The timeline we are looking at covers the 52 weeks to 20 February 2022 versus the previous 12 months. This also coincides with the pandemic so the brands that feature will have navigated this growth in a period where consumers have adapted to restrictions imposed on their behaviours and freedoms.

The value of food and drink in Scotland for the grocery channel is £10.3bn, up 11% versus pre-pandemic levels. The manufacturers, retailers and supply chain that contribute to this value, and the people they employ, are integral to Scotland’s economy.

This was a period where there were less promotions: 27% sold on promotion versus 31% pre-pandemic. The partial closure of the hospitality sector meant that for many consumers a higher proportion of their total food and drink spend was in the grocery channel. This has been one of the most dynamic periods in retailing which resulted in double-digit value growth for the retailers and even higher growth for some categories such as alcohol.

This has been a time when we changed where and how we shopped with an increase in online market share as shoppers across all ages embraced digital shopping and delivery. This also led to an increase in the use of aggregators and apps to facilitate other innovative methods of delivery.

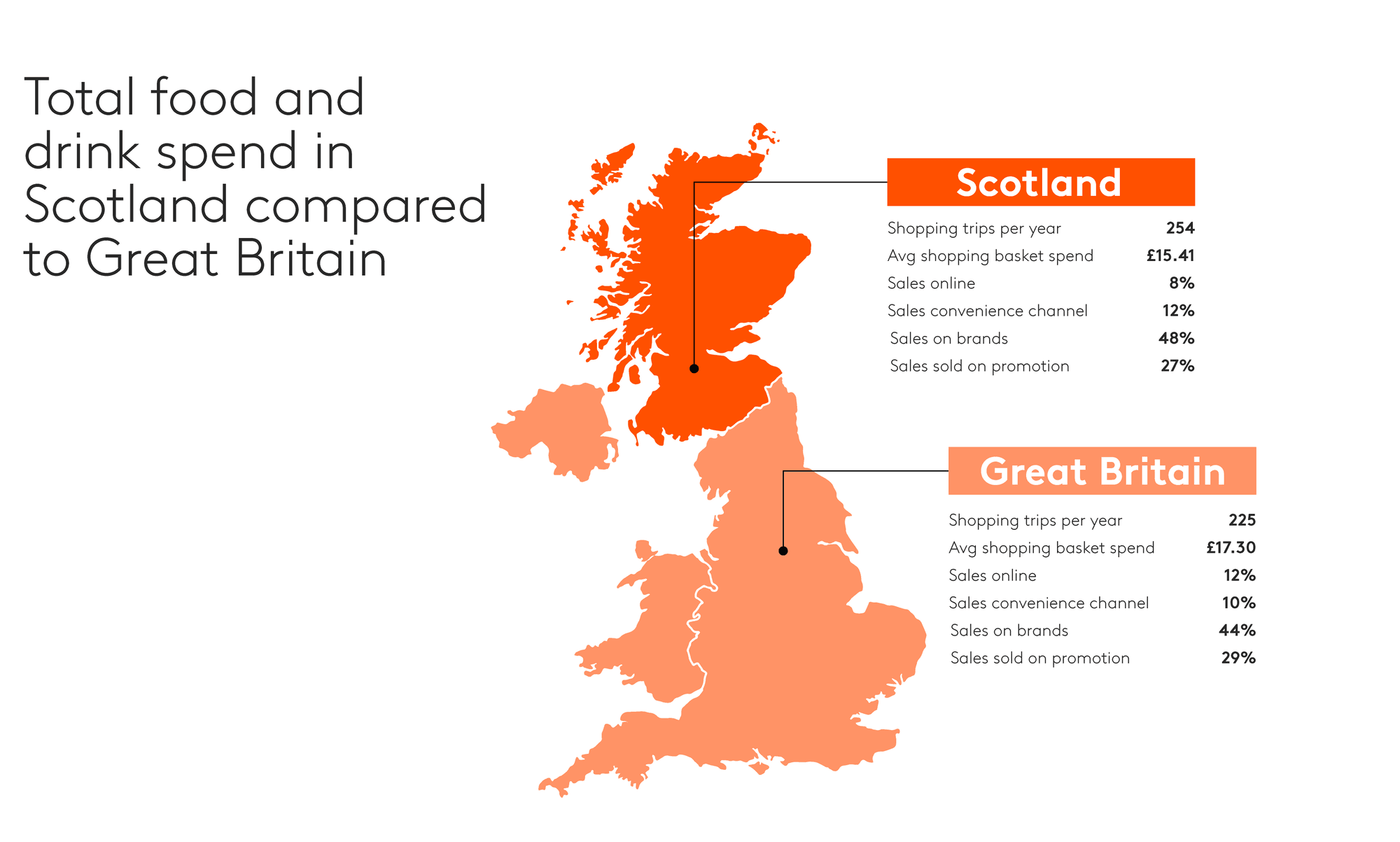

How do we shop in Scotland compared to Great Britain? There are still some fundamental differences to the Scottish grocery channel metrics compared to total Great Britain. In Scotland, we shop more frequently, our average basket spend is less, the convenience channel is more important and a higher percentage of our spend is on brands while the value sold on promotion is less.