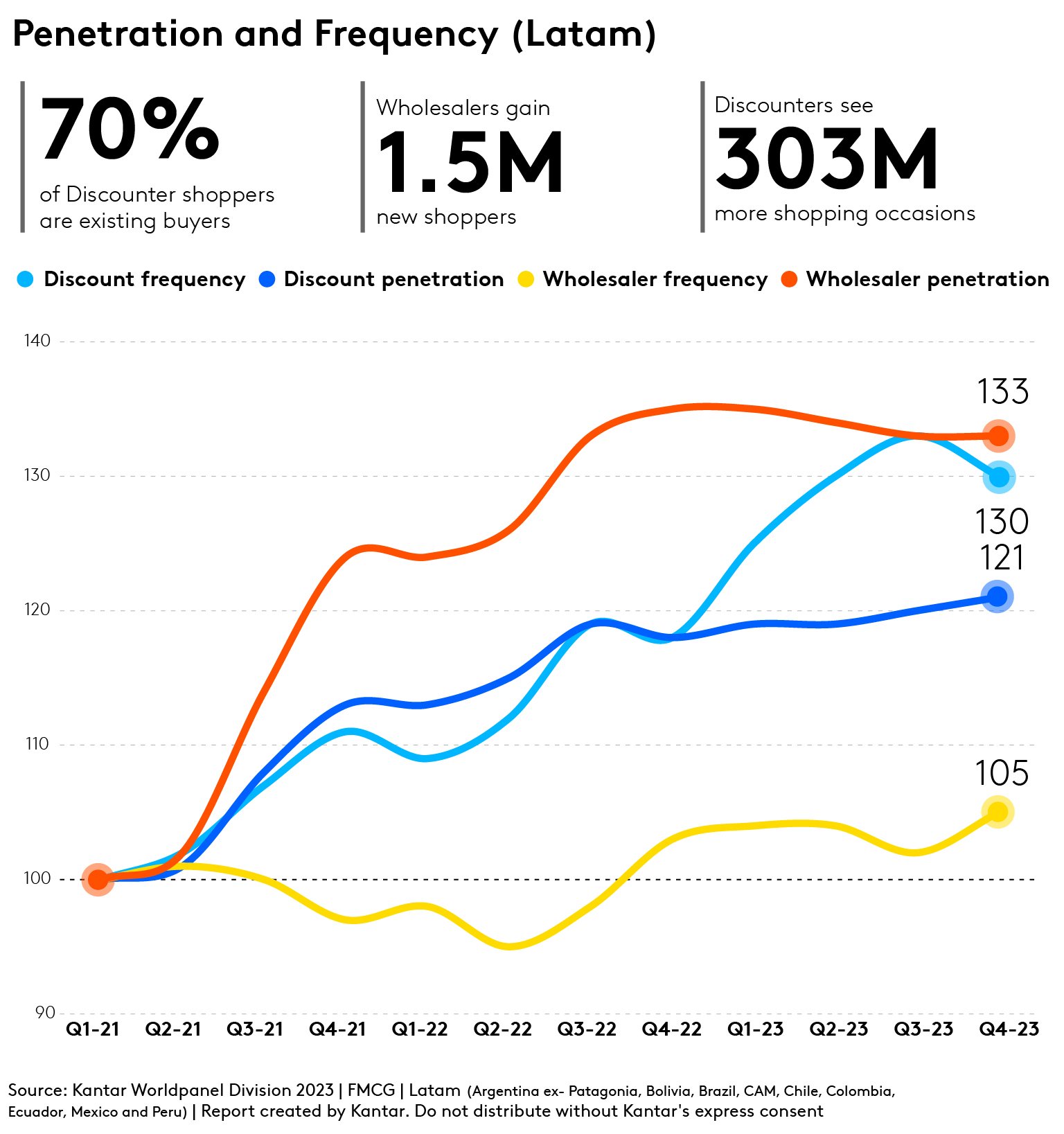

Amidst the shift to discounters and wholesalers, we also see telling indicators in penetration rates and usage frequency. Discounters are charting an upward trajectory, welcoming a growing number of consumers through their doors, evidenced by higher penetration and frequency rates showing no meaningful signs of slowing.

Conversely, wholesalers are carving out their own domain, expanding their consumer base by 1.5 million new shoppers finding allure in the broader product assortment available. The frequency of visits to wholesalers tells of a staggering 303 million additional shopping occasions underscoring their growing footprint in the consumer's routine.

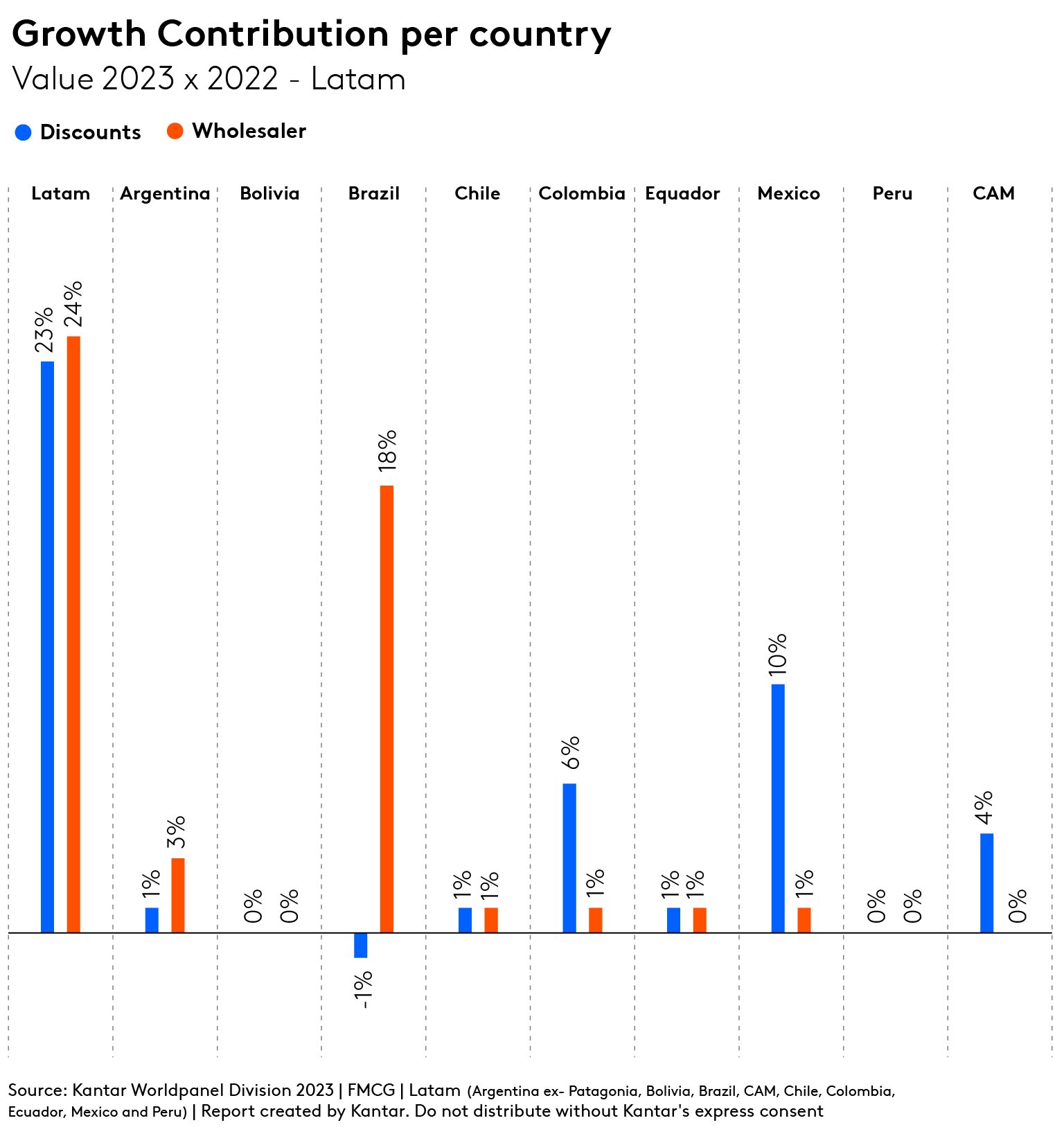

So where are discounters and wholesalers running fastest? Analysing the growth contributions by country within Latin America from 2022 to 2023, Brazil stands out as the powerhouse behind the growth of wholesalers, while Mexico and Colombia are the driving forces propelling the expansion of discount stores. Ecuador is also seeing solid signs of growth in the discounters.

Interestingly, a substantial 70% of discounter volume growth is credited to retained buyers, which indicates a strong loyalty within the discounter shopper base. Additionally, a quarter of this growth is drawn from consumers transitioning from other retail formats, both large and small.

This trend within discounters showcases their ability to pull in consumers who are driven by value for money and, perhaps, an evolving preference towards more streamlined shopping experiences.

With a keen eye on the European market, where discounters have consistently increased their market share over decades, the expectation is that this retail format will continue to expand as plans for more stores unfold across Latin America. Brands should be agile and responsive to these trends, leveraging the loyalty and cross-channel appeal that discounters have carved out to remain competitive and resonant with consumer needs.

Discount stores and wholesalers are capturing the attention and loyalty of Latin American consumers, with large increases in shopper numbers and visit frequency. This reflects a shift towards price-conscious purchasing and a preference for expansive store formats that offer a diverse range of products at competitive prices. Simultaneously, discounters are aggressively promoting their private label products, a strategy that places considerable pressure on branded products striving to secure shelf space.

The distinct growth patterns of these increasingly popular channels also reveal diverse consumer motivations: wholesalers draw in consumers for bigger shopping trips less frequently and discounters entice regular visits with their focus on competitive pricing and targeted shopping expeditions. The implication for those operating other channels is the necessity to remap offerings to shopper demands increasingly being satisfied elsewhere.