Inno-Vation nation

How brands are pioneering new products to satisfy shoppers' demands

It is a truth universally acknowledged, though rarely as true as we might think, that we are creatures of habit. We supposedly stick with the products we know, the ones that have been with us through thick and thin, in good times and in bad. But sometimes — much more often than one might imagine — we reconsider our choices.

Such is the case in the world of fast-moving consumer goods, where the landscape is shifting again, and the pressures of inflation and economic uncertainty are pushing shoppers to reassess their buying habits.

In an environment where (increasingly) every purchase counts for penny-pushed households, we face a shopping metamorphosis of sorts. The industry is well and truly grappling with the complexities of shifting consumer preferences, rising inflation, and margins under pressure.

Frustratingly, the common narratives that have historically emerged during times of economic crisis are that new product development is less necessary or, for some, not necessary at all. History has proved this to be wrong. Those who innovate in tough times tend to come out ahead. And guess what, we’re seeing that very dynamic play out again.

Under pressure

But first, some context: In May 2020, Kantar began tracking households through three lenses - we call them pressure groups - comfortable, managing, and struggling. These terms are how the households we measure describe their financial circumstances. We’ve continued to track them through the dark days of the pandemic and into 2023.

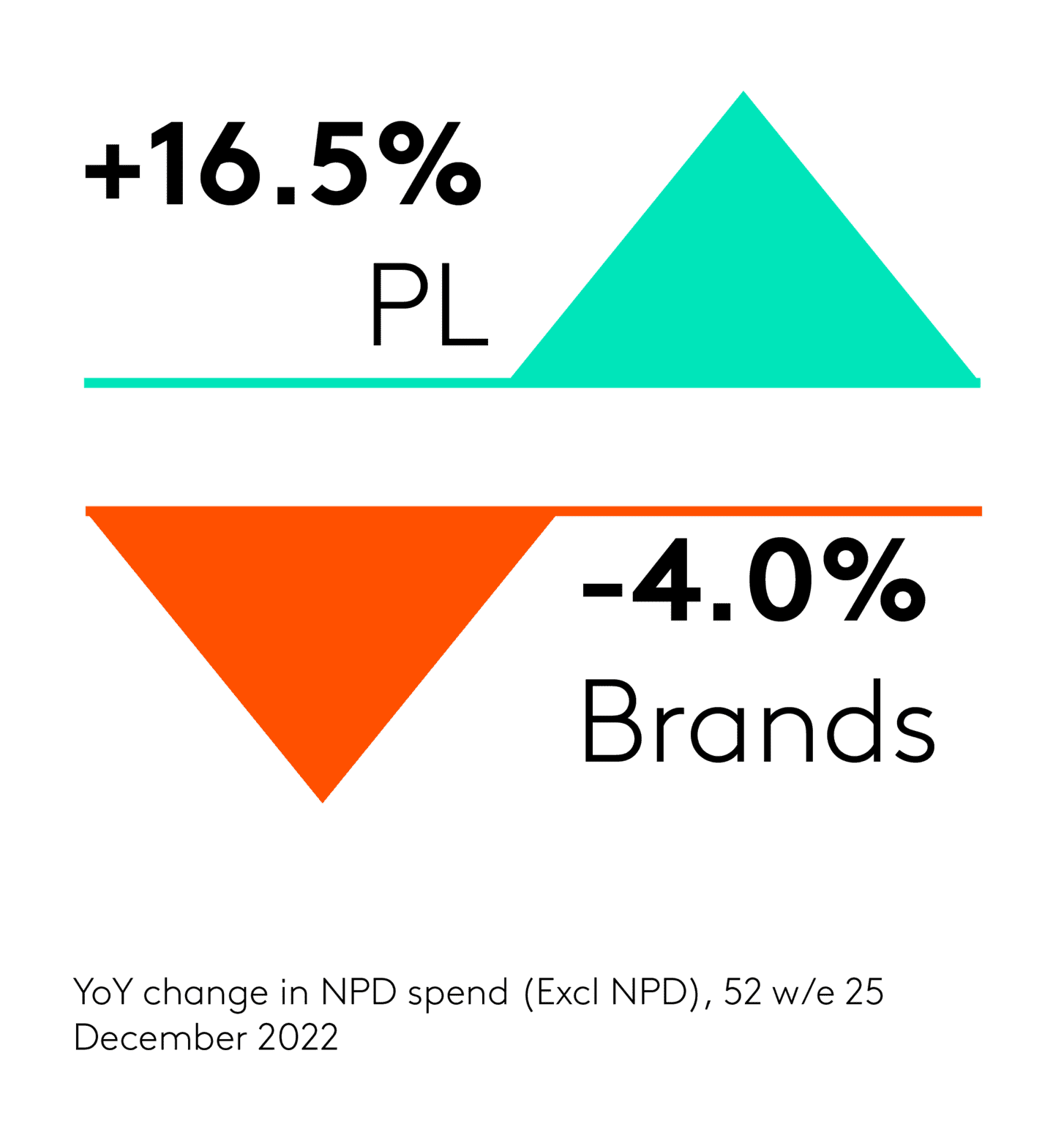

When we looked at the most recent full year of data on new products released into the market (2022), we found that struggling shoppers still represented a strong market for branded new products (NPD), even though they are looking for more private label (PL) in their lives.

Yes, you read that right — struggling shoppers are willing to risk their hard-earned cash for new products. But brands have to get it right.

Struggling shoppers over-traded in seven out of the top 10 NPDs vs their comfortable and managing counterparts. Even premium propositions had a place for struggling consumers. This is a big deal.

But the reality of private label products and their continued rise is also a big deal. And very real. Private label products, often called own-label, have been handily outpacing branded products introduced to the market.

Growth remains possible

But that doesn't mean the end of the road for branded products. In some categories, such as toiletries, alcohol, and household items, branded innovation growth remains strong. This tells us there is still ample room for consumer goods brands to make their mark, despite the rising competition from private label products.

Perhaps unsurprisingly, we see those consumers who say they are struggling financially are more likely to gravitate towards private label products. While those who are comfortable or managing their finances prefer branded products. Brands, therefore, need to be able to cater to the needs of these different groups by adapting their strategies and product offerings accordingly.

Inflationary challenges

Rising inflation is another challenge that looms large, and is part of the innovation picture. As prices continue to rise, consumers become more price-sensitive and start looking for cheaper alternatives, often in private label.

In such an environment, brands that can offer value to consumers without sacrificing quality are often seeing success and mitigating the pivot to private label.

To create and expand on opportunities for growth, FMCG brands and retailers must focus relentlessly on several key areas. Firstly, they need to adapt their product offerings to cater to the different needs and tensions sitting inside consumer groups. Our struggling, managing, and comfortable pressure groups provide a sensible framework to follow. There are, of course, other forms of segmentation our teams commonly deploy. One crucial aspect to consider when adapting product offerings is identifying areas where private label credentials are strong enough to provide a palatable alternative to branded products. This strategy should be led by understanding where shoppers are willing to compromise or sacrifice, and where it would be wasteful to deny brands valuable shelf space. For instance, discounters struggle to crack the toiletries market because established brands dominate the sector. However, this isn't always the case; nappies are an excellent example of successful private label investment.

Overall, the key is to strike a balance between offering more private label products in certain categories while continuing to invest in branded innovation in other categories, always considering the consumers' preferences and the market dynamics.

Secondly, brands and supermarkets need to find ways to offer different kinds of value to consumers. For example, this could involve providing products packaged in sustainable materials or providing clarity on the efficacy of the supply chain. Admittedly, sustainable products tend to be a more difficult sale in tough economic times, but remain appealing if the right price point and value exchange can be found. Additionally, brands need to communicate more effectively with consumers about the value they offer and be more transparent about their pricing. The price-sensitive shopper needs brands to remove risk from their considerations at the checkout.

Finally, embracing digital technologies has become a necessity for brands and supermarkets, rather than just an option. Investing in e-commerce platforms, developing mobile apps, and engaging with consumers via social media are now essential to meet consumers' expectations and helping them with their grocery spend. Notably, these digital platforms are more cost-effective than traditional media like TV, making them attractive to those looking to cut back on expenses.

However, it is worth mentioning that historically, businesses that continue to invest in advertising during recessionary periods usually emerge stronger in the long run.

In particular, food products have a unique opportunity to use media platforms to educate consumers about scratch cooking as a cost-saving alternative to eating out or buying ready meals. Brands can leverage digital platforms to provide recipe ideas, cooking tips, and tutorials to encourage more home cooking.

Similarly, in the health and beauty sector, companies can offer beauty tutorials that empower consumers to confidently downtrade from salon services to at-home solutions. By providing valuable content and engaging with consumers through these cost-effective digital channels, brands can also build longterm loyalty.

As the saying goes, if you don’t like change, you’ll like irrelevance even less.