Making assumptions about consumer behaviour will be a bigger mistake than usual, given the current economic climate. Changing product pack size demands and pricing shifts are already proving this true.

As the tide of recession sweeps Britain, the familiar “rule of thumb” expectation has been that, as in the past, pressured consumers would immediately rush to the lowest price tiers and switch to smaller pack sizes to manage their day-to-day spending. But this has not entirely been the case.

The dominant tier of products with year-on-year growth has been lower mid-tier products, not those products at the extreme value end of the range. In other words, a rush to the cheapest products hasn’t happened. At least not yet.

That is not to say trading down is not taking place. It certainly is, but the downtrading is from premium or super-premium products to those nestling somewhere in the middle of the pricing spectrum. Category abandonment is, by and large, still not taking place on any scale on any price tier.

So what does this mean? Firstly, for those with premium offerings, it will be harder ground to defend. To keep consumers in those premium categories, it will be necessary to develop options in terms of pack sizes and to understand the dynamics of price by volume in the minds of loyal consumers. The advantage for consumers then becomes that the brand is helping them make like-for-like choices but in different, likely more affordable, pack sizes.

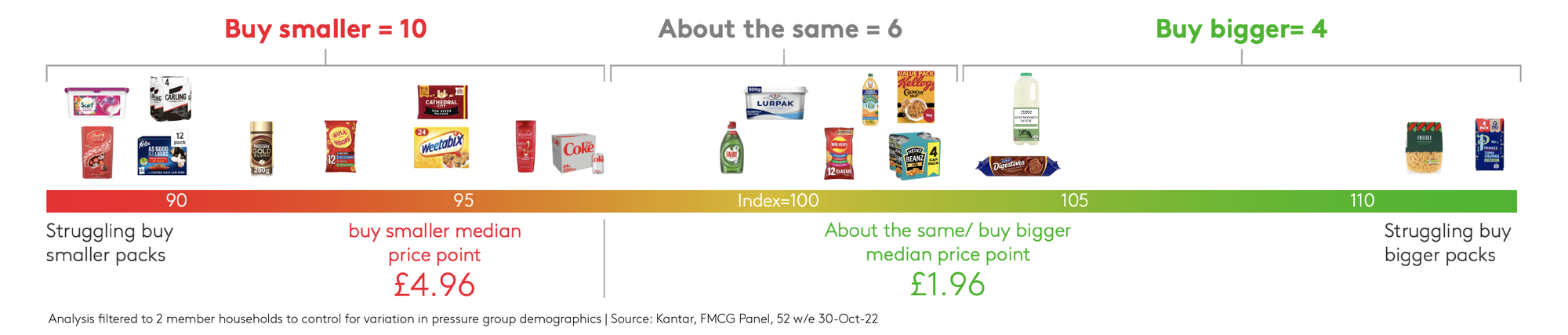

The expected shift to smaller pack sizes hasn’t yet happened at scale on more value-driven products. A Kantar review of 20 products across a wide range of popular categories found that for most products, bigger pack sizes offering more value were still popular despite pressured wallets. The difference from past recessionary behaviours is that the bigger pack sizes are in more favour than expected. However, as a consequence, some shopper segments are purchasing fewer products to mitigate rising costs. This is an important dynamic to monitor.

The takeaway here is that there may still be a risk for brands to err too heavily on offering smaller packs and thus undermine their position with retailers — at least until there is more obvious demand for smaller packs across a wider range of shoppers. The current dynamic requires brands to balance what value means to shoppers, understand how that meaning changes over time, and to recognise shoppers may not always behave rationally as they respond to market conditions.

In reality, bigger packs will only successfully work while people can afford them. Preparing to move ever so slightly in front of that demand dynamic will be where sales are likely to be optimised. Hints of the future can already be found in shoppers who say their households are struggling. These shoppers are leaning towards smaller packs, but not in all categories or at all price points. Products that have high price points are the first to feel the shift to smaller pack choices. It makes sense since bigger packs of things that cost more in any size put bigger demands on the wallet.

The counterbalance to this is that those same struggling shoppers are still willing to buy bigger packs for products typically lower in price as they further mitigate risk. A large pack of pasta or rice is less financial exposure than a large pack of higher-end chocolate or imported canned food. It makes sense.

Failing to focus on this moving price and packaging architecture will bring risk to maintaining market share. It will be particularly critical to understand for brands in a higher price point category whose buyers have room to trade down but remain in the category.

And for all brands, context will be king. The correlation of mindset, spending power, basket management, and store will be mission critical as interlocking components of a savvy strategy.