Category insights

Beer leads the way

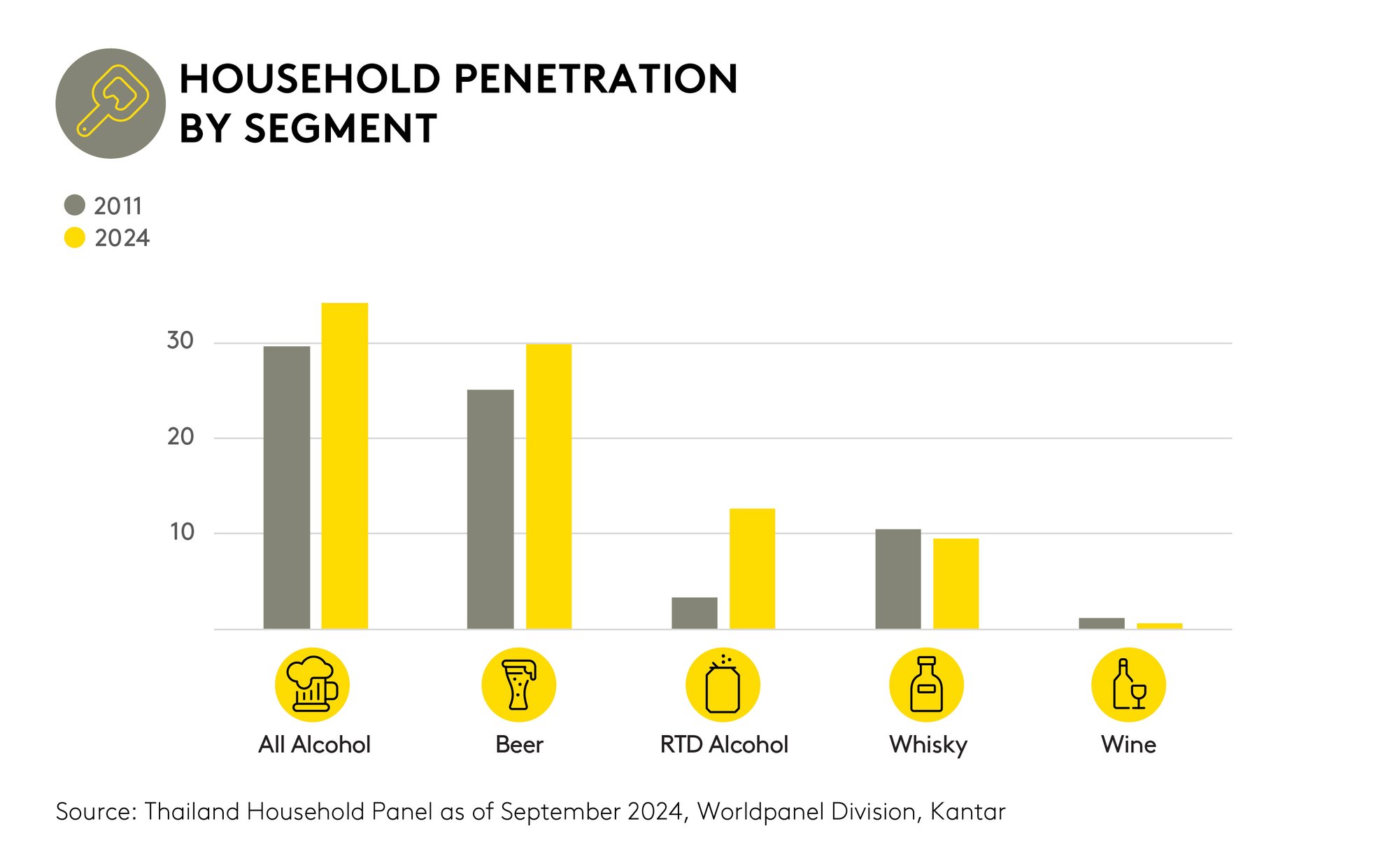

In terms of segments, Beer continues to be most popular, with about one third of Thai households buying it at least once a year. Beer is also the largest category, accounting for approximately 70% of spend in the total alcoholic beverage market, followed by whiskey and spirits.

Despite a decline in the number of buyers, a trend also seen across other alcoholic beverages, overall consumption both in and out of home is still increasing, and this is keeping the beer market stable.

RTD alcohol

Taking a closer look at the profile of RTD alcohol, we found that female consumers contributed more than 70% of category sales, compared to 35% for beer. RTD alcohol also attracted much younger shoppers, with those in their twenties contributing 40% of category sales, compared with 20% for beer.

Spirits

The spirits category has gained in popularity over the past year, particularly soju and brandy. Although products in this category did not grow much in 2024, due to a slowdown in purchases across the broader alcoholic beverage market, we find that buyers of these products are exploring new experiences, especially in brandy.

This segment has seen more brands entering the market, including traditional players like Regency, which has maintained a strong customer base. In addition, some buyers have shifted from beer to brandy, making it the only spirit that is still growing within the spirits category.

However, the type of liquor with the largest footprint in this group remains white spirits, which has the highest number of buyers nationwide. Overall, the market is contracting due to a decrease in white spirit buyers, along with the increasing number of consumers who are shifting to whiskey instead. Although this behaviour can be viewed as a form of premiumisation, it is likely to be taking a significant share of white spirit drinkers’ wallets.

Whiskey

Worldpanel’s long-term market surveys in Thailand indicate that the whiskey category is facing long-term issues, with a continuous decline in the number of buyers over several years. In the past year, the whiskey market has seen a significant drop in households purchasing for home consumption, with regular whiskey buyers ceasing to buy, but not purchasing any other types of alcoholic beverages as an alternative.

Additionally, those who typically buy whiskey and other spirits are opting to remove whiskey from their shopping baskets in favour of other products. This is a primary reason for the severe decline in the whiskey market within the alcoholic beverage sector.

When we look at the out-of-home whiskey consumption behaviour, the picture may appear positive, as there has been a slight increase in the number of whiskey buyers, primarily due to increased consumption frequency. However, whiskey remains the slowest-growing alcoholic beverage in the out-of-home market, presenting another challenge for brands. They may need to seek more and better insights into sales channels, product perspectives, and consumer behaviour.

Whiskey remains the slowest-growing alcoholic category, underscoring the need for deeper consumer insights.